You might also like

- Understand Banks & Financial Markets: An Introduction to the International World of Money & FinanceFrom EverandUnderstand Banks & Financial Markets: An Introduction to the International World of Money & FinanceRating: 4 out of 5 stars4/5 (9)

- Money Market of Bangladesh.: Characteristics: The Central Bank Controls The Entire Operation of The OrganizedDocument4 pagesMoney Market of Bangladesh.: Characteristics: The Central Bank Controls The Entire Operation of The OrganizedFaisal Hamid EmonNo ratings yet

- Bank Fundamentals: An Introduction to the World of Finance and BankingFrom EverandBank Fundamentals: An Introduction to the World of Finance and BankingRating: 4.5 out of 5 stars4.5/5 (4)

- BLACKBOOKDocument27 pagesBLACKBOOKKushNo ratings yet

- Financial Markets Fundamentals: Why, how and what Products are traded on Financial Markets. Understand the Emotions that drive TradingFrom EverandFinancial Markets Fundamentals: Why, how and what Products are traded on Financial Markets. Understand the Emotions that drive TradingNo ratings yet

- Following Are The Features of Money MarketDocument9 pagesFollowing Are The Features of Money MarketVaidehi MirajkarNo ratings yet

- Submitted To Submitted By: Course Name: Course Code: Name of AssignmentDocument9 pagesSubmitted To Submitted By: Course Name: Course Code: Name of AssignmentPigeons LoftNo ratings yet

- Characteristics of a well-developed Indian money marketDocument7 pagesCharacteristics of a well-developed Indian money marketamritranjan123_34249No ratings yet

- Financial MarketDocument26 pagesFinancial Marketmamta jainNo ratings yet

- Biitm by Dr. Sudeshna Dutta Asst. Professor FinanceDocument49 pagesBiitm by Dr. Sudeshna Dutta Asst. Professor FinancePrity AsopaNo ratings yet

- Money MarketDocument21 pagesMoney MarketanuradhaNo ratings yet

- Accounting and FinancialDocument31 pagesAccounting and FinancialAkash ArvikarNo ratings yet

- Money Market InstrumentsDocument15 pagesMoney Market InstrumentsDharmendra Singh100% (1)

- Money Market in India: Prof. Shailendra Singh BhadouriaDocument18 pagesMoney Market in India: Prof. Shailendra Singh Bhadouriaraveesh kumarNo ratings yet

- Indian Money MarketDocument11 pagesIndian Money MarketPradeepKumarNo ratings yet

- Background of Money Market in BangladeshDocument5 pagesBackground of Money Market in Bangladeshanamikabhoumik100% (1)

- FALLSEM2020-21 CCA2705 TH VL2020210101345 Reference Material III 14-Jul-2020 FINANCIAL MARKETS Module 2 5Document40 pagesFALLSEM2020-21 CCA2705 TH VL2020210101345 Reference Material III 14-Jul-2020 FINANCIAL MARKETS Module 2 5Jayagokul SaravananNo ratings yet

- Money Market FundamentalsDocument7 pagesMoney Market FundamentalsManohar SumathiNo ratings yet

- MONEY MARKET OVERVIEWDocument10 pagesMONEY MARKET OVERVIEWjhanvi tayalNo ratings yet

- Types and OF: Money Market and Capital MarketDocument39 pagesTypes and OF: Money Market and Capital MarketDikshita NavaniNo ratings yet

- Role of Money MarketsDocument3 pagesRole of Money Marketssiddharthjain_90No ratings yet

- Money MarketDocument44 pagesMoney MarketReshma MaliNo ratings yet

- Money MarketDocument7 pagesMoney MarketShaimon JosephNo ratings yet

- Definitions of Money MarketDocument7 pagesDefinitions of Money Marketsamaira7No ratings yet

- Money Market and Capital MarketDocument33 pagesMoney Market and Capital MarketMohammad Shaniaz IslamNo ratings yet

- Assignment: Inancial Nstituton MarketsDocument25 pagesAssignment: Inancial Nstituton MarketsImranNo ratings yet

- HS 2nd Year Finance Project 2023Document7 pagesHS 2nd Year Finance Project 2023jnsz7t5bpqNo ratings yet

- Money Markets in IndiaDocument56 pagesMoney Markets in IndiaAvanishNo ratings yet

- Indian Money Market Structure and ComponentsDocument9 pagesIndian Money Market Structure and ComponentsPrasun KumarNo ratings yet

- Money MarketDocument37 pagesMoney MarketPrajith KrishNo ratings yet

- Unit 3 FINANACIAL MARKETS 30 MarksDocument58 pagesUnit 3 FINANACIAL MARKETS 30 Marksaishwarya raikarNo ratings yet

- Indian Money Market Features & ReformsDocument3 pagesIndian Money Market Features & ReformssonaNo ratings yet

- Features / Characteristics of Indian Money MarketDocument5 pagesFeatures / Characteristics of Indian Money Marketnaved7No ratings yet

- Money MarketDocument20 pagesMoney MarketDev AshishNo ratings yet

- Indian Money Market OperationsDocument28 pagesIndian Money Market OperationsdeepeshmahajanNo ratings yet

- The Role of Financial Market and Institution in The Economic Development of BangladeshDocument11 pagesThe Role of Financial Market and Institution in The Economic Development of Bangladeshbleeding_heart120567% (12)

- Name of School: AMITY LAW SCHOOL, Gurgaon: Money MarketDocument16 pagesName of School: AMITY LAW SCHOOL, Gurgaon: Money Marketankita singhNo ratings yet

- Module 10 Financial MarketsDocument61 pagesModule 10 Financial Marketsg.prasanna saiNo ratings yet

- Presentation On Money Market: Manasi JinalDocument22 pagesPresentation On Money Market: Manasi JinalYashBhattNo ratings yet

- A PPT On Money MarketDocument25 pagesA PPT On Money MarketBasanta100% (27)

- Indian Money Market - FinDocument4 pagesIndian Money Market - Finphiliptijo88100% (1)

- Money MarketDocument12 pagesMoney MarketNeha RathoreNo ratings yet

- Factors Operating in the Money Market ExplainedDocument26 pagesFactors Operating in the Money Market Explaineddeepesh_sinhaNo ratings yet

- Money Market in BangladeshDocument34 pagesMoney Market in Bangladeshjubaida khanamNo ratings yet

- 08 - Chapter 3 PDFDocument39 pages08 - Chapter 3 PDFvidushi sahuNo ratings yet

- The Economic Markets SyllabusDocument30 pagesThe Economic Markets SyllabusDeepak R GoradNo ratings yet

- Arsh Advani - 1 Abhishek Dhariwal - 8 Pooja Jain - 17 Priyanka Majmundar - 32 Himanshu SanghviDocument14 pagesArsh Advani - 1 Abhishek Dhariwal - 8 Pooja Jain - 17 Priyanka Majmundar - 32 Himanshu SanghviArshAdvaniNo ratings yet

- PobDocument24 pagesPobgillyhicksNo ratings yet

- Financial Markets: Money MarketDocument11 pagesFinancial Markets: Money Marketramesh2490No ratings yet

- Final - SFM - Money Market PDFDocument37 pagesFinal - SFM - Money Market PDFMarikrishna Chandran CANo ratings yet

- Finnancial Enviroment of BusinessDocument22 pagesFinnancial Enviroment of Businesssuru2331No ratings yet

- 19353sm SFM Finalnew cp10 PDFDocument33 pages19353sm SFM Finalnew cp10 PDFTushar JoshiNo ratings yet

- 19353sm SFM Finalnew cp10 PDFDocument33 pages19353sm SFM Finalnew cp10 PDFRajat SahuNo ratings yet

- Indian Money MarketDocument2 pagesIndian Money MarketSandeep KulkarniNo ratings yet

- A Manual On Non Banking Financial Institutions: 9. Anti Money Laundering StandardsDocument143 pagesA Manual On Non Banking Financial Institutions: 9. Anti Money Laundering StandardsRahul JagwaniNo ratings yet

- Money MarketDocument10 pagesMoney Marketswe1234No ratings yet

- Money Market Reforms and InstrumentsDocument20 pagesMoney Market Reforms and InstrumentsAshish PatangeNo ratings yet

- Call Money Market: By, M.Tulasi PrasadDocument24 pagesCall Money Market: By, M.Tulasi Prasadprasadnaidu00No ratings yet

- MOney MarketDocument13 pagesMOney MarketNaveen KumarNo ratings yet

- Wwwruvj C×WZ Z 96Zg E V P WMCVNX (WRWW) C ' Cyiæl I GWNJV Cöv - ©X Fwz©I WeáwßDocument1 pageWwwruvj C×WZ Z 96Zg E V P WMCVNX (WRWW) C ' Cyiæl I GWNJV Cöv - ©X Fwz©I WeáwßKhanNo ratings yet

- Payment 1Document3 pagesPayment 1Faisal Hamid EmonNo ratings yet

- DocumentaryDocument1 pageDocumentaryFaisal Hamid EmonNo ratings yet

- Assignment On PMGTDocument2 pagesAssignment On PMGTFaisal Hamid EmonNo ratings yet

- JamilDocument30 pagesJamilFaisal Hamid EmonNo ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

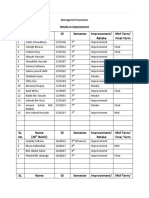

- Retake or Improvement DetailsDocument3 pagesRetake or Improvement DetailsFaisal Hamid EmonNo ratings yet

- ZOOM Link of ClassesDocument4 pagesZOOM Link of ClassesFaisal Hamid EmonNo ratings yet

- ZOOM Link of ClassesDocument4 pagesZOOM Link of ClassesFaisal Hamid EmonNo ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Retake or Improvement DetailsDocument3 pagesRetake or Improvement DetailsFaisal Hamid EmonNo ratings yet

- Wholesaler of Glow Sticks Offers Bulk DealsDocument3 pagesWholesaler of Glow Sticks Offers Bulk DealsfaryalNo ratings yet

- Walmart EssayDocument9 pagesWalmart EssayIrish TorresNo ratings yet

- Solved Is Overshooting in Theory and in Practice Consistent With PurchasingDocument1 pageSolved Is Overshooting in Theory and in Practice Consistent With PurchasingM Bilal SaleemNo ratings yet

- Stock Price Analysis and Valuations-: Figure 5 (A) 5 (B)Document7 pagesStock Price Analysis and Valuations-: Figure 5 (A) 5 (B)sanjNo ratings yet

- Marketing Strategy Text and Cases 6th Edition Ferrell Solutions Manual DownloadDocument9 pagesMarketing Strategy Text and Cases 6th Edition Ferrell Solutions Manual DownloadDinorah Strack100% (23)

- REBUTTALS FOR STOCK MARKET SKEPTICSDocument28 pagesREBUTTALS FOR STOCK MARKET SKEPTICSVictor100% (3)

- Keown Valuation and Charactheristic of StockDocument44 pagesKeown Valuation and Charactheristic of Stockmaya husniaNo ratings yet

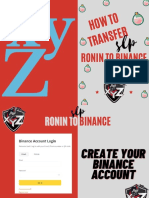

- How to transfer SLP token from Ronin to Binance and convert to PHPDocument11 pagesHow to transfer SLP token from Ronin to Binance and convert to PHPGeraldine VergaraNo ratings yet

- Strategic Decision-Making Final Exam Dec 22Document23 pagesStrategic Decision-Making Final Exam Dec 22Fungai MajuriraNo ratings yet

- Iapm 7 TutDocument4 pagesIapm 7 TutTshepang MatebesiNo ratings yet

- GSBA504Document6 pagesGSBA504Hunganistan JózsefNo ratings yet

- Introduction of Digital Media Chapter 1 - MyDocument2 pagesIntroduction of Digital Media Chapter 1 - MyTahseen Raza100% (1)

- Planning The New Venture: 2.1 What Is A Business Plan?Document26 pagesPlanning The New Venture: 2.1 What Is A Business Plan?Hasan AskaryNo ratings yet

- C1 - Overview of International MarketingDocument9 pagesC1 - Overview of International Marketinghương nguyễnNo ratings yet

- Petrobras Case StudyDocument13 pagesPetrobras Case Studykid.hahnNo ratings yet

- Financial Asset at Fair Value Problem 21-1 (IFRS) : Solution 21-1 Answer CDocument15 pagesFinancial Asset at Fair Value Problem 21-1 (IFRS) : Solution 21-1 Answer CLiana100% (2)

- Custom Jewelry Maker Marketing PlanDocument19 pagesCustom Jewelry Maker Marketing PlanPalo Alto Software100% (13)

- Swot On VodafoneDocument4 pagesSwot On VodafoneNagaraj GogiNo ratings yet

- KeywordsDocument3 pagesKeywordsNisco SysNo ratings yet

- Business Plan Format Guide: Written ProposalDocument6 pagesBusiness Plan Format Guide: Written ProposalR- Jay MontallanaNo ratings yet

- GMA Network Inc.: A Presentation of The FinancialsDocument14 pagesGMA Network Inc.: A Presentation of The FinancialsZed LadjaNo ratings yet

- JPM Weekly MKT Recap 9-10-12Document2 pagesJPM Weekly MKT Recap 9-10-12Flat Fee PortfoliosNo ratings yet

- Innovation in RetailingDocument11 pagesInnovation in Retailingliza shoorNo ratings yet

- Valuation Report: Property AddressDocument18 pagesValuation Report: Property AddressOteng ThembaNo ratings yet

- B2B SegmentationDocument81 pagesB2B SegmentationShivaen KatialNo ratings yet

- Marketing Plan TemplateDocument17 pagesMarketing Plan TemplateChrisNo ratings yet

- Chart Patterns: Base Counting NotesDocument19 pagesChart Patterns: Base Counting NotesAnonymous Mw6J6Sh50% (2)

- The Role of Government in Accelerating Industrial Development in Developing CountriesDocument12 pagesThe Role of Government in Accelerating Industrial Development in Developing CountriesTan Tien NguyenNo ratings yet

- Corporate Finance Ii2008 PDFDocument85 pagesCorporate Finance Ii2008 PDFTrymore KateeraNo ratings yet

- PM Q4 - Week 1Document14 pagesPM Q4 - Week 1xfq6tfqgtwNo ratings yet

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingFrom EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingRating: 4.5 out of 5 stars4.5/5 (97)

- IFRS 9 and CECL Credit Risk Modelling and Validation: A Practical Guide with Examples Worked in R and SASFrom EverandIFRS 9 and CECL Credit Risk Modelling and Validation: A Practical Guide with Examples Worked in R and SASRating: 3 out of 5 stars3/5 (5)

- The Business Legal Lifecycle US Edition: How To Successfully Navigate Your Way From Start Up To SuccessFrom EverandThe Business Legal Lifecycle US Edition: How To Successfully Navigate Your Way From Start Up To SuccessNo ratings yet

- AI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersFrom EverandAI For Lawyers: How Artificial Intelligence is Adding Value, Amplifying Expertise, and Transforming CareersNo ratings yet

- Introduction to Negotiable Instruments: As per Indian LawsFrom EverandIntroduction to Negotiable Instruments: As per Indian LawsRating: 5 out of 5 stars5/5 (1)

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorFrom EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorRating: 4.5 out of 5 stars4.5/5 (132)

- Getting Through: Cold Calling Techniques To Get Your Foot In The DoorFrom EverandGetting Through: Cold Calling Techniques To Get Your Foot In The DoorRating: 4.5 out of 5 stars4.5/5 (63)

- Wall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementFrom EverandWall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementRating: 4.5 out of 5 stars4.5/5 (20)

- Learn the Essentials of Business Law in 15 DaysFrom EverandLearn the Essentials of Business Law in 15 DaysRating: 4 out of 5 stars4/5 (13)

- Disloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpFrom EverandDisloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpRating: 4 out of 5 stars4/5 (214)

- The Complete Book of Wills, Estates & Trusts (4th Edition): Advice That Can Save You Thousands of Dollars in Legal Fees and TaxesFrom EverandThe Complete Book of Wills, Estates & Trusts (4th Edition): Advice That Can Save You Thousands of Dollars in Legal Fees and TaxesRating: 4 out of 5 stars4/5 (1)

- The Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesWhite Collar CriminalsFrom EverandThe Chickenshit Club: Why the Justice Department Fails to Prosecute ExecutivesWhite Collar CriminalsRating: 5 out of 5 stars5/5 (24)

- How to Win a Merchant Dispute or Fraudulent Chargeback CaseFrom EverandHow to Win a Merchant Dispute or Fraudulent Chargeback CaseNo ratings yet

- How to Structure Your Business for Success: Choosing the Correct Legal Structure for Your BusinessFrom EverandHow to Structure Your Business for Success: Choosing the Correct Legal Structure for Your BusinessNo ratings yet

- Competition and Antitrust Law: A Very Short IntroductionFrom EverandCompetition and Antitrust Law: A Very Short IntroductionRating: 5 out of 5 stars5/5 (3)

- LLC: LLC Quick start guide - A beginner's guide to Limited liability companies, and starting a businessFrom EverandLLC: LLC Quick start guide - A beginner's guide to Limited liability companies, and starting a businessRating: 5 out of 5 stars5/5 (1)

- The Shareholder Value Myth: How Putting Shareholders First Harms Investors, Corporations, and the PublicFrom EverandThe Shareholder Value Myth: How Putting Shareholders First Harms Investors, Corporations, and the PublicRating: 5 out of 5 stars5/5 (1)

- Building Your Empire: Achieve Financial Freedom with Passive IncomeFrom EverandBuilding Your Empire: Achieve Financial Freedom with Passive IncomeNo ratings yet

- Legal Guide for Starting & Running a Small BusinessFrom EverandLegal Guide for Starting & Running a Small BusinessRating: 4.5 out of 5 stars4.5/5 (9)