You might also like

- Introduction To Cookery Ncii: Cooking-The Act of Using Heat To Prepare Food For ConsumptionDocument5 pagesIntroduction To Cookery Ncii: Cooking-The Act of Using Heat To Prepare Food For Consumptionfranco jocsonNo ratings yet

- Module 7 Elements of PlatingDocument2 pagesModule 7 Elements of Platingfranco jocsonNo ratings yet

- Module 3. Basic CutsDocument6 pagesModule 3. Basic Cutsfranco jocson100% (3)

- Module 6. Prepare SandwichDocument6 pagesModule 6. Prepare Sandwichfranco jocson100% (2)

- 2.1 Economics As Applied Science - QuizDocument1 page2.1 Economics As Applied Science - Quizfranco jocsonNo ratings yet

- Module 4. Prepare AppetizersDocument4 pagesModule 4. Prepare Appetizersfranco jocson100% (4)

- 1.1 Intro To Applied Economics - QuizDocument3 pages1.1 Intro To Applied Economics - Quizfranco jocsonNo ratings yet

- Module 2. Methods of CookingDocument3 pagesModule 2. Methods of Cookingfranco jocsonNo ratings yet

- Module 5. Prepare Salad and DressingDocument5 pagesModule 5. Prepare Salad and Dressingfranco jocson87% (15)

- Compensation and WagesDocument12 pagesCompensation and Wagesfranco jocsonNo ratings yet

- Forms of Organization and PlanningDocument18 pagesForms of Organization and Planningfranco jocsonNo ratings yet

- Chapter 5: Staffing: RecruitmentDocument15 pagesChapter 5: Staffing: Recruitmentfranco jocsonNo ratings yet

- Compensation and WagesDocument12 pagesCompensation and Wagesfranco jocson100% (3)

- Cblm-Uc1 CMKPDocument102 pagesCblm-Uc1 CMKPfranco jocsonNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Starbucks Supply ChainDocument22 pagesStarbucks Supply Chainxozab90% (20)

- Project Work On Banking LawDocument19 pagesProject Work On Banking LawGaurav GehlotNo ratings yet

- Scheme of Work: Cambridge IGCSE / Cambridge IGCSE (9 1) Business Studies 0450 / 0986Document45 pagesScheme of Work: Cambridge IGCSE / Cambridge IGCSE (9 1) Business Studies 0450 / 0986Rico C. FranszNo ratings yet

- 2018 Bar Question Item No. VIIDocument3 pages2018 Bar Question Item No. VIIElsie Cayetano100% (1)

- Accountancy Review Center (ARC) of The Philippines Inc.: First Pre-Board ExaminationDocument26 pagesAccountancy Review Center (ARC) of The Philippines Inc.: First Pre-Board ExaminationCarlo AgravanteNo ratings yet

- FM6 Final ExamsDocument6 pagesFM6 Final Examsmartinelli ladoresNo ratings yet

- Sales JournalDocument3 pagesSales JournalViviNo ratings yet

- Precast Construction SeminarDocument30 pagesPrecast Construction SeminarNzar HamaNo ratings yet

- E BayDocument97 pagesE BayAhmet EminNo ratings yet

- Chapter 19 Testbank Solution Manual Management AccountingDocument66 pagesChapter 19 Testbank Solution Manual Management AccountingTrinh LêNo ratings yet

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument7 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit Balancelalit JainNo ratings yet

- SFC Presentation 1: 1. Professionals 2. Sharers 3. Creators 4. BondersDocument4 pagesSFC Presentation 1: 1. Professionals 2. Sharers 3. Creators 4. BondersSamuel Muabia PlānetNo ratings yet

- CBLM (Complete)Document53 pagesCBLM (Complete)DorgieFelicianoVirayNo ratings yet

- Revenue Cycle in Accounting Information Systems PDFDocument5 pagesRevenue Cycle in Accounting Information Systems PDFPrecious Ivy Fernandez100% (1)

- Law of Demand Slides PDFDocument20 pagesLaw of Demand Slides PDFAkankshya MishraNo ratings yet

- IRIS Credixo API v1.4 09thjan2018Document36 pagesIRIS Credixo API v1.4 09thjan2018Rupesh ParabNo ratings yet

- Nintex Workflow 2007 SDK 1.2Document235 pagesNintex Workflow 2007 SDK 1.2wregweNo ratings yet

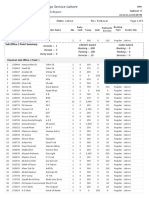

- The Asia Cargo Service Lahore: Invoices Dispatch ReportDocument6 pagesThe Asia Cargo Service Lahore: Invoices Dispatch ReportAsia CargoNo ratings yet

- Commerce McqsDocument10 pagesCommerce McqsAb GondalNo ratings yet

- NIK - 20pip EbookDocument12 pagesNIK - 20pip EbookSandro Pinna100% (1)

- F5 - 14financial Performance MeasurementDocument7 pagesF5 - 14financial Performance Measurementsajid newaz khanNo ratings yet

- BSBPMG540 Task 2 Knowledge Questions V1.1121-SV049116-MarianaVargasGarciaDocument5 pagesBSBPMG540 Task 2 Knowledge Questions V1.1121-SV049116-MarianaVargasGarciaRahmi Can ÖzmenNo ratings yet

- 1.1 MC - Exercises On Estate Tax (PRTC)Document8 pages1.1 MC - Exercises On Estate Tax (PRTC)marco poloNo ratings yet

- Dhiman S The Routledge Companion To Leadership and Change 2023Document484 pagesDhiman S The Routledge Companion To Leadership and Change 2023maxxion.hrNo ratings yet

- Material Self: Consumer Culture and ConsumerismDocument2 pagesMaterial Self: Consumer Culture and ConsumerismAngelo Chan100% (1)

- Curriculum Vitae Soedjatmiko: KontakDocument4 pagesCurriculum Vitae Soedjatmiko: KontakKang AdingNo ratings yet

- Cash Analytics: How To Make Your Working Capital Metrics WorkDocument5 pagesCash Analytics: How To Make Your Working Capital Metrics WorkMuhammadKashifNo ratings yet

- 2023 BW 320 Vantage Owners ManualDocument202 pages2023 BW 320 Vantage Owners ManualVolker DietrichNo ratings yet

- 10 Chapter 4Document49 pages10 Chapter 4AliNo ratings yet

- World Atlas of Illicit Flows-1Document152 pagesWorld Atlas of Illicit Flows-1Clinton Antonius100% (1)