You might also like

- Dividend Investing for Beginners & DummiesFrom EverandDividend Investing for Beginners & DummiesRating: 5 out of 5 stars5/5 (1)

- Film Project Package Prospectus (Template)Document3 pagesFilm Project Package Prospectus (Template)Neil BrimelowNo ratings yet

- Linear Technology Payout Policy Case 3Document4 pagesLinear Technology Payout Policy Case 3Amrinder SinghNo ratings yet

- Mas LectureDocument7 pagesMas Lecturerav danoNo ratings yet

- Ming The Mechanic - The Unknown 20 Trillion Dollar CompanyDocument27 pagesMing The Mechanic - The Unknown 20 Trillion Dollar CompanyJesus BerriosNo ratings yet

- Inter Law MCQs Book PDFDocument63 pagesInter Law MCQs Book PDFShreyans JainNo ratings yet

- DIVIDEND INVESTING: Maximizing Returns while Minimizing Risk through Selective Stock Selection and Diversification (2023 Guide for Beginners)From EverandDIVIDEND INVESTING: Maximizing Returns while Minimizing Risk through Selective Stock Selection and Diversification (2023 Guide for Beginners)No ratings yet

- BBPW3203 731101125021 Financial Management IIDocument18 pagesBBPW3203 731101125021 Financial Management IIVeronica Sadom80% (5)

- A Study On Dividend PolicyDocument75 pagesA Study On Dividend PolicyVeera Bhadra Chary ChNo ratings yet

- DD Icici UppalDocument14 pagesDD Icici Uppalferoz khanNo ratings yet

- Convertible BondsDocument14 pagesConvertible BondsMarissa Villarreal100% (1)

- Corporation Law CasesDocument22 pagesCorporation Law CasesJessica Joyce PenalosaNo ratings yet

- Gitman c14 SG 13geDocument13 pagesGitman c14 SG 13gekarim100% (3)

- LEGASPI y NAVERA Vs People PDFDocument1 pageLEGASPI y NAVERA Vs People PDFethan pulveraNo ratings yet

- Dividend Policy AfmDocument10 pagesDividend Policy AfmPooja NagNo ratings yet

- Pakistani Dividend PolicyDocument2 pagesPakistani Dividend PolicyZeshan MustafaNo ratings yet

- Determinants of Dividend Payout RatioDocument16 pagesDeterminants of Dividend Payout RatioZohaib MalikNo ratings yet

- Types of Dividend PoliciesDocument3 pagesTypes of Dividend PoliciesAlphaNo ratings yet

- Impact of Dividend Policy On A Firm PerformanceDocument11 pagesImpact of Dividend Policy On A Firm PerformanceMuhammad AnasNo ratings yet

- Fin 4050 Term PaperDocument11 pagesFin 4050 Term PaperMark D. KaniaruNo ratings yet

- Discuss The Relevance of Dividend Policy in Financial Decision MakingDocument6 pagesDiscuss The Relevance of Dividend Policy in Financial Decision MakingMichael NyamutambweNo ratings yet

- Dividend Policy of Indian Corporate FirmsDocument19 pagesDividend Policy of Indian Corporate FirmsRoads Sub Division-I,PuriNo ratings yet

- Introduction To Corporate Finance, Megginson, Smart and LuceyDocument6 pagesIntroduction To Corporate Finance, Megginson, Smart and LuceyGvz HndraNo ratings yet

- Assignment Pengurusan Kewangan 2Document13 pagesAssignment Pengurusan Kewangan 2william tangNo ratings yet

- Beximco Chapter 2Document15 pagesBeximco Chapter 2Tanvir Ahmed Rana100% (2)

- Analysis of The Factors in Uencing Dividend Policy: Evidence of Indonesian Listed FirmsDocument10 pagesAnalysis of The Factors in Uencing Dividend Policy: Evidence of Indonesian Listed FirmsChan Hui YanNo ratings yet

- Corporate Finance Assignment No. 1 Topic: Factor Affecting Divivdend PlicyDocument7 pagesCorporate Finance Assignment No. 1 Topic: Factor Affecting Divivdend Plicyanum fatimaNo ratings yet

- Impact of Financial Leverage On Dividend Policy Evidence From Islamabad Stock Exchange Listed CompaniesDocument4 pagesImpact of Financial Leverage On Dividend Policy Evidence From Islamabad Stock Exchange Listed CompaniesSyed Ameer HayderNo ratings yet

- Study of Dividend Payout PatternDocument27 pagesStudy of Dividend Payout PatternVivekNo ratings yet

- Mai Moyo Theory 2 Fin ManDocument4 pagesMai Moyo Theory 2 Fin Manmarvadomarvellous67No ratings yet

- Dividend Policy: Answers To Concept Review QuestionsDocument6 pagesDividend Policy: Answers To Concept Review Questionsmeselu workuNo ratings yet

- Chapter No. 10 Â " Dividend PolicyDocument9 pagesChapter No. 10 Â " Dividend PolicyToaster97No ratings yet

- Analysis On Dividend Payout: Empirical Evidence of Property Companies in MalaysiaDocument11 pagesAnalysis On Dividend Payout: Empirical Evidence of Property Companies in MalaysiaLink LinkNo ratings yet

- Chapter-II Literature ReviewDocument32 pagesChapter-II Literature Reviewbikash ranaNo ratings yet

- The Importance of DividendsDocument4 pagesThe Importance of Dividendssmartravian007No ratings yet

- Dividend Policy": Term Paper - I On Corporate Financial ManagementDocument10 pagesDividend Policy": Term Paper - I On Corporate Financial ManagementbodhikolNo ratings yet

- Impact of Financial Leverage On Dividend Policy of Selected Manufacturing Firms in NigeriaDocument12 pagesImpact of Financial Leverage On Dividend Policy of Selected Manufacturing Firms in NigeriaMayaz AhmedNo ratings yet

- FinmanDocument7 pagesFinmanNHEMIA ELEVENCIONADONo ratings yet

- ResearchDocument21 pagesResearchAizaz AliNo ratings yet

- Module4 Dividend PolicyDocument5 pagesModule4 Dividend PolicyShihad Panoor N KNo ratings yet

- Determinants of Dividend Policy: Evidence From GCC MarketDocument13 pagesDeterminants of Dividend Policy: Evidence From GCC MarketeferemNo ratings yet

- Analysis of The Factors Affecting Devident PolicyDocument12 pagesAnalysis of The Factors Affecting Devident PolicyJung AuLiaNo ratings yet

- Chapter-I: 1.1 Background of The StudyDocument10 pagesChapter-I: 1.1 Background of The StudyAnonymous NpglhCs1JNo ratings yet

- IndianJournalofCorporateGovernance 2015 Roy 1 33Document34 pagesIndianJournalofCorporateGovernance 2015 Roy 1 33mrzia996No ratings yet

- Dividend Policy As Strategic Tool of Financing in Public Firms: Evidence From NigeriaDocument24 pagesDividend Policy As Strategic Tool of Financing in Public Firms: Evidence From Nigeriay_378602342No ratings yet

- Corporate Finance BasicsDocument27 pagesCorporate Finance BasicsAhimbisibwe BenyaNo ratings yet

- Dividend Policy and Firm Performance: A Study of Listed Firms On National Stock ExchangeDocument4 pagesDividend Policy and Firm Performance: A Study of Listed Firms On National Stock ExchangeMUZNANo ratings yet

- Chapter - IDocument14 pagesChapter - Iprabin ghimireNo ratings yet

- "Dividend Decision": Synopsis OnDocument14 pages"Dividend Decision": Synopsis Onferoz khanNo ratings yet

- Impact of Dividend Policy On Share PricesDocument16 pagesImpact of Dividend Policy On Share PricesAli JarralNo ratings yet

- Dividend Policy Analysis For Sun PharmaceuticalsDocument16 pagesDividend Policy Analysis For Sun PharmaceuticalsIshita SoodNo ratings yet

- DividendDocument30 pagesDividendFaruqNo ratings yet

- Dividend PolicyDocument8 pagesDividend PolicyToufiq AmanNo ratings yet

- Factors Affecting Dividend Policy in Manufacturing Companies in Indonesia Stock ExchangeDocument14 pagesFactors Affecting Dividend Policy in Manufacturing Companies in Indonesia Stock ExchangeWindaNo ratings yet

- The Tip of The Iceberg For Dividend StocksDocument6 pagesThe Tip of The Iceberg For Dividend StocksdfgNo ratings yet

- Factors Determining Optimal Capital StructureDocument8 pagesFactors Determining Optimal Capital StructureArindam Mitra100% (8)

- Notes of Dividend PolicyDocument16 pagesNotes of Dividend PolicyVineet VermaNo ratings yet

- Dividend Assignment ReportDocument20 pagesDividend Assignment ReportSadia Afroz LeezaNo ratings yet

- Leverage Analysis ProjectDocument106 pagesLeverage Analysis Projectbalki123No ratings yet

- Christ FM Unit 1.4 NotesDocument3 pagesChrist FM Unit 1.4 NotesDrawing MasterNo ratings yet

- Dividend Policy AssignmentDocument8 pagesDividend Policy Assignmentgeetikag2018No ratings yet

- C-5 Dividend Policy 3rdDocument12 pagesC-5 Dividend Policy 3rdsamuel debebeNo ratings yet

- Angga Dwi PutraDocument13 pagesAngga Dwi PutraSuci IsmadyaNo ratings yet

- DEVIDEND DICISION... HDFC Bank-2015Document64 pagesDEVIDEND DICISION... HDFC Bank-2015Tanvir KhanNo ratings yet

- Dividend PolicyDocument10 pagesDividend PolicyShivam MalhotraNo ratings yet

- Financial ManagementDocument8 pagesFinancial ManagementAayush JainNo ratings yet

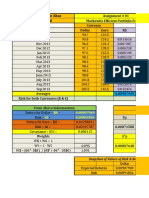

- Mushtaq Hussain Khan MM133038: Assignment # 01 Markowitz Efficient Portfolio Frontier Currency Months Dollar Euro R$Document6 pagesMushtaq Hussain Khan MM133038: Assignment # 01 Markowitz Efficient Portfolio Frontier Currency Months Dollar Euro R$Muneeb AmanNo ratings yet

- Venture Capital in PakistanDocument2 pagesVenture Capital in PakistanMuneeb AmanNo ratings yet

- Summary of Results and Their InterpretationDocument1 pageSummary of Results and Their InterpretationMuneeb AmanNo ratings yet

- Interest Rate Hedging-ExamplesDocument9 pagesInterest Rate Hedging-ExamplesMuneeb AmanNo ratings yet

- Interest Rate Hedging-ExamplesDocument9 pagesInterest Rate Hedging-ExamplesMuneeb AmanNo ratings yet

- Formula Sheet: C S N d Xe N d S X r+ σ τ σ τDocument2 pagesFormula Sheet: C S N d Xe N d S X r+ σ τ σ τMuneeb AmanNo ratings yet

- Investment Analysis-ButtDocument11 pagesInvestment Analysis-ButtMuneeb AmanNo ratings yet

- Greeks PutDocument27 pagesGreeks PutMuneeb AmanNo ratings yet

- University of Azad Jammu and Kashmir Muzaffarabad: Muneeb Aman Roll No: 02 Regd. No. 2015-GMDB (B) - 000573Document37 pagesUniversity of Azad Jammu and Kashmir Muzaffarabad: Muneeb Aman Roll No: 02 Regd. No. 2015-GMDB (B) - 000573Muneeb AmanNo ratings yet

- Internship Report On National Bank of Pakistan (Main Branch Palandri)Document52 pagesInternship Report On National Bank of Pakistan (Main Branch Palandri)Muneeb AmanNo ratings yet

- Chapter No 08 CAMEL Framework: Capital Adequacy-CDocument10 pagesChapter No 08 CAMEL Framework: Capital Adequacy-CMuneeb AmanNo ratings yet

- 2014 2015 2016 2017 2018 AssetsDocument6 pages2014 2015 2016 2017 2018 AssetsMuneeb AmanNo ratings yet

- Riphah International UniversityDocument2 pagesRiphah International UniversityMuneeb AmanNo ratings yet

- Week 6 and Week 7Document49 pagesWeek 6 and Week 7Muneeb AmanNo ratings yet

- Hira 2Document22 pagesHira 2Muneeb AmanNo ratings yet

- Chapter 7 - Stocks and Stock ValuationDocument5 pagesChapter 7 - Stocks and Stock ValuationYasmine AbdelbaryNo ratings yet

- Andritz Rapport-Annuel PDFDocument136 pagesAndritz Rapport-Annuel PDFIR MA Al AzharNo ratings yet

- Kling OriginManagingAgency 1966Document12 pagesKling OriginManagingAgency 1966Ankan Bairagya17No ratings yet

- FinalDocument30 pagesFinalhiraa_bhattiNo ratings yet

- Automobile Sector of PakistanDocument28 pagesAutomobile Sector of PakistanImama KhanNo ratings yet

- Instant Download Ebook PDF Fundamentals of Corporate Finance 7th Edition by Richard A Brealey 6 PDF ScribdDocument41 pagesInstant Download Ebook PDF Fundamentals of Corporate Finance 7th Edition by Richard A Brealey 6 PDF Scribdlauryn.corbett387100% (43)

- Internship Program.: ProposalDocument5 pagesInternship Program.: ProposalstrangerNo ratings yet

- Bangladesh University of Professionals Faculty of Business StudiesDocument9 pagesBangladesh University of Professionals Faculty of Business StudiesTashkin MahmudNo ratings yet

- Questionnaire Revised 2Document7 pagesQuestionnaire Revised 2Anish MarwahNo ratings yet

- MBA Derivatives ReportDocument93 pagesMBA Derivatives ReportcheemaNo ratings yet

- Reaction Paper (Chapter 13)Document5 pagesReaction Paper (Chapter 13)Arsenio RojoNo ratings yet

- Financial Management: Interest RatesDocument12 pagesFinancial Management: Interest RatesArif SharifNo ratings yet

- A Project Report ON Investment Options Offered by Icici Bank and HDFC BankDocument78 pagesA Project Report ON Investment Options Offered by Icici Bank and HDFC BanksimanttNo ratings yet

- Blessings InterviewDocument329 pagesBlessings Interviewsalihu_aliNo ratings yet

- MFM Project Guidelines From Christ University FFFFFDocument6 pagesMFM Project Guidelines From Christ University FFFFFakash08agarwal_18589No ratings yet

- Chapter 05 - AnswerDocument36 pagesChapter 05 - AnswerAgentSkySkyNo ratings yet

- SBI - Life - Smart - Wealth - Assure - V03 - Brochure - 20 - 1Document15 pagesSBI - Life - Smart - Wealth - Assure - V03 - Brochure - 20 - 1sunder vermaNo ratings yet

- Memorandum of Association OF Darcl Logistics LimitedDocument58 pagesMemorandum of Association OF Darcl Logistics LimitedPiyush Nikam MishraNo ratings yet

- Review of Literature WordDocument5 pagesReview of Literature WordLakshmiRengarajanNo ratings yet

- Accounting Research Journal: Article InformationDocument29 pagesAccounting Research Journal: Article InformationShelviDyanPrastiwiNo ratings yet

- Edwards Lifesciences Corp (EW) : Financial and Strategic SWOT Analysis ReviewDocument36 pagesEdwards Lifesciences Corp (EW) : Financial and Strategic SWOT Analysis ReviewHITESH MAKHIJANo ratings yet

- Evaluating A Company's Capital StructureDocument3 pagesEvaluating A Company's Capital StructureSteffanie228No ratings yet