You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Far - 1st Quiz Midterm - Ay 2019-2020Document1 pageFar - 1st Quiz Midterm - Ay 2019-2020Renalyn Paras33% (3)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Excel-Based Model To Value Firms Experiencing Financial DistressDocument4 pagesExcel-Based Model To Value Firms Experiencing Financial DistressgenergiaNo ratings yet

- At 03 Introduction To Public Accountancy PDFDocument5 pagesAt 03 Introduction To Public Accountancy PDFMadelyn Jane IgnacioNo ratings yet

- At 04 Audit Evidence and Audit Documentation PDFDocument6 pagesAt 04 Audit Evidence and Audit Documentation PDFMadelyn Jane IgnacioNo ratings yet

- At 05 Preliminary Engagement Activities PDFDocument4 pagesAt 05 Preliminary Engagement Activities PDFMadelyn Jane IgnacioNo ratings yet

- Afar Midterm Major Exam Key Answer PDFDocument4 pagesAfar Midterm Major Exam Key Answer PDFMadelyn Jane IgnacioNo ratings yet

- Introduction To Financial Statements AuditDocument6 pagesIntroduction To Financial Statements AuditMadelyn Jane IgnacioNo ratings yet

- Chapter 2 Estate TaxDocument4 pagesChapter 2 Estate TaxMadelyn Jane IgnacioNo ratings yet

- Chapter 1 Consumption TaxDocument5 pagesChapter 1 Consumption TaxMadelyn Jane IgnacioNo ratings yet

- Chapter 2 Exempt ImportationsDocument2 pagesChapter 2 Exempt ImportationsMadelyn Jane IgnacioNo ratings yet

- 12943Document4 pages12943Madelyn Jane IgnacioNo ratings yet

- F 3949 ADocument3 pagesF 3949 Aiamsomedude100% (3)

- Las - Week 3.fabm II.Document21 pagesLas - Week 3.fabm II.Jason Tagapan GullaNo ratings yet

- TaxationDocument15 pagesTaxationHani NazrinaNo ratings yet

- Payment Payment: Colorado Individual Income Tax Filing GuideDocument40 pagesPayment Payment: Colorado Individual Income Tax Filing Guidestop recordsNo ratings yet

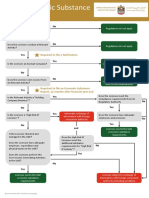

- Flowchart: Required To File A NotificationDocument2 pagesFlowchart: Required To File A NotificationSajidZiaNo ratings yet

- Sneakers SolutionDocument7 pagesSneakers SolutionRamesh Singh100% (1)

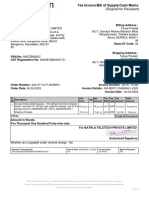

- InvoiceDocument1 pageInvoiceArvind KumarNo ratings yet

- Compromise Penalty RMO 7 2015Document12 pagesCompromise Penalty RMO 7 2015Bernadette JaoNo ratings yet

- The Apple Case: An Irish PerspectiveDocument1 pageThe Apple Case: An Irish PerspectivetyjhgdNo ratings yet

- Onnorokom Solutions LTDDocument3 pagesOnnorokom Solutions LTDYeamin KaziNo ratings yet

- Wuxi Marriott Hotel Lihu Lake S JaiswalDocument1 pageWuxi Marriott Hotel Lihu Lake S JaiswalShubhranshu JaiswalNo ratings yet

- Form PDF 379730120021023Document9 pagesForm PDF 379730120021023parwindersingh9066No ratings yet

- E-Way Bill - TamDocument1 pageE-Way Bill - TamPrashant GuptaNo ratings yet

- Mayer Islamization and Taxation in PakistanDocument23 pagesMayer Islamization and Taxation in PakistanKashif Ali Khan SherwaniNo ratings yet

- CIR Vs CADocument1 pageCIR Vs CAJazem AnsamaNo ratings yet

- Student List RSDocument6 pagesStudent List RSIfa ChanNo ratings yet

- Full and Final Payment 1Document1 pageFull and Final Payment 1AaaaNo ratings yet

- Particulars Amount Particulars Amount: Trading Account FormatDocument4 pagesParticulars Amount Particulars Amount: Trading Account FormatSaravananSrvnNo ratings yet

- InvoiceDocument1 pageInvoicetanya.prasadNo ratings yet

- Gaytor C04 v4Document12 pagesGaytor C04 v4gpm-81100% (1)

- Omnia 301-044959 Payslip 20191031 26 PDFDocument1 pageOmnia 301-044959 Payslip 20191031 26 PDFMilkovic DinoNo ratings yet

- Tax Mod 3Document7 pagesTax Mod 3Ayushi TiwariNo ratings yet

- BAM 127 Day 14 - TGDocument9 pagesBAM 127 Day 14 - TGPaulo BelenNo ratings yet

- Benefit Illustration: UIN: 104N116V02 Page 1 of 3Document3 pagesBenefit Illustration: UIN: 104N116V02 Page 1 of 3Ravindar aNo ratings yet

- AO Code Search For TANDocument1 pageAO Code Search For TANSubhashis DasNo ratings yet

- Domingo Vs GarlitosDocument1 pageDomingo Vs Garlitossally deeNo ratings yet

- Tax Sale ListingsDocument18 pagesTax Sale ListingsmmelhamNo ratings yet

- TUA Income Tax Course SyllabusDocument5 pagesTUA Income Tax Course SyllabusFerdinand Caralde Narciso ImportadoNo ratings yet