You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Coffee KingdomDocument13 pagesCoffee Kingdomlumonyet hohoNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Process Safety - Recommended Practice On KPIsDocument90 pagesProcess Safety - Recommended Practice On KPIsfrancis100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Balance Sheet Detective Additional AnalysisDocument2 pagesBalance Sheet Detective Additional AnalysisAlina ZubairNo ratings yet

- Check List For Revenue Audit of A BankDocument4 pagesCheck List For Revenue Audit of A Bankjibujinson50% (2)

- BS en 12075-1997 - (2018-06-28 - 03-58-44 Am)Document14 pagesBS en 12075-1997 - (2018-06-28 - 03-58-44 Am)Rankie ChoiNo ratings yet

- PDF 20230219 143109 0000Document1 pagePDF 20230219 143109 0000Sam SamNo ratings yet

- Altascio Technologies India Private Limited: D&B Business DirectoryDocument4 pagesAltascio Technologies India Private Limited: D&B Business DirectoryHaritha HaribabuNo ratings yet

- F5 - Mock A - AnswersDocument13 pagesF5 - Mock A - AnswersmasangaaxNo ratings yet

- Kalyan Jewellers India LimitedDocument3 pagesKalyan Jewellers India LimitedJijo JosephNo ratings yet

- Technology - Entrepreneurship - Bringing - Innovation - To... - (PG - 264 - 302) - Chapter 8Document39 pagesTechnology - Entrepreneurship - Bringing - Innovation - To... - (PG - 264 - 302) - Chapter 8Uzma NaumanNo ratings yet

- Managerial Economics Applications Strategies and Tactics 13th Edition James R Mcguigan R Charles Moyer Frederick H Deb HarrisDocument33 pagesManagerial Economics Applications Strategies and Tactics 13th Edition James R Mcguigan R Charles Moyer Frederick H Deb Harriskatieterryrlrb100% (11)

- Electrical Enclosure Catalog Ca304001en PDFDocument524 pagesElectrical Enclosure Catalog Ca304001en PDFNathanNo ratings yet

- FABM2 LAS 10 Income and Business TaxationDocument13 pagesFABM2 LAS 10 Income and Business TaxationXander AlcantaraNo ratings yet

- Irrm Revision NotesDocument19 pagesIrrm Revision Notesteam aspirantsNo ratings yet

- Agence France-PresseDocument2 pagesAgence France-PresseZainab Ali KhanNo ratings yet

- Myeg InvoiceDocument1 pageMyeg InvoiceRiaz KhanNo ratings yet

- Lessons From The Titans: What Companies in The New Economy Can Learn From The Great Industrial Giants To Drive Sustainable Success Scott DavisDocument52 pagesLessons From The Titans: What Companies in The New Economy Can Learn From The Great Industrial Giants To Drive Sustainable Success Scott Davisjason.hollendonner905100% (19)

- Character Formation Chapter 5.docx Version 1Document8 pagesCharacter Formation Chapter 5.docx Version 1Criminegrology TvNo ratings yet

- Union vs. VivarDocument2 pagesUnion vs. VivarKê MilanNo ratings yet

- Summary On "Uber: The New Face of E-Commerce"Document2 pagesSummary On "Uber: The New Face of E-Commerce"Sonu Tandukar100% (1)

- Burgelman 1983Document20 pagesBurgelman 1983Hoàng BảoNo ratings yet

- Q1 Module 7Document40 pagesQ1 Module 7Guada Guan FabioNo ratings yet

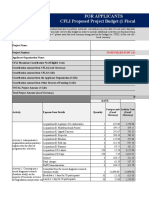

- Modus RP Cfli Proposed Project Budget For Project Spanning 1 Fy - enDocument17 pagesModus RP Cfli Proposed Project Budget For Project Spanning 1 Fy - enHélio MutombeneNo ratings yet

- Portfolio Revision: Raj Kumar Faculty, PUDocument24 pagesPortfolio Revision: Raj Kumar Faculty, PUrajunsc100% (4)

- Inspection Checklist: A. Tools and Equipment YES NODocument1 pageInspection Checklist: A. Tools and Equipment YES NOHENJEL PERALESNo ratings yet

- FINAL REPORT (Edited) 161-009-45 PDFDocument87 pagesFINAL REPORT (Edited) 161-009-45 PDFpabel ahmedNo ratings yet

- Kim2005 PDFDocument12 pagesKim2005 PDFHassan TariqNo ratings yet

- Entrepreneurship Budget of WorkDocument3 pagesEntrepreneurship Budget of WorkRachel BandiolaNo ratings yet

- 32-95 Rev 4 - Environmental Occupational Health and Safety Incident ManagementDocument69 pages32-95 Rev 4 - Environmental Occupational Health and Safety Incident ManagementZinhle DlaminiNo ratings yet

- 123Document3 pages123Dilan WarnakulasooriyaNo ratings yet