You might also like

- Cathay v. Vasquez 399 SCRA 207Document2 pagesCathay v. Vasquez 399 SCRA 207FSCBNo ratings yet

- CIR v. PrietoDocument2 pagesCIR v. PrietoFSCBNo ratings yet

- Espidol v. COMELECDocument3 pagesEspidol v. COMELECFSCB0% (1)

- Abad v. COMELECDocument2 pagesAbad v. COMELECFSCBNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- 2019rev MS493Document2 pages2019rev MS493deepak777No ratings yet

- Public International Law - Dean Sedfrey M. CandelariaDocument16 pagesPublic International Law - Dean Sedfrey M. CandelariaAndrei Da JoseNo ratings yet

- 12 Cases For OmbudsmanDocument13 pages12 Cases For OmbudsmanElixirLanganlanganNo ratings yet

- 2012 Contracts Slides CH 7Document42 pages2012 Contracts Slides CH 7lindajkangNo ratings yet

- Jurnal Hukum - 2020 - 623-2244-2-pbDocument8 pagesJurnal Hukum - 2020 - 623-2244-2-pbKarimullah SaingNo ratings yet

- BCPC PresentationDocument40 pagesBCPC PresentationJoy Navaja Dominguez88% (41)

- Aguinaldo DoctrineDocument7 pagesAguinaldo Doctrineapril75No ratings yet

- Private Firearm SaleDocument2 pagesPrivate Firearm SalepreppeddudeNo ratings yet

- Dela Cruz - SPL Case DigestDocument4 pagesDela Cruz - SPL Case DigestJefferson A. dela CruzNo ratings yet

- Fifteen Reasons You Should Own A GunDocument2 pagesFifteen Reasons You Should Own A GunAmmoLand Shooting Sports NewsNo ratings yet

- Tan Vs Crisologo 2017Document2 pagesTan Vs Crisologo 2017Clyde TanNo ratings yet

- 2017 DOJ Free Bar Notes in Remedial LawDocument9 pages2017 DOJ Free Bar Notes in Remedial LawRoland ApareceNo ratings yet

- How Create A Calendar by Your Photos Using GimpDocument27 pagesHow Create A Calendar by Your Photos Using GimpEmiliano ProgrammiNo ratings yet

- Vice President Real Estate in Dallas FT Worth TX Resume Kevin BennettDocument2 pagesVice President Real Estate in Dallas FT Worth TX Resume Kevin BennettKevinBennett1No ratings yet

- #12-Digest-Matuguina Wood Vs CADocument2 pages#12-Digest-Matuguina Wood Vs CAJared RiveraNo ratings yet

- Notice: Privacy Act Systems of RecordsDocument34 pagesNotice: Privacy Act Systems of RecordsJustia.comNo ratings yet

- Civil Procedure Notes Compiled University of San Carlos College of Law 23Document5 pagesCivil Procedure Notes Compiled University of San Carlos College of Law 23Jan NiñoNo ratings yet

- Benedict Atkinson, Brian Fitzgerald (Auth.) - A Short History of Copyright - The Genie of Information-Springer International Publishing (2014)Document145 pagesBenedict Atkinson, Brian Fitzgerald (Auth.) - A Short History of Copyright - The Genie of Information-Springer International Publishing (2014)kovacmilovanovicNo ratings yet

- Save Our Springs TCEQ LawsuitDocument24 pagesSave Our Springs TCEQ LawsuitAnonymous Pb39klJNo ratings yet

- Las - LC4 Filipino Sa Piling Larang Akad Week 4Document9 pagesLas - LC4 Filipino Sa Piling Larang Akad Week 4FORBETA, KIANNE GELL C.No ratings yet

- Creation of LGU-Municipality of JimenezDocument5 pagesCreation of LGU-Municipality of JimenezJamiah HulipasNo ratings yet

- CDR SC JaidwalDocument68 pagesCDR SC JaidwalbabbuNo ratings yet

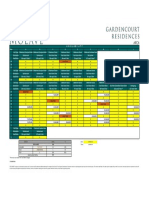

- Gardencourt Residences Molave Availability (July 19, 2022)Document1 pageGardencourt Residences Molave Availability (July 19, 2022)Nicolo MendozaNo ratings yet

- Affidavit Right To Travel and Declaration of StatusDocument15 pagesAffidavit Right To Travel and Declaration of StatusCharles Fowler100% (4)

- People Vs JanjalaniDocument3 pagesPeople Vs JanjalaniLee MatiasNo ratings yet

- Epc SchedulesDocument321 pagesEpc SchedulesAli Asghar ShahNo ratings yet

- Form-LRA-12 Affidavit of Lost TitleDocument2 pagesForm-LRA-12 Affidavit of Lost TitleEmpress DagiNo ratings yet

- Intranslaw - Zbornik 2017.Document593 pagesIntranslaw - Zbornik 2017.Emir DžambegovićNo ratings yet

- RamesDocument1 pageRamesAngelito RegulacionNo ratings yet

- Thomas Skinner GenealogyDocument11 pagesThomas Skinner Genealogybskinner5812No ratings yet