You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- ABM-ENTERPRENUERSHIP 12 - Q1 - W4 - Mod4 PDFDocument15 pagesABM-ENTERPRENUERSHIP 12 - Q1 - W4 - Mod4 PDFjoebert agraviador86% (21)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- International Chamber of Commerce Non-Circumvention, Non-Disclosure & Working Agreement (Ncnda) Irrevocable Master Fee Protection Agreement (Imfpa)Document10 pagesInternational Chamber of Commerce Non-Circumvention, Non-Disclosure & Working Agreement (Ncnda) Irrevocable Master Fee Protection Agreement (Imfpa)Claudio PizzoNo ratings yet

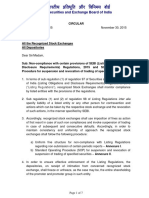

- SEBI Cirular-Non Compliance - 30112015Document7 pagesSEBI Cirular-Non Compliance - 30112015AdityaNo ratings yet

- Disclosure of Reasons For Delay in Submission of Financial Results by Listed EntitiesDocument2 pagesDisclosure of Reasons For Delay in Submission of Financial Results by Listed EntitiesAdityaNo ratings yet

- SEBI BR-Dividend Distribution Policy For Listed CompaniesDocument1 pageSEBI BR-Dividend Distribution Policy For Listed CompaniesAdityaNo ratings yet

- Amendment To Regulation 40 of SEBI (LODR) Regulations, 2015Document1 pageAmendment To Regulation 40 of SEBI (LODR) Regulations, 2015AdityaNo ratings yet

- 140618Document4 pages140618Rohit PurandareNo ratings yet

- Disclosures Regarding Commodity Risks by Listed EntitiesDocument3 pagesDisclosures Regarding Commodity Risks by Listed EntitiesAdityaNo ratings yet

- Schemes of Arrangement by Listed Entities and (Ii) Relaxation Under Sub-Rule (7) of Rule 19 of The Securities Contracts (Regulation) Rules, 1957Document12 pagesSchemes of Arrangement by Listed Entities and (Ii) Relaxation Under Sub-Rule (7) of Rule 19 of The Securities Contracts (Regulation) Rules, 1957Shyam SunderNo ratings yet

- Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) (Amendment) Regulations 2016Document4 pagesSecurities and Exchange Board of India (Listing Obligations and Disclosure Requirements) (Amendment) Regulations 2016Shyam SunderNo ratings yet

- SEBI Circular - Formats For Publishing Financial Results - 30112015 PDFDocument26 pagesSEBI Circular - Formats For Publishing Financial Results - 30112015 PDFAdityaNo ratings yet

- Issue of No Objection Certificate For Release of 1% of Issue AmountDocument1 pageIssue of No Objection Certificate For Release of 1% of Issue AmountShyam SunderNo ratings yet

- SEBI Circular - Disclosure of Holding Securities Demat - 30112015Document10 pagesSEBI Circular - Disclosure of Holding Securities Demat - 30112015AdityaNo ratings yet

- IEPF (Recruitment, Salary and Other T&C of Services of Officers and Other Employees) Rules 2016Document5 pagesIEPF (Recruitment, Salary and Other T&C of Services of Officers and Other Employees) Rules 2016AdityaNo ratings yet

- SEBI Cirular-Manner of Public Shareholding - 30112015Document2 pagesSEBI Cirular-Manner of Public Shareholding - 30112015AdityaNo ratings yet

- Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015.Document2 pagesSecurities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015.Shyam SunderNo ratings yet

- Companies (Registration of Charges) Amendment Rules, 2018Document3 pagesCompanies (Registration of Charges) Amendment Rules, 2018AdityaNo ratings yet

- SEBI Circular - Disclosure of Audit Quali - 27052016Document4 pagesSEBI Circular - Disclosure of Audit Quali - 27052016AdityaNo ratings yet

- 16.FAQs-SEBI (LODR) Regulations, 2015 - 29012016Document7 pages16.FAQs-SEBI (LODR) Regulations, 2015 - 29012016AdityaNo ratings yet

- Securities and Exchange Board of IndiaDocument7 pagesSecurities and Exchange Board of IndiaShyam SunderNo ratings yet

- SEBI Circular - Formats For Publishing Listed Debt Sec or Irr Pref - 27112015Document7 pagesSEBI Circular - Formats For Publishing Listed Debt Sec or Irr Pref - 27112015AdityaNo ratings yet

- SEBI Circular - Formats For Voting Results - 04112015Document2 pagesSEBI Circular - Formats For Voting Results - 04112015AdityaNo ratings yet

- Companies (Registration of Charges) Amendment Rules 2017 - 08042017Document44 pagesCompanies (Registration of Charges) Amendment Rules 2017 - 08042017AdityaNo ratings yet

- Co. (Registration of Charges) Amendment Rules - May 2015Document2 pagesCo. (Registration of Charges) Amendment Rules - May 2015AdityaNo ratings yet

- Securities and Exchange Board of India: CircularDocument13 pagesSecurities and Exchange Board of India: CircularArsh AlamNo ratings yet

- SEBI Circular - Formats For Publishing Listed Securitised Debt Instruments - 27112015 PDFDocument14 pagesSEBI Circular - Formats For Publishing Listed Securitised Debt Instruments - 27112015 PDFAdityaNo ratings yet

- Rules - Co. (Acceptance of Deposits) June 2016Document10 pagesRules - Co. (Acceptance of Deposits) June 2016AdityaNo ratings yet

- Co. (Acceptance of Deposits) Second Amendment Rules, 2015 - Sep 2015 PDFDocument4 pagesCo. (Acceptance of Deposits) Second Amendment Rules, 2015 - Sep 2015 PDFAdityaNo ratings yet

- The Companies (Acceptance of Deposits) Amendment Rules, 2015 - March 2015 PDFDocument13 pagesThe Companies (Acceptance of Deposits) Amendment Rules, 2015 - March 2015 PDFAdityaNo ratings yet

- J. General - Circular - ClarificationSep 2013Document2 pagesJ. General - Circular - ClarificationSep 2013AdityaNo ratings yet

- K. Circular04 - Clarification On App. of Section 16 of CA 2013 For Cases Under CA 1956 - 2017 - 17052017Document1 pageK. Circular04 - Clarification On App. of Section 16 of CA 2013 For Cases Under CA 1956 - 2017 - 17052017AdityaNo ratings yet

- Magic Floor Produces and Sells A Complete Line of FloorDocument2 pagesMagic Floor Produces and Sells A Complete Line of Floortrilocksp SinghNo ratings yet

- Cover 1 4Document4 pagesCover 1 4kumara1986No ratings yet

- Lot 01 Boq Utc Elgon CurrDocument445 pagesLot 01 Boq Utc Elgon CurrAnonymous qOBFvINo ratings yet

- FM II Assignment 12 W22Document2 pagesFM II Assignment 12 W22Farah ImamiNo ratings yet

- Invitational 2020 2ndDocument36 pagesInvitational 2020 2ndÁnh Thiện TriệuNo ratings yet

- Ner 65lc Nit 15sep15Document4 pagesNer 65lc Nit 15sep15vspuriNo ratings yet

- UNIT-5 Controlling Definition of ControllingDocument7 pagesUNIT-5 Controlling Definition of ControllingAishwarya yadavNo ratings yet

- Indian Oil 17Document2 pagesIndian Oil 17Ramesh AnkithaNo ratings yet

- Ch15 SchedulingDocument20 pagesCh15 SchedulingFatemah Maher HegazyNo ratings yet

- Research Methodology and Business AnalyticsDocument27 pagesResearch Methodology and Business Analyticsamarnadh allaNo ratings yet

- WCE ENT504M Environmental Analysis and Opportunity EvaluationDocument14 pagesWCE ENT504M Environmental Analysis and Opportunity EvaluationLevi BlueNo ratings yet

- TRC Tender. 12.03.2024Document84 pagesTRC Tender. 12.03.2024mkudeNo ratings yet

- Islamic Finance SNA BOPDocument89 pagesIslamic Finance SNA BOPOmar MajeedNo ratings yet

- Chapter 5 Complex Group StructuresDocument12 pagesChapter 5 Complex Group StructuresKE XIN NGNo ratings yet

- BUS 1.3 - Financial Awareness - Level 4 AssignmentDocument9 pagesBUS 1.3 - Financial Awareness - Level 4 AssignmentDave PulpulaanNo ratings yet

- HRM Group ProjectDocument13 pagesHRM Group Projectanas ejazNo ratings yet

- Ba Core 6 Pmodule 9Document6 pagesBa Core 6 Pmodule 9Francheska LarozaNo ratings yet

- Us Digital Gambling Halftime Report August 2023Document34 pagesUs Digital Gambling Halftime Report August 2023Antonius VincentNo ratings yet

- Jaegar LivewireDocument3 pagesJaegar LivewirePravesh KumarNo ratings yet

- Morroow Question SolutionDocument4 pagesMorroow Question SolutionDilsa JainNo ratings yet

- Jeonand ChoiDocument12 pagesJeonand ChoiJenny AguilaNo ratings yet

- SERTICA - 7 Challenges in Technical Ship ManagementDocument11 pagesSERTICA - 7 Challenges in Technical Ship ManagementSamuel ChanNo ratings yet

- Lista de Precios de Tuberia 23-7-21 ITECODocument4 pagesLista de Precios de Tuberia 23-7-21 ITECOfelipeNo ratings yet

- 2021-11-09-SWIR - OQ-RBC Capital Markets-Normalizing Following Manufacturing Disruptions-94496714Document14 pages2021-11-09-SWIR - OQ-RBC Capital Markets-Normalizing Following Manufacturing Disruptions-94496714andrewNo ratings yet

- SAP Implementation Project, Rollout Project, Supporting Project, Upgrading ProjectDocument3 pagesSAP Implementation Project, Rollout Project, Supporting Project, Upgrading Projectsrinivasa varmaNo ratings yet

- 2015 SALN Form BLANK 1 Annex 35 For Saln 2022Document2 pages2015 SALN Form BLANK 1 Annex 35 For Saln 2022Bediones Econ ClassNo ratings yet

- Standard, Actual Costing, Normal CostingDocument11 pagesStandard, Actual Costing, Normal Costinghababammar660No ratings yet

- Industrial Court Award PDFDocument47 pagesIndustrial Court Award PDFGunasundaryChandramohan100% (1)