You might also like

- Brochuredocument OSP 202308030651PM891 PDFDocument23 pagesBrochuredocument OSP 202308030651PM891 PDFhaseebamerNo ratings yet

- GIP Sales BrochureDocument15 pagesGIP Sales BrochureSiva NandNo ratings yet

- Insurance Ia 2Document6 pagesInsurance Ia 2Vikrant SinghNo ratings yet

- Max Life Saral Jeevan Bima ProspectusDocument9 pagesMax Life Saral Jeevan Bima Prospectusmohan krishnaNo ratings yet

- GSIP BrochureDocument2 pagesGSIP Brochureabdul.nm4064No ratings yet

- Max Life Super Term Plan Prospectus PDFDocument12 pagesMax Life Super Term Plan Prospectus PDFFood Supply Headquarter ChandigarhNo ratings yet

- Lifetime Super Pension: Benefits in DetailDocument4 pagesLifetime Super Pension: Benefits in DetailSathish KumarNo ratings yet

- 2.whole Life PlansDocument3 pages2.whole Life PlansKoshyNo ratings yet

- Eprotect BrochureDocument13 pagesEprotect BrochureAbhishek RamNo ratings yet

- Secure Income PlanDocument15 pagesSecure Income PlanSuyash PrasadNo ratings yet

- Life Gain Premier BrochureDocument12 pagesLife Gain Premier BrochureNeeralNo ratings yet

- Kotak Assured Income PlanDocument9 pagesKotak Assured Income Plandinesh2u85No ratings yet

- LIC - New Tech Term - Sales BrochureDocument11 pagesLIC - New Tech Term - Sales BrochureRahul ChauhanNo ratings yet

- 825 E-Term 288V01 SLDocument5 pages825 E-Term 288V01 SLIncredible MediaNo ratings yet

- ICICI Savings Suraksha BrochureDocument8 pagesICICI Savings Suraksha BrochureJetesh DevgunNo ratings yet

- HDFC Life Super Income Plan SHAREDocument6 pagesHDFC Life Super Income Plan SHARESandeep MookerjeeNo ratings yet

- Ko Tak Term PlanDocument8 pagesKo Tak Term PlanRKNo ratings yet

- Insurance Policy Consultancy: Banking and Insurance - CIA 3Document11 pagesInsurance Policy Consultancy: Banking and Insurance - CIA 3Mehraan ZoroofchiNo ratings yet

- Max Life Monthly Income Advantage Plan ProspectusDocument11 pagesMax Life Monthly Income Advantage Plan Prospectushemantchawla89No ratings yet

- MM AssignmentDocument16 pagesMM AssignmentRahul ParasharNo ratings yet

- Consumer Preference Towards Shriram Life Insurance CompanyDocument18 pagesConsumer Preference Towards Shriram Life Insurance Companyprava vamsiNo ratings yet

- Sales Brochure LIC-s E-Term Rev PDFDocument3 pagesSales Brochure LIC-s E-Term Rev PDFRamesh ThumburuNo ratings yet

- Term Life Insurance FinalDocument10 pagesTerm Life Insurance FinalsearchingnobodyNo ratings yet

- KFD U39Document3 pagesKFD U39mniarunNo ratings yet

- Savings Assurance PlanDocument1 pageSavings Assurance Planrajeshdubey7No ratings yet

- Life Insurance Corporation Pension PlusDocument9 pagesLife Insurance Corporation Pension PlusAmitabh AnandNo ratings yet

- PNB Metlife Smart Pletinium PlanDocument5 pagesPNB Metlife Smart Pletinium PlanPurnima PurohitNo ratings yet

- Nitish Arora Banking3Document20 pagesNitish Arora Banking3nitisharora116No ratings yet

- Future Generali Long Term Income Plan (UIN - 133N090V01) Individual, Non-Linked, Non-Participating (Without Profits), Savings, Life Insurance PlanDocument8 pagesFuture Generali Long Term Income Plan (UIN - 133N090V01) Individual, Non-Linked, Non-Participating (Without Profits), Savings, Life Insurance PlanHSNo ratings yet

- Sales Brochure LIC S Single Premium Endowment PlanDocument9 pagesSales Brochure LIC S Single Premium Endowment Plansantosh kumarNo ratings yet

- Term Protector Product Summary: Important NoteDocument8 pagesTerm Protector Product Summary: Important NotesoxoNo ratings yet

- Bima Nivesh Triple Cover Table NoDocument3 pagesBima Nivesh Triple Cover Table Noravirawat15No ratings yet

- ICICI Pru Assure WealthDocument2 pagesICICI Pru Assure WealthPavan Kumar RanguduNo ratings yet

- Fulfil The Smaller Joys in Life, Through Regular IncomeDocument8 pagesFulfil The Smaller Joys in Life, Through Regular IncomeSajeed ShaikhNo ratings yet

- SM RT: DHFL Pramerica Smart Income, A Non-Participating Endowment Insurance PlanDocument4 pagesSM RT: DHFL Pramerica Smart Income, A Non-Participating Endowment Insurance PlankulaseraNo ratings yet

- Jeev Anankur-807 - CircularDocument8 pagesJeev Anankur-807 - CircularKamlesh Kumar Mandal100% (1)

- Reating Lif: Child Protection Money Back PlanDocument2 pagesReating Lif: Child Protection Money Back PlanSanjay Ku AgrawalNo ratings yet

- EProtect BrochureDocument13 pagesEProtect Brochurehyhy 21No ratings yet

- Sales Brochure LIC S Saral PensionDocument10 pagesSales Brochure LIC S Saral PensionKshitij KumarNo ratings yet

- Jeevan VriddhiDocument4 pagesJeevan VriddhihemukariaNo ratings yet

- Contact Your Agent/Branch or Visit Our Website WWW - Licindia.in or SMS YOUR CITY NAME TO 56767474 (Eg. MUMBAI)Document12 pagesContact Your Agent/Branch or Visit Our Website WWW - Licindia.in or SMS YOUR CITY NAME TO 56767474 (Eg. MUMBAI)RustyNo ratings yet

- Sales Brochure - LIC S New Children S Money Back PlanDocument11 pagesSales Brochure - LIC S New Children S Money Back Planamit_saxena_10No ratings yet

- Max Life Guaranteed Income Plan Prospectus PDFDocument14 pagesMax Life Guaranteed Income Plan Prospectus PDFRishi MitraNo ratings yet

- Name: Vikrant Singh Tomar USN: 19MBAR0331 Sec:MF2 Subject: Insurance Assignment-02Document6 pagesName: Vikrant Singh Tomar USN: 19MBAR0331 Sec:MF2 Subject: Insurance Assignment-02Vikrant SinghNo ratings yet

- Lic'S Bima Account - I (Plan No. 805) (UIN: 512N263V01)Document8 pagesLic'S Bima Account - I (Plan No. 805) (UIN: 512N263V01)Niten GuptaNo ratings yet

- Dhan Vriddhi English Sales BrochureDocument16 pagesDhan Vriddhi English Sales BrochureNimesh PrakashNo ratings yet

- Aegon Life Akhil Bharat Term PlanDocument9 pagesAegon Life Akhil Bharat Term Planmohinlaskar123No ratings yet

- LIC - Amritbaal - Brochure - 4 Inch X 9 Inch - Eng - Single PGDocument20 pagesLIC - Amritbaal - Brochure - 4 Inch X 9 Inch - Eng - Single PGsrajdinesh94No ratings yet

- Igain Iii - Investment Plan: FeaturesDocument8 pagesIgain Iii - Investment Plan: FeaturesShankar VasuNo ratings yet

- Term Paper of BankingDocument22 pagesTerm Paper of BankingnidhijunejaNo ratings yet

- Power Your Independent Retirement.: WWW - Sbilife.co - inDocument20 pagesPower Your Independent Retirement.: WWW - Sbilife.co - injithin jayNo ratings yet

- Secure Income Plan BrochureDocument18 pagesSecure Income Plan Brochuremantoo kumarNo ratings yet

- IllustrationFormat PrashantDocument8 pagesIllustrationFormat PrashantBhavesh ShuklaNo ratings yet

- Money Back PlusDocument4 pagesMoney Back Plusvek80No ratings yet

- IRM Final FileDocument10 pagesIRM Final FileSubham ChoudhuryNo ratings yet

- Life Partner Plus Pay Endowment To Age 75 NewDocument6 pagesLife Partner Plus Pay Endowment To Age 75 NewshamaritesNo ratings yet

- Lic Brochure 917 Single Endoment Plan 2021Document12 pagesLic Brochure 917 Single Endoment Plan 2021राजकुमार पटेल स्वदेशी प्रचारकNo ratings yet

- Textbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterFrom EverandTextbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterNo ratings yet

- Infinite Banking Secrets for Tax-Free Retirement: A Beginner's Guide: How to invest in Real Estate with Infinite BankingFrom EverandInfinite Banking Secrets for Tax-Free Retirement: A Beginner's Guide: How to invest in Real Estate with Infinite BankingNo ratings yet

- Finiii MaDocument311 pagesFiniii MamanishaNo ratings yet

- Unit 3 - Foreign Exchange MarketDocument3 pagesUnit 3 - Foreign Exchange MarketmanishaNo ratings yet

- 062021T000042537 ContractNotes TaxInvoiceDocument1 page062021T000042537 ContractNotes TaxInvoicemanishaNo ratings yet

- Form For Evidence of Payment of Securities Transaction Tax On Transactions Entered in A Recognised Stock ExchangeDocument2 pagesForm For Evidence of Payment of Securities Transaction Tax On Transactions Entered in A Recognised Stock ExchangemanishaNo ratings yet

- Unit 1 So FarDocument4 pagesUnit 1 So FarmanishaNo ratings yet

- House No 1073 Sector 43 B Chandigarh Sector 22 Chandigarh CHANDIGARH - CHA - 160022 Chandigarh, IndiaDocument1 pageHouse No 1073 Sector 43 B Chandigarh Sector 22 Chandigarh CHANDIGARH - CHA - 160022 Chandigarh, IndiamanishaNo ratings yet

- Unit 19 Factoring, Forfaiting and Bill Discounting: ObjectivesDocument20 pagesUnit 19 Factoring, Forfaiting and Bill Discounting: ObjectivesmanishaNo ratings yet

- Examination Prep Guide: Certified Treasury ProfessionalDocument24 pagesExamination Prep Guide: Certified Treasury ProfessionalmanishaNo ratings yet

- Form For Evidence of Payment of Securities Transaction Tax On Transactions Entered in A Recognised Stock ExchangeDocument2 pagesForm For Evidence of Payment of Securities Transaction Tax On Transactions Entered in A Recognised Stock ExchangemanishaNo ratings yet

- Final AFSTDocument7 pagesFinal AFSTCatherine ValdezNo ratings yet

- Private Public and Global EnterprisesDocument23 pagesPrivate Public and Global EnterprisesusethNo ratings yet

- 13 - Tax Law - Customs Law - 271219Document25 pages13 - Tax Law - Customs Law - 271219Sushil BansalNo ratings yet

- NPV Irr MCQDocument6 pagesNPV Irr MCQMM Fakhrul Islam0% (1)

- Sapm Project ReportDocument25 pagesSapm Project ReportAdarshNo ratings yet

- Confirmation of Your Hotel Reservation - Ibis Budget Phnom Penh Riverside (Cambodia), 02 06 23 - 06 06 23 Process Number 163017975Document1 pageConfirmation of Your Hotel Reservation - Ibis Budget Phnom Penh Riverside (Cambodia), 02 06 23 - 06 06 23 Process Number 163017975Thangadurai SureshNo ratings yet

- SYBCO AC FIN Financial Accounting Special Accounting Areas IIIDocument249 pagesSYBCO AC FIN Financial Accounting Special Accounting Areas IIIctfworkshop2020No ratings yet

- Project Cost Estimating Manual Third Edition PDFDocument83 pagesProject Cost Estimating Manual Third Edition PDFYanning LiNo ratings yet

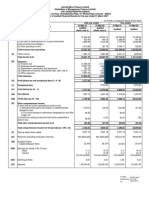

- Kangra Central Cooperative Bank Report 2016-17 Pankajrana209@Document54 pagesKangra Central Cooperative Bank Report 2016-17 Pankajrana209@pankaj91% (11)

- ERP Financials: SAP FICO Transaction CodesDocument24 pagesERP Financials: SAP FICO Transaction CodesAnand DuttaNo ratings yet

- AFA® (Accredited Financial Analyst®) Is One of The Most Highly Valued Qualifications AvailableDocument3 pagesAFA® (Accredited Financial Analyst®) Is One of The Most Highly Valued Qualifications AvailableLina Dela Pena FurucNo ratings yet

- BDO Canada - Summary - IFRS-16Document7 pagesBDO Canada - Summary - IFRS-16Ernest IpNo ratings yet

- IB Econ Chap 16 Macro EQDocument11 pagesIB Econ Chap 16 Macro EQsweetlunaticNo ratings yet

- Banking Laws - DizonDocument26 pagesBanking Laws - DizonZsa-shimi FranciscoNo ratings yet

- Financing Sustainable Infrastructure in Latin America and The Caribbean Market Development and Recommendations PDFDocument171 pagesFinancing Sustainable Infrastructure in Latin America and The Caribbean Market Development and Recommendations PDFHector Castellanos VillalpandoNo ratings yet

- Chapter 1 SolutionsDocument44 pagesChapter 1 Solutionsaevium0% (1)

- 2 Financial Accounting ReportingDocument5 pages2 Financial Accounting ReportingBizness Zenius HantNo ratings yet

- (In Lakhs, Except Per Equity Share Data) : Digitally Signed Bysvraja VaidyanathanDocument9 pages(In Lakhs, Except Per Equity Share Data) : Digitally Signed Bysvraja VaidyanathanAnamika NandiNo ratings yet

- Powers: Powers, Duties & Liabilities of Board of Directors of A Company in IndiaDocument7 pagesPowers: Powers, Duties & Liabilities of Board of Directors of A Company in IndiaVinay SinghNo ratings yet

- Notice of Allodial Cost Schedule (Template) PDFDocument7 pagesNotice of Allodial Cost Schedule (Template) PDFAnonymous byf7jsz100% (3)

- Ms SalesDocument41 pagesMs Salesalyza burdeosNo ratings yet

- Corporate Credit Card AgreementDocument5 pagesCorporate Credit Card AgreementmanishNo ratings yet

- FI360 Week 5 SolutionsDocument3 pagesFI360 Week 5 Solutionsrz100% (1)

- F7irl 2010 Dec AnsDocument11 pagesF7irl 2010 Dec AnsNghiêm Thị Mai AnhNo ratings yet

- BIR Ruling No. 370-11 PDFDocument18 pagesBIR Ruling No. 370-11 PDFJuris PasionNo ratings yet

- Industry Reports OverviewDocument43 pagesIndustry Reports OverviewAkshay ChunodkarNo ratings yet

- Applied Economics Power PointDocument213 pagesApplied Economics Power Pointjonathan malasigNo ratings yet

- Angel Broking Limited Minimium Margin Requirement For Futures Contract As Per Span For 31-12-2019Document2 pagesAngel Broking Limited Minimium Margin Requirement For Futures Contract As Per Span For 31-12-2019parthNo ratings yet

- EmanuelEmails 1501-1800Document300 pagesEmanuelEmails 1501-1800CrainsChicagoBusinessNo ratings yet

- McGraw Hill Earnings ReportDocument20 pagesMcGraw Hill Earnings Reportmtpo6No ratings yet