You might also like

- Test Bank For Financial Reporting and Analysis 8th Edition Lawrence Revsine Daniel Collins Bruce Johnson Fred Mittelstaedt Leonard SofferDocument55 pagesTest Bank For Financial Reporting and Analysis 8th Edition Lawrence Revsine Daniel Collins Bruce Johnson Fred Mittelstaedt Leonard Soffergisellesamvb3100% (20)

- IMPACT-MFDocument16 pagesIMPACT-MFFarah YasserNo ratings yet

- LOMA FLMI CoursesDocument4 pagesLOMA FLMI CoursesCeleste Joy C. LinsanganNo ratings yet

- 2007-2013 MERCANTILE Law Philippine Bar Examination Questions and Suggested Answers (JayArhSals)Document173 pages2007-2013 MERCANTILE Law Philippine Bar Examination Questions and Suggested Answers (JayArhSals)Jay-Arh97% (103)

- Assign 4 Answer Partnership Liquidation Millan 2021Document12 pagesAssign 4 Answer Partnership Liquidation Millan 2021mhikeedelantar100% (1)

- MPRA Paper 31815 PDFDocument9 pagesMPRA Paper 31815 PDFHajra ANo ratings yet

- Review of Past Literature On AgricultureDocument8 pagesReview of Past Literature On AgricultureAftab AhmadNo ratings yet

- MUHAMMAD IQBAL, MUNIR AHMAD, and KALBE ABBAS PDFDocument15 pagesMUHAMMAD IQBAL, MUNIR AHMAD, and KALBE ABBAS PDFHajra ANo ratings yet

- A STUDY ON EFFECTIVENESS OF AGRICULTURAL LOANSDocument4 pagesA STUDY ON EFFECTIVENESS OF AGRICULTURAL LOANSRakshith AcharyaNo ratings yet

- ECB Scopus ArticleDocument8 pagesECB Scopus ArticleRaviShankarNo ratings yet

- tmp963D TMPDocument11 pagestmp963D TMPFrontiersNo ratings yet

- A Study On Agriculture Insurance in India - SbiDocument18 pagesA Study On Agriculture Insurance in India - SbiMOHAMMED KHAYYUMNo ratings yet

- Impact of Institutional Credit On Agricultural Productivity in Sindh PakistanDocument9 pagesImpact of Institutional Credit On Agricultural Productivity in Sindh PakistanHajra ANo ratings yet

- NABARD Jaisheela B 2017 PDFDocument7 pagesNABARD Jaisheela B 2017 PDFPrema G100% (1)

- Utilization of Agriculture Credit by The Farming Community of Zarai Tariqiati Bank Limited (ZTBL) For Agriculture DevelopmentDocument4 pagesUtilization of Agriculture Credit by The Farming Community of Zarai Tariqiati Bank Limited (ZTBL) For Agriculture DevelopmentAshfaq AhamdNo ratings yet

- A Synopsis Report ON AT Sbi Bank: Agricultural InsuranceDocument11 pagesA Synopsis Report ON AT Sbi Bank: Agricultural InsuranceMOHAMMED KHAYYUMNo ratings yet

- Role of Cooperative Bank in Agricultural PDFDocument12 pagesRole of Cooperative Bank in Agricultural PDFYashodhara BhattNo ratings yet

- LIKITHA - Agri F InsuDocument16 pagesLIKITHA - Agri F InsuMOHAMMED KHAYYUMNo ratings yet

- 10 - Article On Sources and UsesDocument12 pages10 - Article On Sources and Usesiiste100% (1)

- Manuscript 2023Document14 pagesManuscript 2023Divesh DuttNo ratings yet

- Agriculture FinanceDocument14 pagesAgriculture FinanceRutik PanchalNo ratings yet

- 62 PDFDocument7 pages62 PDFShibin T. ANo ratings yet

- Review of Literature: Chapter-2Document5 pagesReview of Literature: Chapter-2Juan JacksonNo ratings yet

- Literature Review JDocument9 pagesLiterature Review JmovinNo ratings yet

- COM_V4_N3_026Document8 pagesCOM_V4_N3_026pradhanraja05679No ratings yet

- A Study On Agricultural Finance in India - Awareness and UsageDocument46 pagesA Study On Agricultural Finance in India - Awareness and UsageAnkita Rathod80% (5)

- Cooperative BankDocument10 pagesCooperative BankUlagaNo ratings yet

- The Effects of Short Term AgriculturalDocument6 pagesThe Effects of Short Term AgriculturalNyiter Fanen AndrewNo ratings yet

- University of MumbaiDocument46 pagesUniversity of MumbaiswapnilhadkeNo ratings yet

- A Synopsis Report ON AT Sbi Bank: Agricultural InsuranceDocument13 pagesA Synopsis Report ON AT Sbi Bank: Agricultural InsuranceMOHAMMED KHAYYUMNo ratings yet

- An Evaluation of Pre-And Post Sanction Process in Agriculture Credit by BanksDocument17 pagesAn Evaluation of Pre-And Post Sanction Process in Agriculture Credit by Banksnimisha praveenNo ratings yet

- Impact of Agricultural Credit On Product PDFDocument5 pagesImpact of Agricultural Credit On Product PDFHajra ANo ratings yet

- Institutional Credit To Agriculture Sector in India: Status, Performance and DeterminantsDocument12 pagesInstitutional Credit To Agriculture Sector in India: Status, Performance and DeterminantssumitNo ratings yet

- Agricultural Credit in BangladeshDocument40 pagesAgricultural Credit in Bangladeshaluka porota80% (5)

- Micro Finance ArticleDocument7 pagesMicro Finance ArticleBelkis RiahiNo ratings yet

- Private Capital Formation and Bank Credit AccessDocument11 pagesPrivate Capital Formation and Bank Credit AccessDr Ezekia SvotwaNo ratings yet

- Impact of Microfinance on Income and Living StandardsDocument9 pagesImpact of Microfinance on Income and Living StandardsShah WazirNo ratings yet

- Functioning of Kscard Bank in The Economic Development of Farming CommunityDocument9 pagesFunctioning of Kscard Bank in The Economic Development of Farming CommunityarcherselevatorsNo ratings yet

- Hassan Ali 467 PP (1-14)Document14 pagesHassan Ali 467 PP (1-14)International Journal of Management Research and Emerging SciencesNo ratings yet

- Thesis1 PDFDocument329 pagesThesis1 PDFUma deviNo ratings yet

- Financing Effectiveness in Agriculture: Comparing Conventional and Islamic BanksDocument8 pagesFinancing Effectiveness in Agriculture: Comparing Conventional and Islamic BanksNur WijayantoNo ratings yet

- Presentation, Analysis and FindingsDocument9 pagesPresentation, Analysis and FindingsMadhusudan BiswasNo ratings yet

- Credit Rationing in Rural India PDFDocument20 pagesCredit Rationing in Rural India PDFShivangi AgrawalNo ratings yet

- Role of Salem District Bank in Agricultural FinancingDocument4 pagesRole of Salem District Bank in Agricultural FinancingNaresh KumarNo ratings yet

- Document PDFDocument11 pagesDocument PDFAjinkya JagtapNo ratings yet

- 5th Sem ProjectDocument74 pages5th Sem Projectstellastar24No ratings yet

- Agricultural Credit in Pakistan: Constraints and OptionsDocument3 pagesAgricultural Credit in Pakistan: Constraints and OptionsSameen HussainNo ratings yet

- Chapter-1 Introduction and Design of The StudyDocument3 pagesChapter-1 Introduction and Design of The StudyRama ChandranNo ratings yet

- Bank AttachmentDocument9 pagesBank AttachmentAnanshya R VNo ratings yet

- Meutia Et Al - Comparative Analysis of Agricultural FinancingDocument24 pagesMeutia Et Al - Comparative Analysis of Agricultural Financingmuthiatur rofiahNo ratings yet

- 3-MJH 1515-Ok PDFDocument18 pages3-MJH 1515-Ok PDFAbid UllahNo ratings yet

- 21 Sources of Rural Finance PDFDocument15 pages21 Sources of Rural Finance PDFAman SinghNo ratings yet

- " Title of The Project ": Name of Student Batch PRNDocument22 pages" Title of The Project ": Name of Student Batch PRNMANSHI RAINo ratings yet

- Agricultural Finance in IndiaDocument69 pagesAgricultural Finance in Indiajyoti raghuvanshiNo ratings yet

- Role of Banks On Agricultural DevelopmenDocument7 pagesRole of Banks On Agricultural Developmenrufaidanurain2000No ratings yet

- Institute of Law Jiwaji University Gwalior: Agriculture Credit Sources and ProblemsDocument14 pagesInstitute of Law Jiwaji University Gwalior: Agriculture Credit Sources and ProblemsJake LavenstienNo ratings yet

- 661-Article Text-3020-1-10-20220311Document7 pages661-Article Text-3020-1-10-20220311reddy sekharNo ratings yet

- IMPACT OF AGRICULTURE LOAN ON AGRICULTURAL FARM PRODUCTIVITY: EVIDENCE FROM DISTRICT PARACHINAR, KURRAM AGENCY, PAKISTANDocument5 pagesIMPACT OF AGRICULTURE LOAN ON AGRICULTURAL FARM PRODUCTIVITY: EVIDENCE FROM DISTRICT PARACHINAR, KURRAM AGENCY, PAKISTANSheena Pearl RodeoNo ratings yet

- The Social and Financial Performance of Conventional and Islamic Microfinance Institutions in PakistanDocument19 pagesThe Social and Financial Performance of Conventional and Islamic Microfinance Institutions in PakistanmairaNo ratings yet

- Chapter IiDocument29 pagesChapter IiSarath KumarNo ratings yet

- Banks Credit and Agricultural Sector Output in NigeriaDocument12 pagesBanks Credit and Agricultural Sector Output in NigeriaPORI ENTERPRISESNo ratings yet

- Damodaram Sanjivayya National Law University: Instituional Credit and Agriculture in IndiaDocument18 pagesDamodaram Sanjivayya National Law University: Instituional Credit and Agriculture in IndiaSaniaNo ratings yet

- Blessing Stimulating Capital CreationDocument11 pagesBlessing Stimulating Capital CreationDr Ezekia SvotwaNo ratings yet

- Promoting Social Bonds for Impact Investments in AsiaFrom EverandPromoting Social Bonds for Impact Investments in AsiaNo ratings yet

- DataDocument18 pagesDataHajra ANo ratings yet

- THE LEVEL OF ENTREPRENEURSHIP GROWTH AND Obstacles in OpennessDocument16 pagesTHE LEVEL OF ENTREPRENEURSHIP GROWTH AND Obstacles in OpennessHajra ANo ratings yet

- Impact of Institutional Credit On Agricultural Output PDFDocument22 pagesImpact of Institutional Credit On Agricultural Output PDFRizwan KhalidNo ratings yet

- The Impact of Commercial Banks' Credit To Agriculture On Agricultural Development in Nigeria: An Econometric AnalysisDocument10 pagesThe Impact of Commercial Banks' Credit To Agriculture On Agricultural Development in Nigeria: An Econometric AnalysisJonesNo ratings yet

- Impact of Institutional Credit On Agricultural Productivity in Sindh PakistanDocument9 pagesImpact of Institutional Credit On Agricultural Productivity in Sindh PakistanHajra ANo ratings yet

- Impact of Public Debt On Economic GrowthDocument18 pagesImpact of Public Debt On Economic GrowthHajra ANo ratings yet

- The Role of Agricultural Credit in The Growth of Livestock Sector: A Case Study of FaisalabadDocument4 pagesThe Role of Agricultural Credit in The Growth of Livestock Sector: A Case Study of FaisalabadKhan NiaziNo ratings yet

- Sources: Pakistan Bureau of StatisticsDocument16 pagesSources: Pakistan Bureau of StatisticsHajra ANo ratings yet

- sUDAN, AHMEDDocument8 pagessUDAN, AHMEDHajra ANo ratings yet

- Agricultural Credit and Economic Growth in Nigeria: An Empirical AnalysisDocument8 pagesAgricultural Credit and Economic Growth in Nigeria: An Empirical AnalysisHajra ANo ratings yet

- Impact of Agricultural Credit On ProductivityDocument8 pagesImpact of Agricultural Credit On ProductivityArsalan ArifNo ratings yet

- Managerial AssignmentDocument5 pagesManagerial AssignmentHajra ANo ratings yet

- Role of Agricultural Credit On Production Efficiency of Farming Sector SAIMADocument7 pagesRole of Agricultural Credit On Production Efficiency of Farming Sector SAIMAHajra ANo ratings yet

- Impact of Agricultural Credit On Product PDFDocument5 pagesImpact of Agricultural Credit On Product PDFHajra ANo ratings yet

- Role of Agricultural Credit On Production Efficiency of Farming Sector SAIMADocument7 pagesRole of Agricultural Credit On Production Efficiency of Farming Sector SAIMAHajra ANo ratings yet

- Managerial Economics Ass2Document5 pagesManagerial Economics Ass2Hajra ANo ratings yet

- Bulb OutlineDocument1 pageBulb OutlineHajra ANo ratings yet

- Literature ReviewDocument3 pagesLiterature ReviewHajra ANo ratings yet

- Magoosh GRE Math Formula EbookDocument33 pagesMagoosh GRE Math Formula EbookLavina D'costa100% (1)

- Impact of Agricultural Credit On Product PDFDocument5 pagesImpact of Agricultural Credit On Product PDFHajra ANo ratings yet

- Managerial AssignmentDocument5 pagesManagerial AssignmentHajra ANo ratings yet

- Effects of Agricultural Credit On Agriculture OutputDocument21 pagesEffects of Agricultural Credit On Agriculture OutputHajra ANo ratings yet

- Impact of Formal Credit CHNADIO2 PDFDocument7 pagesImpact of Formal Credit CHNADIO2 PDFHajra ANo ratings yet

- Practice Book Math PDFDocument66 pagesPractice Book Math PDFNoureldinYosriNo ratings yet

- Effects of Agricultural Credit On Agriculture OutputDocument21 pagesEffects of Agricultural Credit On Agriculture OutputHajra ANo ratings yet

- Advanced MacroeconomicsDocument2 pagesAdvanced MacroeconomicsHajra ANo ratings yet

- Iowa Turkey Federation PAC - 9743 - ScannedDocument5 pagesIowa Turkey Federation PAC - 9743 - ScannedZach EdwardsNo ratings yet

- BANK MUSCAT-Tariff Eng BookDocument14 pagesBANK MUSCAT-Tariff Eng BookmujeebmuscatNo ratings yet

- Millions of Dollars Except Per-Share DataDocument14 pagesMillions of Dollars Except Per-Share DataAjax0% (1)

- Friendly Aquaponics Financial Proforma For Single 35 X 96 Greenhouse Projections For A SINGLE Species (Lettuce, OR Bok Choi, OR Green Onions Etc)Document3 pagesFriendly Aquaponics Financial Proforma For Single 35 X 96 Greenhouse Projections For A SINGLE Species (Lettuce, OR Bok Choi, OR Green Onions Etc)Juan Carlos FernandezNo ratings yet

- Horgren CH 03Document29 pagesHorgren CH 03Nuke Sekuntum HariyaniNo ratings yet

- Circular Flow of Income MCQDocument4 pagesCircular Flow of Income MCQKishore KintaliNo ratings yet

- Accounting For Business CombinationDocument9 pagesAccounting For Business CombinationArlene Diane OrozcoNo ratings yet

- Financial Analysis Tools and Techniques GuideDocument22 pagesFinancial Analysis Tools and Techniques GuideCamille G.No ratings yet

- Chapter 12. Tool Kit For Cash Flow Estimation and Risk AnalysisDocument4 pagesChapter 12. Tool Kit For Cash Flow Estimation and Risk AnalysisHerlambang PrayogaNo ratings yet

- Personal Share PortfoliosDocument1 pagePersonal Share PortfoliosBruce BarclayNo ratings yet

- Ahn 和 Choi - 2009 - The role of bank monitoring in corporate governancDocument10 pagesAhn 和 Choi - 2009 - The role of bank monitoring in corporate governanczilin LiNo ratings yet

- Manav's Salary SlipDocument1 pageManav's Salary SlipManav Unique WorldNo ratings yet

- Notes On Final Accounts & Journal& Ledger ProblemDocument17 pagesNotes On Final Accounts & Journal& Ledger ProblemSaiVenkatNo ratings yet

- Assessment of Credit Risk Management in Micro Finance Institutions: A Case of Adama Town Mfis, EthiopiaDocument13 pagesAssessment of Credit Risk Management in Micro Finance Institutions: A Case of Adama Town Mfis, EthiopiaHunde gutemaNo ratings yet

- Sol Q5Document3 pagesSol Q5Shubham RankaNo ratings yet

- Derivative Analysis and Valuation TechniquesDocument32 pagesDerivative Analysis and Valuation TechniquesMukunda HandeNo ratings yet

- Security Bank & Trust Company vs. Cuenca PDFDocument46 pagesSecurity Bank & Trust Company vs. Cuenca PDFRogie ApoloNo ratings yet

- Working Capital ManagementDocument82 pagesWorking Capital ManagementAnacristina PincaNo ratings yet

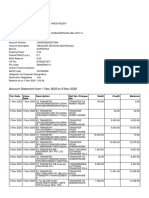

- Account Statement From 1 Nov 2020 To 9 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Nov 2020 To 9 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancevinod reddyNo ratings yet

- P 50Document2 pagesP 50Emily DeerNo ratings yet

- Global Model Risk ManagementDocument24 pagesGlobal Model Risk ManagementrichdevNo ratings yet

- Tax Invoice / Bill of SupplyDocument1 pageTax Invoice / Bill of SupplyabhimanyuNo ratings yet

- Chapter 7 - Regular Output VATDocument17 pagesChapter 7 - Regular Output VATSelene DimlaNo ratings yet

- Funded NextDocument1 pageFunded NextSathya PrakashNo ratings yet

- 0452 s12 QP 22Document20 pages0452 s12 QP 22Faisal RaoNo ratings yet

- Block 2Document90 pagesBlock 2G RAVIKISHORENo ratings yet