You might also like

- Introduction to Negotiable Instruments: As per Indian LawsFrom EverandIntroduction to Negotiable Instruments: As per Indian LawsRating: 5 out of 5 stars5/5 (1)

- Contracts Project 3rd TremDocument17 pagesContracts Project 3rd TremYashwant ManothiyaNo ratings yet

- Goods under the Sale of Goods ActDocument20 pagesGoods under the Sale of Goods ActsiddharthNo ratings yet

- The Sale of Goods ActDocument49 pagesThe Sale of Goods ActPathway LawNo ratings yet

- Soga PDFDocument50 pagesSoga PDFPooja MeenaNo ratings yet

- Contract of Sale of GoodsDocument5 pagesContract of Sale of GoodsRonan FerrerNo ratings yet

- Laws Related To Contract, Property, TenancyDocument12 pagesLaws Related To Contract, Property, Tenancykrishan PatidarNo ratings yet

- Contract of sale guideDocument13 pagesContract of sale guidehina ranaNo ratings yet

- Transfer of Property Act ExplainedDocument15 pagesTransfer of Property Act ExplainedrubabshaikhNo ratings yet

- BailmentDocument7 pagesBailmentNavisha VermaNo ratings yet

- SECTION 1: Short Title, Extent and CommencementDocument27 pagesSECTION 1: Short Title, Extent and Commencementshivangi paliwalNo ratings yet

- Anuj Rathee Tpa 1142-1Document11 pagesAnuj Rathee Tpa 1142-1Ridhika SinghNo ratings yet

- Soga DefinitionDocument6 pagesSoga Definitionkushank.mittalNo ratings yet

- Saurabh Chopra's Property Law Exam NotesDocument30 pagesSaurabh Chopra's Property Law Exam NotesdukaantestNo ratings yet

- Transfer of Property Roll No 4 Pratiksha BhagatDocument17 pagesTransfer of Property Roll No 4 Pratiksha Bhagatpratiksha lakdeNo ratings yet

- Electricity AsDocument2 pagesElectricity AshbldjshfleNo ratings yet

- The Sale of Goods Act 1930 JNCWDocument39 pagesThe Sale of Goods Act 1930 JNCWselvam sNo ratings yet

- Contract - 2nd Sem - Navrose-2Document8 pagesContract - 2nd Sem - Navrose-2navrose1996No ratings yet

- Transfer of Property AssignmentDocument20 pagesTransfer of Property Assignmenturvesh bhardwajNo ratings yet

- Imovable and Movable Property PDFDocument13 pagesImovable and Movable Property PDFLively RoamerNo ratings yet

- Tpa NotesDocument14 pagesTpa NotesAdv Deepak Garg100% (1)

- The Sale of Goods Act, 1930: Chapter OutlineDocument41 pagesThe Sale of Goods Act, 1930: Chapter OutlineDasvinderSinghNo ratings yet

- Sales and Goods ActDocument9 pagesSales and Goods ActAksh AggarwalNo ratings yet

- Defining Sale of Goods ContractDocument12 pagesDefining Sale of Goods ContractAksh AggarwalNo ratings yet

- Pollock and Mulla The Sale of Goods ActDocument368 pagesPollock and Mulla The Sale of Goods ActAdira Chaturvedi100% (1)

- Sales of GoodsDocument41 pagesSales of GoodsFathimaHynulMNo ratings yet

- Sale of Goods Act overviewDocument6 pagesSale of Goods Act overviewShalini Nisha100% (1)

- TPA Bullet NotesDocument166 pagesTPA Bullet NotesvarshiniNo ratings yet

- Soga - 1Document17 pagesSoga - 1Ritvikh RajputNo ratings yet

- Tybba - Sem - 5: Content of ChapterDocument21 pagesTybba - Sem - 5: Content of ChapterRahul Rahul AhirNo ratings yet

- CONtractsDocument8 pagesCONtractsmanjeet kumarNo ratings yet

- Notes On The Different Types of Properties As Governed by Indian LawDocument2 pagesNotes On The Different Types of Properties As Governed by Indian LawChaitu ChaituNo ratings yet

- 3 SogaDocument94 pages3 SogaBARSHANo ratings yet

- CK 114Document21 pagesCK 114varun v sNo ratings yet

- Property Law Exam NotesDocument30 pagesProperty Law Exam NotesRitesh AroraNo ratings yet

- Sale of Goods Act - Class 1Document3 pagesSale of Goods Act - Class 1AbhirokxNo ratings yet

- LOC IIDocument12 pagesLOC IIbhumikabisht3175No ratings yet

- Business Law - 3Document25 pagesBusiness Law - 3saketNo ratings yet

- Transfer of Property in IndiaDocument76 pagesTransfer of Property in IndiaProf. Amit kashyap50% (2)

- An Introduction to the Sale of Goods ActDocument20 pagesAn Introduction to the Sale of Goods ActRakesh PruthiNo ratings yet

- Sale of Goods Act, 1930Document4 pagesSale of Goods Act, 1930somnath mahapatraNo ratings yet

- TpaDocument40 pagesTpadeepankarkatNo ratings yet

- TP Act Final DraftDocument16 pagesTP Act Final Draftvivek thakurNo ratings yet

- Property Law Exam Notes: Thelegal - Co.InDocument30 pagesProperty Law Exam Notes: Thelegal - Co.InnimishaNo ratings yet

- Contract of Sale EssentialsDocument8 pagesContract of Sale EssentialsHamna SikanderNo ratings yet

- Property Law IDocument10 pagesProperty Law IDhruv Thakur0% (1)

- Property Law Including Transfer of Property ActDocument30 pagesProperty Law Including Transfer of Property ActAbhishek PandeyNo ratings yet

- Section 3 and 5 of The Transfer of Property Act 1882Document18 pagesSection 3 and 5 of The Transfer of Property Act 1882vivek thakurNo ratings yet

- Damodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaDocument6 pagesDamodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaDileep ChowdaryNo ratings yet

- Levi Ability of Sales Tax To Actionable ClaimDocument3 pagesLevi Ability of Sales Tax To Actionable ClaimJuhi BansalNo ratings yet

- Dr. Ram Manohar Lohiya National Law University, Lucknow: Property Law-I: FINAL DRAFTDocument16 pagesDr. Ram Manohar Lohiya National Law University, Lucknow: Property Law-I: FINAL DRAFTtarun kulharNo ratings yet

- Transfer of Property Act - UditanshuDocument25 pagesTransfer of Property Act - UditanshuKrishna Ahuja100% (1)

- TopaDocument83 pagesTopaShivani Vasudeva VermaNo ratings yet

- An Introduction To The Sale of Goods ActDocument20 pagesAn Introduction To The Sale of Goods Actakkig1No ratings yet

- Legal Aspects ProjectDocument18 pagesLegal Aspects ProjectakshayNo ratings yet

- ML Unit-2Document34 pagesML Unit-2AkshayNo ratings yet

- Section 3 and 5 of The Transfer of Property Act.1882Document18 pagesSection 3 and 5 of The Transfer of Property Act.1882Anonymous H1TW3YY51K100% (1)

- Commercial Law Notes (Sale of Goods) Summary Commercial Law Notes (Sale of Goods) SummaryDocument37 pagesCommercial Law Notes (Sale of Goods) Summary Commercial Law Notes (Sale of Goods) SummaryDiana MintoNo ratings yet

- 6 The Sale of Goods Act Scanner Nikita BachawatDocument40 pages6 The Sale of Goods Act Scanner Nikita BachawatHimanshu RayNo ratings yet

- SOGA IntroDocument15 pagesSOGA IntrodNo ratings yet

- Goods Perishing and Property Passing Contract RulesDocument19 pagesGoods Perishing and Property Passing Contract RulesdNo ratings yet

- Sale of Goods Act essentialsDocument29 pagesSale of Goods Act essentialsKrithikaVenkat100% (2)

- Conditions and WarrantiesDocument11 pagesConditions and WarrantiesdNo ratings yet

- Law-of-contracts-II - LLB NotesDocument60 pagesLaw-of-contracts-II - LLB Notesd100% (1)

- Nationalism Research PaperDocument28 pagesNationalism Research PaperCamille CatorNo ratings yet

- Carlos v. Abelardo, GR 146504Document17 pagesCarlos v. Abelardo, GR 146504Anna NicerioNo ratings yet

- Fikir Eske Mekabir Amharic PDFDocument5 pagesFikir Eske Mekabir Amharic PDFFikr Yashenifal25% (4)

- Request For Proposal FOR: Tasiast Mauritanie Limited S.ADocument16 pagesRequest For Proposal FOR: Tasiast Mauritanie Limited S.AFunda HandasNo ratings yet

- 0051 001Document4 pages0051 001Raheem KassamNo ratings yet

- Hindi - WikipediaDocument21 pagesHindi - WikipediaArjunNo ratings yet

- A Written Report On Self Governance, Independent Nursing Practice, Evidence Based PracticeDocument16 pagesA Written Report On Self Governance, Independent Nursing Practice, Evidence Based PracticeCarlo Emmanuel Santos100% (2)

- Advanced Industrial and Labour Relations - Assignment 2Document4 pagesAdvanced Industrial and Labour Relations - Assignment 2Matthew MhlongoNo ratings yet

- Dead Man AlarmDocument5 pagesDead Man AlarmK S RaoNo ratings yet

- Anju Sharma U1 283 Grange Road, Ormond VIC 3204Document1 pageAnju Sharma U1 283 Grange Road, Ormond VIC 3204Aksh GillNo ratings yet

- CA FINAL IDT QUESTION BANK FOR MAYNOV 2021 Atul AgarwalDocument463 pagesCA FINAL IDT QUESTION BANK FOR MAYNOV 2021 Atul AgarwalRonita DuttaNo ratings yet

- Course Manual-Legal PsychologyDocument12 pagesCourse Manual-Legal PsychologyAnanya PillarisettyNo ratings yet

- Organized Crime: Gangs, Mules, Street-Level DealersDocument4 pagesOrganized Crime: Gangs, Mules, Street-Level DealersAudi KawiraNo ratings yet

- Republic of The Philippines Office of The City Prosecutor Puerto Princesa CityDocument4 pagesRepublic of The Philippines Office of The City Prosecutor Puerto Princesa CityHezro Inciso CaandoyNo ratings yet

- College Assurance v. BelfranltDocument16 pagesCollege Assurance v. BelfranltAgent BlueNo ratings yet

- Commercialization of Space Activities - The Laws and ImplicationsDocument25 pagesCommercialization of Space Activities - The Laws and ImplicationsSHIVANGI BAJPAINo ratings yet

- LKKLNDocument364 pagesLKKLNCy PanganibanNo ratings yet

- Who is the 420 CM of Andhra PradeshDocument1 pageWho is the 420 CM of Andhra Pradeshprabhu chand alluriNo ratings yet

- Full Test Bank For CCH Federal Taxation Comprehensive Topics 2014 Harmelink 080802972X PDF Docx Full Chapter ChapterDocument36 pagesFull Test Bank For CCH Federal Taxation Comprehensive Topics 2014 Harmelink 080802972X PDF Docx Full Chapter Chapterfuze.riddle.ghik9100% (11)

- Thesis Public Administration PDFDocument10 pagesThesis Public Administration PDFraxdouvcf100% (2)

- Satinder BabejaDocument30 pagesSatinder BabejaduthindaraNo ratings yet

- People vs. DagsaDocument3 pagesPeople vs. DagsaRobNo ratings yet

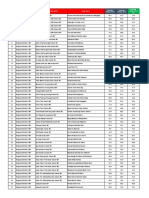

- No. Branch (Mar 2022) Legal Name Organization Level 4 (1 Mar 2022) Average TE/day, 2019 Average TE/day, 2020 Average TE/day, 2021 (A)Document7 pagesNo. Branch (Mar 2022) Legal Name Organization Level 4 (1 Mar 2022) Average TE/day, 2019 Average TE/day, 2020 Average TE/day, 2021 (A)Irfan JauhariNo ratings yet

- Motion For Extension of Time To Serve Complaint, U.S. Ex Rel. Schneider V JPMC 13-01223, D.E. 49Document2 pagesMotion For Extension of Time To Serve Complaint, U.S. Ex Rel. Schneider V JPMC 13-01223, D.E. 49larry-612445No ratings yet

- UCSP - ReviewerDocument7 pagesUCSP - ReviewerMaria Carmie AguilarNo ratings yet

- Political Law Reviewer 2018 Part 1 Atty. MedinaDocument95 pagesPolitical Law Reviewer 2018 Part 1 Atty. MedinayvonneNo ratings yet

- 509 Assignment-1Document11 pages509 Assignment-1mayani musumaliNo ratings yet

- Sanitizer TenderDocument24 pagesSanitizer TenderasdfNo ratings yet

- Business Finance Q4 Module 2Document16 pagesBusiness Finance Q4 Module 2randy magbudhi100% (14)

- Ohio Domestic Violence Fatalities 2022Document2 pagesOhio Domestic Violence Fatalities 2022Sarah McRitchieNo ratings yet