You might also like

- The Valuation of Digital Intangibles: Technology, Marketing and InternetFrom EverandThe Valuation of Digital Intangibles: Technology, Marketing and InternetNo ratings yet

- 2018 MDC FS V2Document24 pages2018 MDC FS V2Paul Mart TisoyNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- PT Indo PerkasaDocument34 pagesPT Indo PerkasaPriska NuriskaNo ratings yet

- Aspin Kemp - Associates Holding Corp. Consolidated FS 2017 PDFDocument25 pagesAspin Kemp - Associates Holding Corp. Consolidated FS 2017 PDFAnonymous nVXCkl0ANo ratings yet

- MSA 1 Winter 2018Document17 pagesMSA 1 Winter 2018Faisal Abbas MB-19-47No ratings yet

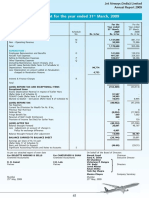

- Chapter-5 Analysis of Financial Statement: Statement of Profit & Loss Account For The Year Ended 31 MarchDocument5 pagesChapter-5 Analysis of Financial Statement: Statement of Profit & Loss Account For The Year Ended 31 MarchAcchu RNo ratings yet

- Antler Fabric Printers (PVT) LTD 2016Document37 pagesAntler Fabric Printers (PVT) LTD 2016IsuruNo ratings yet

- HBL FSAnnouncement 3Q2016Document9 pagesHBL FSAnnouncement 3Q2016Ryan Hock Keong TanNo ratings yet

- 2018 ResultsDocument36 pages2018 ResultstheredcornerNo ratings yet

- BPI Capital Audited Financial StatementsDocument66 pagesBPI Capital Audited Financial StatementsGes Glai-em BayabordaNo ratings yet

- 07 MalabonCity2018 - Part1 FSDocument8 pages07 MalabonCity2018 - Part1 FSJuan Uriel CruzNo ratings yet

- 4.1-Hortizontal/Trends Analysis: Chapter No # 4Document32 pages4.1-Hortizontal/Trends Analysis: Chapter No # 4Sadi ShahzadiNo ratings yet

- cAPITAL hOTELDocument41 pagescAPITAL hOTELFasasi Abdul Qodir AlabiNo ratings yet

- Cricket Canada FS FY 2017Document12 pagesCricket Canada FS FY 2017Ajay BhattNo ratings yet

- Starwood Hotels & Resorts Worldwide Inc. (HOT)Document14 pagesStarwood Hotels & Resorts Worldwide Inc. (HOT)assenav001No ratings yet

- Financial Statement Analysis: Kapuso O KapamilyaDocument51 pagesFinancial Statement Analysis: Kapuso O KapamilyaMark Angelo BustosNo ratings yet

- BCG Forage Core Strategy - Telco (Task 2 Additional Data) - UpdateDocument10 pagesBCG Forage Core Strategy - Telco (Task 2 Additional Data) - UpdateHằng TừNo ratings yet

- FS - Baltazar, Fatima S. 2020Document50 pagesFS - Baltazar, Fatima S. 2020Ma Teresa B. CerezoNo ratings yet

- KFin Technologies - Flash Note - 12 Dec 23Document6 pagesKFin Technologies - Flash Note - 12 Dec 23palakNo ratings yet

- Petron F (1) .S 3Document74 pagesPetron F (1) .S 3cieloville06100% (1)

- Statement of Financial Position: 2018 2017 (Rupees in Thousand)Document18 pagesStatement of Financial Position: 2018 2017 (Rupees in Thousand)Alina Binte EjazNo ratings yet

- Cobalto 1 PDFDocument22 pagesCobalto 1 PDFcristamaarNo ratings yet

- NIKL PR Aug 07 2020Document5 pagesNIKL PR Aug 07 2020Peter Paul RecaboNo ratings yet

- Chapter 6 PDFDocument23 pagesChapter 6 PDFreyNo ratings yet

- Awasr Oman Partners 2019Document44 pagesAwasr Oman Partners 2019abdullahsaleem91No ratings yet

- Question No.1: (3 Marks)Document25 pagesQuestion No.1: (3 Marks)Sudha SinghNo ratings yet

- Profit and Loss Account For The Year Ended 31 March, 2009: ST STDocument2 pagesProfit and Loss Account For The Year Ended 31 March, 2009: ST STRanjan DasguptaNo ratings yet

- Messenger 2018 FSDocument16 pagesMessenger 2018 FSNew Top Music VideosNo ratings yet

- Case Study - Financial Statements & Future ProspectsDocument8 pagesCase Study - Financial Statements & Future Prospectsmm3289No ratings yet

- Financial Statement For The Year Ended June 30 2017 PDFDocument72 pagesFinancial Statement For The Year Ended June 30 2017 PDFHussain AhmedNo ratings yet

- LACER - FS and Notes 2018 PDFDocument13 pagesLACER - FS and Notes 2018 PDFErben ReyesNo ratings yet

- Amounts in Philippine PesoDocument13 pagesAmounts in Philippine PesoJesse KentNo ratings yet

- Project Final 2Document8 pagesProject Final 2Nirob AhmedNo ratings yet

- Final Financial Reporting AssessmentDocument23 pagesFinal Financial Reporting Assessmentapi-413236814No ratings yet

- Company AssignmentDocument3 pagesCompany Assignmentrajeshparida9624No ratings yet

- Financial White Lotus Motors PVT - LTD - For The FY 2078-79Document117 pagesFinancial White Lotus Motors PVT - LTD - For The FY 2078-79Roshan PoudelNo ratings yet

- Case Study #3Document5 pagesCase Study #3Jenny OjoylanNo ratings yet

- Marta's Financial AspectDocument20 pagesMarta's Financial AspectMarvin GamboaNo ratings yet

- 7 11 Capital ManagementDocument6 pages7 11 Capital ManagementRonaldo ConventoNo ratings yet

- Financial Statements Year Ended December 31, 20X5: ABC CompanyDocument8 pagesFinancial Statements Year Ended December 31, 20X5: ABC CompanysaraNo ratings yet

- Lã Minh Ngọc - 18071385 - INS3007Document15 pagesLã Minh Ngọc - 18071385 - INS3007Ming NgọhNo ratings yet

- Cap II Group I RTP Dec2023Document84 pagesCap II Group I RTP Dec2023pratyushmudbhari340No ratings yet

- ARL Annual 2017Document97 pagesARL Annual 2017rehan naeemNo ratings yet

- 2-Annex A Cpfi Afs ConsoDocument97 pages2-Annex A Cpfi Afs ConsoCynthia PenoliarNo ratings yet

- Cadillac Ventures Inc. (A Development Stage Company) Interim Consolidated Financial Statements For The Three and Six Months Ended November 30, 2007 (Expressed in Canadian Dollars) (Unaudited)Document16 pagesCadillac Ventures Inc. (A Development Stage Company) Interim Consolidated Financial Statements For The Three and Six Months Ended November 30, 2007 (Expressed in Canadian Dollars) (Unaudited)CadVentNo ratings yet

- LG Chem, Ltd. and Subsidiaries: Consolidated Interim Financial Statements June 30, 2018 and 2017Document72 pagesLG Chem, Ltd. and Subsidiaries: Consolidated Interim Financial Statements June 30, 2018 and 2017enrique serrano100% (1)

- Delta Corp East Africa Limited (In Liquidation)Document22 pagesDelta Corp East Africa Limited (In Liquidation)LamineNo ratings yet

- QUCT 2016 FinancialsDocument24 pagesQUCT 2016 FinancialskdwcapitalNo ratings yet

- MABALAZADocument4 pagesMABALAZAMahasa R HajiiNo ratings yet

- Practice Questions For Final W Brick FinancialsDocument7 pagesPractice Questions For Final W Brick FinancialsJoana SilvaNo ratings yet

- IFAC 2018 Financial Statements PDFDocument32 pagesIFAC 2018 Financial Statements PDFsonia JavedNo ratings yet

- SPL - 3rd QTR BL-PNL-DEC 2018-2019 (Full)Document17 pagesSPL - 3rd QTR BL-PNL-DEC 2018-2019 (Full)MedulNo ratings yet

- 2013 Financial ReportDocument36 pages2013 Financial Reportvijay dharmavaramNo ratings yet

- Afs Ekcl 2017Document67 pagesAfs Ekcl 2017Tonmoy ParthoNo ratings yet

- ABS CBN CorporationDocument16 pagesABS CBN CorporationAlyssa BeatriceNo ratings yet

- Case Study FinalDocument47 pagesCase Study FinalVan Errl Nicolai SantosNo ratings yet

- Cash Flow From Assets - Solution PDFDocument3 pagesCash Flow From Assets - Solution PDFSeptian Sugestyo PutroNo ratings yet

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document3 pagesStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- Orth Annabis ORP: Condensed Interim Consolidated Financial Statements (Unaudited) As at March 31, 2020Document25 pagesOrth Annabis ORP: Condensed Interim Consolidated Financial Statements (Unaudited) As at March 31, 2020stonerhinoNo ratings yet

- Capital Structure Analysis of TriveniDocument73 pagesCapital Structure Analysis of Trivenisurender_singh0092100% (5)

- Chapter 10a - Long Term Finance - BondsDocument6 pagesChapter 10a - Long Term Finance - BondsTAN YUN YUNNo ratings yet

- Far670 Group Report - Group 2 (Kac2208c)Document23 pagesFar670 Group Report - Group 2 (Kac2208c)NURUL SYAFIQAH MOHD IDRIS50% (2)

- Pefindo'S Corporate and Corporate Debt Securities Default Study 2007-2019Document35 pagesPefindo'S Corporate and Corporate Debt Securities Default Study 2007-2019Bangkit ZuasNo ratings yet

- Debtocracy : On The Title: It Is A Neologism Between Debt and Democracy Since Greece Is The Cradle of DemocracyDocument1 pageDebtocracy : On The Title: It Is A Neologism Between Debt and Democracy Since Greece Is The Cradle of DemocracyEliezer MPianoNo ratings yet

- 633833334841206250Document57 pages633833334841206250Ritesh Kumar Dubey100% (1)

- Financial Performance Analysis of Kotak Mahindra BankDocument60 pagesFinancial Performance Analysis of Kotak Mahindra Bankvaibhav pachputeNo ratings yet

- Chapter 07-Bank Loans: Name: Class: DateDocument11 pagesChapter 07-Bank Loans: Name: Class: DateLê Đặng Minh ThảoNo ratings yet

- Ethiopian Bankruptcy Law A Commentary Part I PDFDocument41 pagesEthiopian Bankruptcy Law A Commentary Part I PDFAnonymous dLIq7U3DKz100% (2)

- Personal Finance Canadian Canadian 5th Edition Kapoor Test BankDocument25 pagesPersonal Finance Canadian Canadian 5th Edition Kapoor Test BankMollyMoralescowyxefb100% (43)

- Kamadhenu Feeds PVT LTD: Standalone Financial Statements For Period 01/04/2017 To 31/03/2018Document72 pagesKamadhenu Feeds PVT LTD: Standalone Financial Statements For Period 01/04/2017 To 31/03/2018bhalakankshaNo ratings yet

- Assignment - Corporate FinanceDocument9 pagesAssignment - Corporate FinanceShivam GoelNo ratings yet

- Assignment No. 1: Course Name: "Financial Reporting and Disclosure" Submitted byDocument7 pagesAssignment No. 1: Course Name: "Financial Reporting and Disclosure" Submitted byMUHAMMAD UMARNo ratings yet

- FMGTDocument40 pagesFMGTbindrapalak1905No ratings yet

- Statistik Perusahaan Pergadaian Indonesia - Februari 2023Document16 pagesStatistik Perusahaan Pergadaian Indonesia - Februari 2023SiskaratriNo ratings yet

- Eun Resnick 8e Chapter 11Document18 pagesEun Resnick 8e Chapter 11Wai Man NgNo ratings yet

- Financial Management: FINA 6212Document81 pagesFinancial Management: FINA 6212Yuhan KENo ratings yet

- Choice Between Debt and Equity and Its Impact On Business PerformanceDocument13 pagesChoice Between Debt and Equity and Its Impact On Business PerformanceAvinash aviNo ratings yet

- Afs ProjectDocument37 pagesAfs ProjectNuman RoxNo ratings yet

- Credit and CollectionDocument116 pagesCredit and Collectionhadassah Villar100% (14)

- Final Term Paper PDFDocument45 pagesFinal Term Paper PDFAfsana arefin PriyaNo ratings yet

- Bhushan Steel Project But Not GoodDocument48 pagesBhushan Steel Project But Not Goodchauhanbrothers3423No ratings yet

- Tax-Exempt Private Activity Bonds, 1988-1995: by Sarah E. NutterDocument16 pagesTax-Exempt Private Activity Bonds, 1988-1995: by Sarah E. NutterIRSNo ratings yet

- MCQ's Total Marks 100: Sbp-Sbots (Get-Fs) Sunday, October 14, 2012Document13 pagesMCQ's Total Marks 100: Sbp-Sbots (Get-Fs) Sunday, October 14, 2012ShakeelNo ratings yet

- Edurev: Case Studies - (Chapter - 9) Financial Management, BST Class 12Document20 pagesEdurev: Case Studies - (Chapter - 9) Financial Management, BST Class 12Heer SirwaniNo ratings yet

- Sample Questions of Venture Capital and Private EquityDocument3 pagesSample Questions of Venture Capital and Private EquityvijaygawdeNo ratings yet

- SR Bills and DepreciationDocument2 pagesSR Bills and DepreciationM JEEVARATHNAM NAIDUNo ratings yet

- Introduction To Financial Modelling PDFDocument18 pagesIntroduction To Financial Modelling PDFJeffrey Millinger50% (2)

- Fria Law: Sole Proprietorship Duly Registered With The Department of Trade and Industry (DTIDocument10 pagesFria Law: Sole Proprietorship Duly Registered With The Department of Trade and Industry (DTIReigh Harvy CantaNo ratings yet

- Business Law A2 Mai Huong (Recovered)Document6 pagesBusiness Law A2 Mai Huong (Recovered)Mai HươngNo ratings yet

- Nine Black Robes: Inside the Supreme Court's Drive to the Right and Its Historic ConsequencesFrom EverandNine Black Robes: Inside the Supreme Court's Drive to the Right and Its Historic ConsequencesNo ratings yet

- For the Thrill of It: Leopold, Loeb, and the Murder That Shocked Jazz Age ChicagoFrom EverandFor the Thrill of It: Leopold, Loeb, and the Murder That Shocked Jazz Age ChicagoRating: 4 out of 5 stars4/5 (97)

- Perversion of Justice: The Jeffrey Epstein StoryFrom EverandPerversion of Justice: The Jeffrey Epstein StoryRating: 4.5 out of 5 stars4.5/5 (10)

- The Internet Con: How to Seize the Means of ComputationFrom EverandThe Internet Con: How to Seize the Means of ComputationRating: 5 out of 5 stars5/5 (6)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingFrom EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingRating: 4.5 out of 5 stars4.5/5 (97)

- Summary: Surrounded by Idiots: The Four Types of Human Behavior and How to Effectively Communicate with Each in Business (and in Life) by Thomas Erikson: Key Takeaways, Summary & AnalysisFrom EverandSummary: Surrounded by Idiots: The Four Types of Human Behavior and How to Effectively Communicate with Each in Business (and in Life) by Thomas Erikson: Key Takeaways, Summary & AnalysisRating: 4 out of 5 stars4/5 (2)

- Get Outta Jail Free Card “Jim Crow’s last stand at perpetuating slavery” Non-Unanimous Jury Verdicts & Voter SuppressionFrom EverandGet Outta Jail Free Card “Jim Crow’s last stand at perpetuating slavery” Non-Unanimous Jury Verdicts & Voter SuppressionRating: 5 out of 5 stars5/5 (1)

- Reading the Constitution: Why I Chose Pragmatism, not TextualismFrom EverandReading the Constitution: Why I Chose Pragmatism, not TextualismNo ratings yet

- Hunting Whitey: The Inside Story of the Capture & Killing of America's Most Wanted Crime BossFrom EverandHunting Whitey: The Inside Story of the Capture & Killing of America's Most Wanted Crime BossRating: 3.5 out of 5 stars3.5/5 (6)

- Learning to Disagree: The Surprising Path to Navigating Differences with Empathy and RespectFrom EverandLearning to Disagree: The Surprising Path to Navigating Differences with Empathy and RespectNo ratings yet

- Reasonable Doubts: The O.J. Simpson Case and the Criminal Justice SystemFrom EverandReasonable Doubts: The O.J. Simpson Case and the Criminal Justice SystemRating: 4 out of 5 stars4/5 (25)

- Lady Killers: Deadly Women Throughout HistoryFrom EverandLady Killers: Deadly Women Throughout HistoryRating: 4 out of 5 stars4/5 (154)

- Conviction: The Untold Story of Putting Jodi Arias Behind BarsFrom EverandConviction: The Untold Story of Putting Jodi Arias Behind BarsRating: 4.5 out of 5 stars4.5/5 (16)

- Beyond the Body Farm: A Legendary Bone Detective Explores Murders, Mysteries, and the Revolution in Forensic ScienceFrom EverandBeyond the Body Farm: A Legendary Bone Detective Explores Murders, Mysteries, and the Revolution in Forensic ScienceRating: 4 out of 5 stars4/5 (107)

- The Killer Across the Table: Unlocking the Secrets of Serial Killers and Predators with the FBI's Original MindhunterFrom EverandThe Killer Across the Table: Unlocking the Secrets of Serial Killers and Predators with the FBI's Original MindhunterRating: 4.5 out of 5 stars4.5/5 (456)

- The Edge of Innocence: The Trial of Casper BennettFrom EverandThe Edge of Innocence: The Trial of Casper BennettRating: 4.5 out of 5 stars4.5/5 (3)

- The Dark Net: Inside the Digital UnderworldFrom EverandThe Dark Net: Inside the Digital UnderworldRating: 3.5 out of 5 stars3.5/5 (104)

- Chokepoint Capitalism: How Big Tech and Big Content Captured Creative Labor Markets and How We'll Win Them BackFrom EverandChokepoint Capitalism: How Big Tech and Big Content Captured Creative Labor Markets and How We'll Win Them BackRating: 5 out of 5 stars5/5 (20)

- The Death of Punishment: Searching for Justice among the Worst of the WorstFrom EverandThe Death of Punishment: Searching for Justice among the Worst of the WorstNo ratings yet

- Can't Forgive: My 20-Year Battle With O.J. SimpsonFrom EverandCan't Forgive: My 20-Year Battle With O.J. SimpsonRating: 3 out of 5 stars3/5 (3)

- Free & Clear, Standing & Quiet Title: 11 Possible Ways to Get Rid of Your MortgageFrom EverandFree & Clear, Standing & Quiet Title: 11 Possible Ways to Get Rid of Your MortgageRating: 2 out of 5 stars2/5 (3)