You might also like

- CPAR Auditing TheoryDocument62 pagesCPAR Auditing TheoryKeannu Lewis Vidallo96% (46)

- Assignment of Debt Agreement ClsDocument3 pagesAssignment of Debt Agreement ClsSelena Express100% (2)

- Non Current Asset Questions For ACCADocument11 pagesNon Current Asset Questions For ACCAAiril RazaliNo ratings yet

- Financial Accounting Problems: Problem I (Current Assets)Document21 pagesFinancial Accounting Problems: Problem I (Current Assets)Fery AnnNo ratings yet

- Unit I - Audit of Investment Property - Final - t31314Document11 pagesUnit I - Audit of Investment Property - Final - t31314Jake Bundok50% (2)

- GOSI Contribution CalculationDocument10 pagesGOSI Contribution CalculationMohamed Shanab100% (1)

- Bid Strategy & TacticsDocument15 pagesBid Strategy & TacticsRashmi Ranjan Panigrahi67% (3)

- 84 Solinap V Del RosarioDocument1 page84 Solinap V Del Rosarioluigimanzanares100% (1)

- 3rd On-Line Quiz - Substantive Test For CashDocument3 pages3rd On-Line Quiz - Substantive Test For CashMJ YaconNo ratings yet

- Applied Auditing Audit of Receivables Problem 1: QuestionsDocument9 pagesApplied Auditing Audit of Receivables Problem 1: QuestionsPau SantosNo ratings yet

- Chapter 01 - Auditing and Assurance ServicesDocument74 pagesChapter 01 - Auditing and Assurance ServicesBettina OsterfasticsNo ratings yet

- Applied Auditing Report (Audit of Receivables)Document7 pagesApplied Auditing Report (Audit of Receivables)mary louise magana100% (1)

- CHAPTER 8 - Audit of Liabilities: Problem 1Document27 pagesCHAPTER 8 - Audit of Liabilities: Problem 1Chinee CastilloNo ratings yet

- Cost2 1 PDF FreeDocument9 pagesCost2 1 PDF FreeIT GAMING100% (1)

- 520-FinalllDocument38 pages520-FinalllHatake KakashiNo ratings yet

- MODAUD1 UNIT 4 Audit of Inventories PDFDocument9 pagesMODAUD1 UNIT 4 Audit of Inventories PDFJoey WassigNo ratings yet

- 10.28.2017 MT (Audit of Receivables)Document7 pages10.28.2017 MT (Audit of Receivables)PatOcampo100% (1)

- 01 - Audit of Cash & Cash EquivalentsDocument4 pages01 - Audit of Cash & Cash EquivalentsEARL JOHN RosalesNo ratings yet

- AssignmentDocument6 pagesAssignmentIryne Kim PalatanNo ratings yet

- IntAcct Cash CashEquivalents 1Document3 pagesIntAcct Cash CashEquivalents 1Arkhie DavocolNo ratings yet

- Auditing TheoryDocument13 pagesAuditing TheoryRaven GarciaNo ratings yet

- Far 102 - Cash and Cash EquivalentsDocument4 pagesFar 102 - Cash and Cash EquivalentsKeanna Denise GonzalesNo ratings yet

- AP 2020 - Inventories 2Document9 pagesAP 2020 - Inventories 2Heinie Joy PauleNo ratings yet

- CPAR Fringe Benefits (Batch 90) - HandoutDocument13 pagesCPAR Fringe Benefits (Batch 90) - HandoutAljur SalamedaNo ratings yet

- Cash To Inventory Reviewer 1Document15 pagesCash To Inventory Reviewer 1Patricia Camille AustriaNo ratings yet

- Auditing 1 Final ExamDocument8 pagesAuditing 1 Final ExamEdemson NavalesNo ratings yet

- Activity - Audit of InventoryDocument2 pagesActivity - Audit of InventoryRyan DueÑas GuevarraNo ratings yet

- Months To Go Until They MatureDocument5 pagesMonths To Go Until They MatureJude SantosNo ratings yet

- Nfjpia Nmbe Far 2017 AnsDocument9 pagesNfjpia Nmbe Far 2017 AnsSamieeNo ratings yet

- Audit Problems FinalDocument48 pagesAudit Problems FinalShane TabunggaoNo ratings yet

- Chapter 5 Audit of InventoryDocument10 pagesChapter 5 Audit of InventoryMarkie GrabilloNo ratings yet

- Aud ThEORY 2nd PreboardDocument11 pagesAud ThEORY 2nd PreboardJeric TorionNo ratings yet

- Test Bank - 02012021Document13 pagesTest Bank - 02012021Charisse AbordoNo ratings yet

- Chapter 6 Quiz KeyDocument3 pagesChapter 6 Quiz Keymar8357No ratings yet

- Ms 03 - CVP AnalysisDocument10 pagesMs 03 - CVP AnalysisDin Rose GonzalesNo ratings yet

- Review of Accounting ProcessDocument2 pagesReview of Accounting ProcessSeanNo ratings yet

- Audit of Cash and Cash EquivalentsDocument9 pagesAudit of Cash and Cash Equivalentspatricia100% (1)

- Unit 1 Erica Abegonia Sec Code 416 Exercise 1Document2 pagesUnit 1 Erica Abegonia Sec Code 416 Exercise 1Ivan AnaboNo ratings yet

- Auditing ProblemsDocument6 pagesAuditing ProblemsMaurice AgbayaniNo ratings yet

- Case #1: Book BankDocument40 pagesCase #1: Book BankJohn Lloyd YastoNo ratings yet

- AGS CUP 6 Auditing Elimination RoundDocument17 pagesAGS CUP 6 Auditing Elimination RoundKenneth RobledoNo ratings yet

- Adv 1 - Dept 2010Document16 pagesAdv 1 - Dept 2010Aldrin100% (1)

- National Federation of Junior Philipinne Institute of Accountants - National Capital Region Auditing (Aud)Document14 pagesNational Federation of Junior Philipinne Institute of Accountants - National Capital Region Auditing (Aud)Tricia Jen TobiasNo ratings yet

- Audit of Cash and Cash Equivalents PDFDocument4 pagesAudit of Cash and Cash Equivalents PDFRandyNo ratings yet

- Auditing Practice Problem 2Document1 pageAuditing Practice Problem 2Jessa Gay Cartagena TorresNo ratings yet

- JPIA Financial Accounting 1 (Prelims)Document20 pagesJPIA Financial Accounting 1 (Prelims)Kristienalyn De AsisNo ratings yet

- ReviewerDocument43 pagesReviewergnim1520No ratings yet

- Audit of ReceivablesDocument2 pagesAudit of ReceivablesCarmelaNo ratings yet

- Afar 106 - Home Office and Branch Accounting PDFDocument3 pagesAfar 106 - Home Office and Branch Accounting PDFReyn Saplad PeralesNo ratings yet

- Cash With Cash EqualantDocument5 pagesCash With Cash EqualantkaviyapriyaNo ratings yet

- Auditing TheoryDocument11 pagesAuditing Theoryfnyeko100% (1)

- ACC460Document6 pagesACC460Samantha SchumacherNo ratings yet

- AP 5906q ReceivablesDocument3 pagesAP 5906q ReceivablesJulia MirhanNo ratings yet

- Correction of ErrorsDocument6 pagesCorrection of ErrorsJanjielyn MoralesNo ratings yet

- Chapter 14Document32 pagesChapter 14faye anneNo ratings yet

- Aaca Receivables and Sales ReviewerDocument13 pagesAaca Receivables and Sales ReviewerLiberty NovaNo ratings yet

- CHAPTER 10 - Pre-Board ExaminationsDocument34 pagesCHAPTER 10 - Pre-Board Examinationsmjc24No ratings yet

- AFAR - Part 2Document13 pagesAFAR - Part 2Myrna Laquitan100% (1)

- Audit of CashDocument1 pageAudit of CashXandae MempinNo ratings yet

- Fear and Risk in Audit Process PDFDocument25 pagesFear and Risk in Audit Process PDFElena DobreNo ratings yet

- Exercises On Cash PDFDocument6 pagesExercises On Cash PDFFely MaataNo ratings yet

- Multiple Choic1Document4 pagesMultiple Choic1stillwinmsNo ratings yet

- Ch07 Audit Planning Assessment of Control Risk1Document26 pagesCh07 Audit Planning Assessment of Control Risk1Mary GarciaNo ratings yet

- Unit 2 - Cash and Cash EquivalentsDocument8 pagesUnit 2 - Cash and Cash EquivalentsJeremy Jess ArizabalNo ratings yet

- Unit 2. CashDocument8 pagesUnit 2. CashDaphne100% (1)

- Jan 2015 (Manila) ,: Holidays in PhilippinesDocument1 pageJan 2015 (Manila) ,: Holidays in PhilippinesJake BundokNo ratings yet

- Calendar - 2015 02 01 - 2015 03 01 PDFDocument1 pageCalendar - 2015 02 01 - 2015 03 01 PDFJake BundokNo ratings yet

- At Reviewer Part II - (May 2015 Batch)Document22 pagesAt Reviewer Part II - (May 2015 Batch)Jake BundokNo ratings yet

- AP 5904 InvestmentsDocument9 pagesAP 5904 InvestmentsJake BundokNo ratings yet

- Debt Securities: BondsDocument9 pagesDebt Securities: BondsCorinne GohocNo ratings yet

- Dlsu Thesis Paper LetterheadDocument1 pageDlsu Thesis Paper LetterheadJake BundokNo ratings yet

- REVIEW QUESTIONS Investment in Debt SecuritiesDocument1 pageREVIEW QUESTIONS Investment in Debt SecuritiesJake BundokNo ratings yet

- AP 5904 InvestmentsDocument9 pagesAP 5904 InvestmentsJake BundokNo ratings yet

- Unit II - Audit of Intangibles and Other Assets - Final - t31314Document9 pagesUnit II - Audit of Intangibles and Other Assets - Final - t31314Jake BundokNo ratings yet

- MODAUD1 UNIT 6 - Audit of InvestmentsDocument7 pagesMODAUD1 UNIT 6 - Audit of InvestmentsJake BundokNo ratings yet

- Seitani (2013) Toolkit For DSGEDocument27 pagesSeitani (2013) Toolkit For DSGEJake BundokNo ratings yet

- X Deal FoodDocument1 pageX Deal FoodJake BundokNo ratings yet

- (169472718) MODAUD1 UNIT 1 - Analysis and Correction of ErrorsDocument5 pages(169472718) MODAUD1 UNIT 1 - Analysis and Correction of ErrorsJervin LabroNo ratings yet

- MODAUD1 UNIT 3 - Audit of ReceivablesDocument11 pagesMODAUD1 UNIT 3 - Audit of ReceivablesJake BundokNo ratings yet

- MODAUD1 UNIT 4 - Audit of Inventories PDFDocument9 pagesMODAUD1 UNIT 4 - Audit of Inventories PDFJake BundokNo ratings yet

- MODAUD1 UNIT 5 - Audit of Biological AssetsDocument5 pagesMODAUD1 UNIT 5 - Audit of Biological AssetsJake BundokNo ratings yet

- Methods of Evaluating Capital InvestmentsDocument5 pagesMethods of Evaluating Capital InvestmentsJake BundokNo ratings yet

- ObliCon Case DigestDocument8 pagesObliCon Case DigestJohn Waltz SuanNo ratings yet

- June 2011 Results PresentationDocument17 pagesJune 2011 Results PresentationOladipupo Mayowa PaulNo ratings yet

- Reserva TroncalDocument5 pagesReserva TroncalInter_vivosNo ratings yet

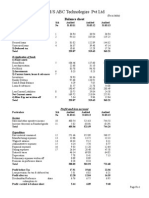

- Balance Sheet of M/S ABC Technologies PVT LTDDocument3 pagesBalance Sheet of M/S ABC Technologies PVT LTDSmitha RajNo ratings yet

- Ch14 - 2015Document86 pagesCh14 - 2015lawrence hNo ratings yet

- Harmer v. CIR, 10th Cir. (2001)Document6 pagesHarmer v. CIR, 10th Cir. (2001)Scribd Government DocsNo ratings yet

- Resume of KarencoslinDocument3 pagesResume of Karencoslinapi-24131152No ratings yet

- BSPLDocument2 pagesBSPLrohitrgsNo ratings yet

- G.G. Sportswear Manufacturing Corp. vs. Banco de Oro Unibank, Inc.Document2 pagesG.G. Sportswear Manufacturing Corp. vs. Banco de Oro Unibank, Inc.kdescallarNo ratings yet

- GenMath Week 1 10Document90 pagesGenMath Week 1 10Noni Montalbo100% (1)

- Jonsay vs. Solidbank Corporation Now MetropolitanBank and Trust CompanyDocument43 pagesJonsay vs. Solidbank Corporation Now MetropolitanBank and Trust CompanyAnnaNo ratings yet

- Balance SheetDocument7 pagesBalance Sheetmhrscribd014No ratings yet

- Foreclosure Benchbook 2 0 - Foreclosure CLE 6-27-11Document64 pagesForeclosure Benchbook 2 0 - Foreclosure CLE 6-27-11Christopher Martin100% (1)

- Weaknesses of Stock Market of IndiaDocument2 pagesWeaknesses of Stock Market of Indiachronicler92100% (1)

- FM - Bankruptcy, Reorganization and LiquidationDocument17 pagesFM - Bankruptcy, Reorganization and LiquidationpandanarangNo ratings yet

- Direct and Indirect InvestmentDocument3 pagesDirect and Indirect InvestmentShariful IslamNo ratings yet

- Alex G Baraona BIO For Salvador Holdings International CorporationDocument7 pagesAlex G Baraona BIO For Salvador Holdings International CorporationAlexGBaraonaNo ratings yet

- Kuenzle & StreiffDocument2 pagesKuenzle & Streiffaerwincarlo4834No ratings yet

- Benefits of Mortgage Refinancing You Must KnowDocument3 pagesBenefits of Mortgage Refinancing You Must KnowriyaNo ratings yet

- TAX Digests Cases BenefitsDocument7 pagesTAX Digests Cases BenefitsRomhead SJNo ratings yet

- Recruitment Process of Brac Bank LimitedDocument60 pagesRecruitment Process of Brac Bank LimitedSabyasachi BosuNo ratings yet

- Naguit vs. Court of Appeals G.R. No. 118375 CASE DIGESTDocument1 pageNaguit vs. Court of Appeals G.R. No. 118375 CASE DIGESTLBitzNo ratings yet

- NFLPA 2014 Dept of Labor LM-2 Part 1Document93 pagesNFLPA 2014 Dept of Labor LM-2 Part 1Robert LeeNo ratings yet

- 5.TN Treasury Code Vol1 77-150Document74 pages5.TN Treasury Code Vol1 77-150Porkodi SengodanNo ratings yet

- CF Assignment 1Document4 pagesCF Assignment 1Kashif KhurshidNo ratings yet