You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Property Sector - Residential and Mall Segments Weakened While Office Segment Stayed ResilientDocument4 pagesProperty Sector - Residential and Mall Segments Weakened While Office Segment Stayed ResilientJNo ratings yet

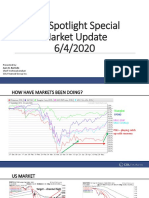

- Tech SpotlightDocument18 pagesTech SpotlightJNo ratings yet

- COL Guide - How To Make Your First InvestmentDocument4 pagesCOL Guide - How To Make Your First InvestmentJNo ratings yet

- The Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresDocument26 pagesThe Expenditure Cycle Part 1: Purchases and Cash Disbursements ProceduresJNo ratings yet

- Adjusting Entries LectureDocument13 pagesAdjusting Entries LectureJNo ratings yet

- 5 Short Term FinancingDocument27 pages5 Short Term FinancingJNo ratings yet

- Literature Theory 1Document14 pagesLiterature Theory 1JNo ratings yet

- 5 Short Term Financing PDFDocument48 pages5 Short Term Financing PDFJNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Measuring The Cost of LivingDocument5 pagesMeasuring The Cost of LivingEdmar OducayenNo ratings yet

- WEEK 13-Pengaruh Pendapatan Dan Kelas SosialDocument18 pagesWEEK 13-Pengaruh Pendapatan Dan Kelas Sosialpew pelNo ratings yet

- Micro4 - Price Floor and Ceilings - 2021Document35 pagesMicro4 - Price Floor and Ceilings - 2021Divya Deepika BobbiliNo ratings yet

- SK BirDocument2 pagesSK BirGem LarezaNo ratings yet

- Habraz Bina SDN BHD: CustomerDocument2 pagesHabraz Bina SDN BHD: Customerroslan yusofNo ratings yet

- The Importance of Competition and Enterprise CompetitivenessDocument6 pagesThe Importance of Competition and Enterprise CompetitivenessNastea SelariNo ratings yet

- COCA COLA CO Balance Sheet: Period Ending FY2010 FY2009 FY2008 FY2007 FY2006Document5 pagesCOCA COLA CO Balance Sheet: Period Ending FY2010 FY2009 FY2008 FY2007 FY2006Sudeep PatneNo ratings yet

- RA Sand BlastingDocument2 pagesRA Sand BlastingAbdus Samad100% (1)

- MOP (Method of Procedure) : TFM (Technical Facilities Management)Document7 pagesMOP (Method of Procedure) : TFM (Technical Facilities Management)MEER MUSTAFA ALINo ratings yet

- Accountancy - Bills of Exchange - 230929 - 081107Document21 pagesAccountancy - Bills of Exchange - 230929 - 081107Amritha VNo ratings yet

- National Income and Price DeterminationDocument3 pagesNational Income and Price Determinationbustiman20No ratings yet

- Gayangan, Jenny Ann C. Bsa 3 Cost Accounting Number 1 Answer: CDocument3 pagesGayangan, Jenny Ann C. Bsa 3 Cost Accounting Number 1 Answer: CKarlo PalerNo ratings yet

- Hope and WishDocument4 pagesHope and WishsupriyantoNo ratings yet

- Wallstreetjournal 20171128 TheWallStreetJournalDocument34 pagesWallstreetjournal 20171128 TheWallStreetJournalsadaq84No ratings yet

- Contemporary World - Bretton WoodsDocument18 pagesContemporary World - Bretton WoodsFaith DomingoNo ratings yet

- Economic Costs of Imperfect Competition 1Document16 pagesEconomic Costs of Imperfect Competition 1Mir Hossain Ekram100% (1)

- FINANCING HIGHER EDUCATION IN INDIA IN THE ERA OF GLOBALIZATION-TKhan-2014Data-5April2021Document60 pagesFINANCING HIGHER EDUCATION IN INDIA IN THE ERA OF GLOBALIZATION-TKhan-2014Data-5April2021Purandar DattaNo ratings yet

- Tugas - Rate of Return AnalysisDocument2 pagesTugas - Rate of Return AnalysisJoshua HutaurukNo ratings yet

- John J Murphy - Technical Analysis of The Financial MarketsDocument596 pagesJohn J Murphy - Technical Analysis of The Financial Marketsbarbarajeanlavender97% (75)

- Activity 1 - PAYROLL SYSTEMDocument2 pagesActivity 1 - PAYROLL SYSTEMEmilyn olidNo ratings yet

- Liberalization, Privatisation and Globalisation!Document37 pagesLiberalization, Privatisation and Globalisation!Nivesh GuptaNo ratings yet

- RRLDocument2 pagesRRLjullana gaddiNo ratings yet

- Utility Shifting PDFDocument2 pagesUtility Shifting PDFPratik GuptaNo ratings yet

- Fundamentals of Partnership: Dhiman ClaimsDocument7 pagesFundamentals of Partnership: Dhiman ClaimsAyareena GiriNo ratings yet

- 0 Transmitting 132Kv Substation 1 Project Master Schedule: Construction DrawingsDocument39 pages0 Transmitting 132Kv Substation 1 Project Master Schedule: Construction Drawingsshahidbolar0% (1)

- HoliDocument3 pagesHoliEazhil DhayallanNo ratings yet

- Michael Porter's Diamond ModelDocument5 pagesMichael Porter's Diamond ModelTiberiu FalibogaNo ratings yet

- OMZIL MID YEAR 2021 FINANCIAL RESULTS FINAL From Lawrence 31AUG21Document10 pagesOMZIL MID YEAR 2021 FINANCIAL RESULTS FINAL From Lawrence 31AUG21Mandisi MoyoNo ratings yet

- How To Trade Chart Patterns With Target and SL@Document39 pagesHow To Trade Chart Patterns With Target and SL@millat hossain100% (1)

- Final File General Awareness Capsule Ibps Po Clerk Mains 2022 Gopal Sir 2Document119 pagesFinal File General Awareness Capsule Ibps Po Clerk Mains 2022 Gopal Sir 2JugnuNo ratings yet