You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Valuation of Cryptocurrency Mining Operations: Jose BerengueresDocument8 pagesValuation of Cryptocurrency Mining Operations: Jose BerengueresShyam P SharmaNo ratings yet

- Valuation of Crypto-Currency Mining Operations: J. BerengueresDocument8 pagesValuation of Crypto-Currency Mining Operations: J. BerengueresShyam P SharmaNo ratings yet

- AWS Governance at ScaleDocument21 pagesAWS Governance at ScaleShyam P SharmaNo ratings yet

- LIBOR Transition Update: Author: Kevin LiddyDocument13 pagesLIBOR Transition Update: Author: Kevin LiddyShyam P SharmaNo ratings yet

- Why The Day After Is Critical: Jayesh Punater - Nuclues January 2020Document3 pagesWhy The Day After Is Critical: Jayesh Punater - Nuclues January 2020Shyam P SharmaNo ratings yet

- 10062019042502blend - AIF - May - 2019Document7 pages10062019042502blend - AIF - May - 2019Shyam P SharmaNo ratings yet

- Equity Long/short: Are Your Shorts Delivering Alpha?: June 2016Document8 pagesEquity Long/short: Are Your Shorts Delivering Alpha?: June 2016Shyam P SharmaNo ratings yet

- Lu Liquidity Risk Management A Look at The Tools AvailableDocument12 pagesLu Liquidity Risk Management A Look at The Tools AvailableShyam P SharmaNo ratings yet

- Sid Absl Frontline Equity Fund Rev 2205Document76 pagesSid Absl Frontline Equity Fund Rev 2205Shyam P SharmaNo ratings yet

- Investment Insights Market Neutral Investing: Spotlight OnDocument6 pagesInvestment Insights Market Neutral Investing: Spotlight OnShyam P SharmaNo ratings yet

- CBS EpmDocument30 pagesCBS EpmShyam P SharmaNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

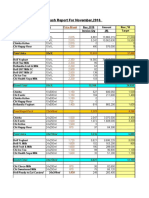

- Aba Monthly Report As at Nov (1) .'10Document78 pagesAba Monthly Report As at Nov (1) .'10Vivek RaghavNo ratings yet

- Universal Remote Control For LG Smart TV Remote Control All Models Complete Features Instruction GuideDocument5 pagesUniversal Remote Control For LG Smart TV Remote Control All Models Complete Features Instruction GuideJeancarlos DominguezNo ratings yet

- Adding New Protocol To ns2Document27 pagesAdding New Protocol To ns2Rajendra BhosaleNo ratings yet

- IBSSA 2008aDocument42 pagesIBSSA 2008asrdjan013No ratings yet

- Rubrics For Infographics PDFDocument2 pagesRubrics For Infographics PDFRansel Burgos100% (2)

- Health Care GuideDocument51 pagesHealth Care GuideM Zainuddin M SaputraNo ratings yet

- Ethics Marks Improvement Booklet 2023Document63 pagesEthics Marks Improvement Booklet 2023Jas SinNo ratings yet

- Automatically Rain Covering SystemDocument40 pagesAutomatically Rain Covering Systemsumathi100% (1)

- Advanced Intelligent Systems For Sustain PDFDocument1,021 pagesAdvanced Intelligent Systems For Sustain PDFManal EzzahmoulyNo ratings yet

- Project On BudgetingDocument75 pagesProject On BudgetingManeha SharmaNo ratings yet

- Parliamentary InviteDocument5 pagesParliamentary InviteNaqee SyedNo ratings yet

- Honda Bf40a Owners ManualDocument120 pagesHonda Bf40a Owners ManualajcapetillogNo ratings yet

- Linux JournalDocument55 pagesLinux JournalHaseeb ShahidNo ratings yet

- B2 Wordlist EnglishDocument43 pagesB2 Wordlist EnglishHeba AlkhawajaNo ratings yet

- Engine Description: CharacteristicsDocument3 pagesEngine Description: Characteristicshorny69No ratings yet

- Old Sharp TV ManualDocument32 pagesOld Sharp TV ManualL RaShawn LusterNo ratings yet

- Introduction MGT (NSA)Document47 pagesIntroduction MGT (NSA)Mengistu MeraNo ratings yet

- Public Sector Financial Accounting Techniques A. Public Sector Financial Accounting TechniquesDocument3 pagesPublic Sector Financial Accounting Techniques A. Public Sector Financial Accounting TechniquesRANIA ABDUL AZIZ BARABANo ratings yet

- 3DHouse Report PDFDocument29 pages3DHouse Report PDFPrithviRaj GadgiNo ratings yet

- Answers For Test-secEDocument4 pagesAnswers For Test-secEAbhishek Sharda100% (1)

- Allan Mwirigi CVDocument3 pagesAllan Mwirigi CVallan kimaathiNo ratings yet

- Horlicks ProjectDocument56 pagesHorlicks ProjectShams S82% (34)

- Calculated Uncertainty of Temperature Due To The Size-of-Source EffectDocument8 pagesCalculated Uncertainty of Temperature Due To The Size-of-Source EffectRONALD ALFONSO PACHECO TORRESNo ratings yet

- 3.teaching Methods Any 5Document18 pages3.teaching Methods Any 5Veena DalmeidaNo ratings yet

- Maid Visa ProcessDocument2 pagesMaid Visa ProcessMuvinda JayasingheNo ratings yet

- Advanced Metering InfrastructureDocument50 pagesAdvanced Metering InfrastructureLudlow_thompson100% (2)

- Rolling of ShipsDocument37 pagesRolling of ShipsMark Antolino75% (8)

- Rerum Novarum - Cled 4Document2 pagesRerum Novarum - Cled 4Melprin CorreaNo ratings yet

- Circular 14 2022Document3 pagesCircular 14 2022shantXNo ratings yet

- Chapter 10: StaircasesDocument25 pagesChapter 10: Staircasestoyi kamiNo ratings yet