You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- SHL-AFP Insulated Flexible Air DuctDocument2 pagesSHL-AFP Insulated Flexible Air DuctWH TNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- TOZEN Spring Isolator PTH-S-SG (A) V1214Document1 pageTOZEN Spring Isolator PTH-S-SG (A) V1214WH TNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- BELITE STP 1x2x18AWG UL2092 - UD1310Document3 pagesBELITE STP 1x2x18AWG UL2092 - UD1310WH TNo ratings yet

- CSD Lea014.e5 PDFDocument4 pagesCSD Lea014.e5 PDFWH TNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Kossan AR 2019 PDFDocument163 pagesKossan AR 2019 PDFWH TNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Ashrae Malaysia ChapterDocument1 pageAshrae Malaysia ChapterWH TNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- SOP For Construction Industry To Operate During MCODocument7 pagesSOP For Construction Industry To Operate During MCOWH TNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- GB Health Care Presentation Rev1Document42 pagesGB Health Care Presentation Rev1WH TNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- JAKS TheEdgeDaily 27112019Document1 pageJAKS TheEdgeDaily 27112019WH TNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Genius GPT CatalogueDocument8 pagesGenius GPT CatalogueWH TNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- SOP For Construction Industry To Operate During MCODocument7 pagesSOP For Construction Industry To Operate During MCOWH TNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

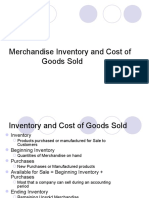

- Acoounting For Inventory and Cost of Goods SoldDocument39 pagesAcoounting For Inventory and Cost of Goods Soldsaba gul rehmatNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Problem 1Document13 pagesProblem 1Ghaill CruzNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Vee Jay AccountingDocument221 pagesVee Jay AccountingWesley KisiNo ratings yet

- Foundations in Accountancy FFA/ACCA FDocument112 pagesFoundations in Accountancy FFA/ACCA FK60 Triệu Thùy LinhNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Key Chapter 11Document3 pagesKey Chapter 11JinAe NaNo ratings yet

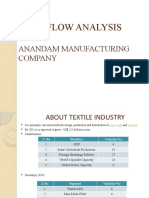

- Cash Flow Analysis: Anandam Manufacturing CompanyDocument13 pagesCash Flow Analysis: Anandam Manufacturing CompanyANANTHA BHAIRAVI MNo ratings yet

- Sevice Entity Module - 695420894Document95 pagesSevice Entity Module - 695420894Kent Justine AbegoniaNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Chapter 2 Problems - IADocument8 pagesChapter 2 Problems - IAKimochi SenpaiiNo ratings yet

- Pembahasan Contoh Soal Matrikulasi Day 2Document5 pagesPembahasan Contoh Soal Matrikulasi Day 2valdaNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Quiz No. 2Document2 pagesQuiz No. 2Nayra DizonNo ratings yet

- FABM2 Module 1Document14 pagesFABM2 Module 1Rea Mariz Jordan100% (1)

- bài tập errorDocument4 pagesbài tập errorHoàng Bảo TrâmNo ratings yet

- Basic Accounting Terms ListDocument3 pagesBasic Accounting Terms ListBogdan MirceaNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Case: Ii: Lecturer: Mr. Shakeel BaigDocument2 pagesCase: Ii: Lecturer: Mr. Shakeel BaigKathleen De JesusNo ratings yet

- Accounting Cycle of A Merchandising BusinessDocument34 pagesAccounting Cycle of A Merchandising BusinessTariga, Dharen Joy J.No ratings yet

- Assignment POSTING TO THE LEDGERDocument7 pagesAssignment POSTING TO THE LEDGERJie SapornaNo ratings yet

- ICI Pakistan Limited: Balance SheetDocument28 pagesICI Pakistan Limited: Balance SheetArsalan KhanNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Practical Accounting TwoDocument25 pagesPractical Accounting TwoJoseph SalidoNo ratings yet

- QuizDocument5 pagesQuizmiss independent100% (1)

- 2 Topsim WS2012 13 InitialsituationDocument8 pages2 Topsim WS2012 13 InitialsituationMaliha KhanNo ratings yet

- Example Income Statement:: Gross SalesDocument2 pagesExample Income Statement:: Gross Salesabdirahman YonisNo ratings yet

- Wright Investors Service Comprehensive Report For MGC Pharmaceuticals LTDDocument67 pagesWright Investors Service Comprehensive Report For MGC Pharmaceuticals LTDAnonymous mg0c9hqXCNo ratings yet

- Edgar Detoya-Answer KeyDocument14 pagesEdgar Detoya-Answer KeyAMBER GAMERNo ratings yet

- Financial Statement AnalysisDocument5 pagesFinancial Statement AnalysisPines MacapagalNo ratings yet

- Moffett Nathanson SnapDocument20 pagesMoffett Nathanson SnapSamson AmoreNo ratings yet

- Textile Mills LimitedDocument33 pagesTextile Mills LimitedSRKNo ratings yet

- Fsa Lectures (Notes) : Introduction To Financial Statement AnalysisDocument13 pagesFsa Lectures (Notes) : Introduction To Financial Statement AnalysisDaniyal ZafarNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Tutorial 2 Q Part 1 - Accounting Cycle For Trade and ServicesDocument8 pagesTutorial 2 Q Part 1 - Accounting Cycle For Trade and ServicesNezelle WongNo ratings yet

- Case Study - ACI and Marico BDDocument9 pagesCase Study - ACI and Marico BDsadekjakeNo ratings yet

- Cbactg01 Complete ModuleDocument170 pagesCbactg01 Complete ModuleJ LagardeNo ratings yet