You might also like

- Electronic Trading Tutorial: (Page 1 of 8)Document8 pagesElectronic Trading Tutorial: (Page 1 of 8)Nazib LeeNo ratings yet

- Quote Driven MarketDocument2 pagesQuote Driven Marketkurdiausha29No ratings yet

- Technical and Fundamental AnalysisDocument75 pagesTechnical and Fundamental Analysiseuge_prime2001No ratings yet

- 2 How Securities Are TradedDocument23 pages2 How Securities Are TradedJenny PabualanNo ratings yet

- Option Chain Part1Document3 pagesOption Chain Part1ramyatan SinghNo ratings yet

- NISM XB Invt Advisor 2 Short NotesDocument32 pagesNISM XB Invt Advisor 2 Short NotesAnchal100% (1)

- Stock Market An Over ViewDocument14 pagesStock Market An Over Viewrobin boseNo ratings yet

- A STUDY ON INDIAN FinalDocument80 pagesA STUDY ON INDIAN FinalAnkita SolankiNo ratings yet

- Market Chapter OneDocument11 pagesMarket Chapter Onehaifa.s.mansourNo ratings yet

- The Stock Market The Stock Market: Fundamentals InvestmentsDocument40 pagesThe Stock Market The Stock Market: Fundamentals Investmentsfaisal197No ratings yet

- Role and Function of The Secondary Market: LiquidityDocument14 pagesRole and Function of The Secondary Market: LiquidityHerojianbuNo ratings yet

- Stock Exchange MechanismDocument24 pagesStock Exchange MechanismSandeep Sandeep SinghNo ratings yet

- Topic 3Document4 pagesTopic 3Regine TorrelizaNo ratings yet

- CH-4 - Organization and Functioning of Securities MarketDocument13 pagesCH-4 - Organization and Functioning of Securities MarketMoin khanNo ratings yet

- MarkersDocument1 pageMarkersAlinaVieruNo ratings yet

- Chapter 12Document10 pagesChapter 12Ana JikiaNo ratings yet

- How Securities Are TradedDocument32 pagesHow Securities Are TradedZawad47 AhaNo ratings yet

- Zaky Zaljuhdi 1401103010148Document5 pagesZaky Zaljuhdi 1401103010148Zaky ZaljuhdiNo ratings yet

- Raj Institute of Finance & Marketing: One Day Crash Course in Financial MarketsDocument29 pagesRaj Institute of Finance & Marketing: One Day Crash Course in Financial MarketsRudrajit GhoshNo ratings yet

- FMM 12Document18 pagesFMM 12gameofgreed876No ratings yet

- Chap 1Document24 pagesChap 1haifa.s.mansourNo ratings yet

- Functions of Secondary MarketDocument7 pagesFunctions of Secondary MarketshugugaurNo ratings yet

- Kind of Stock BrokersDocument4 pagesKind of Stock BrokersImran HassanNo ratings yet

- FNM 104 Finals LectureDocument19 pagesFNM 104 Finals LectureNovelyn DuyoganNo ratings yet

- Inv Lectures FinalsDocument5 pagesInv Lectures FinalsShiela Mae Gabrielle AladoNo ratings yet

- What's An Index?Document23 pagesWhat's An Index?deepani_446621No ratings yet

- How ETFs WorkDocument8 pagesHow ETFs WorkJack Hyunsoo KimNo ratings yet

- Full Thesis Derivatives DyaneshwarDocument46 pagesFull Thesis Derivatives Dyaneshwaryograj DubeNo ratings yet

- Nism Xiii Common Derivatives Short NotesDocument64 pagesNism Xiii Common Derivatives Short NotesAnsh DoshiNo ratings yet

- Online Trading SantuDocument101 pagesOnline Trading SantuAashi YadavNo ratings yet

- Q. 10 Benefits of DerivativesDocument2 pagesQ. 10 Benefits of DerivativesMAHENDRA SHIVAJI DHENAK100% (1)

- Fin208 Ca2Document12 pagesFin208 Ca2sehajpal6943No ratings yet

- DerivativesDocument48 pagesDerivativesBapiraj MallipudiNo ratings yet

- Silber - 1984 - Marketmaker Behavior in An Auction Market, An Analysis of Scalpers in Futures MarketsDocument18 pagesSilber - 1984 - Marketmaker Behavior in An Auction Market, An Analysis of Scalpers in Futures MarketsjpkoningNo ratings yet

- Module 2 Part 2Document65 pagesModule 2 Part 2Shivam AroraNo ratings yet

- Smo Unit 1 NotesDocument15 pagesSmo Unit 1 NotesashlynnahaNo ratings yet

- Assignment Stock MarketDocument16 pagesAssignment Stock MarketDeepikaSaini75% (4)

- Course Overview: CME Group Courses Module 3Document8 pagesCourse Overview: CME Group Courses Module 3Darren FNo ratings yet

- Understanding Level 2 and Market MakersDocument4 pagesUnderstanding Level 2 and Market Makers5_percenter100% (14)

- Derivatives in IndiaDocument55 pagesDerivatives in IndiaDashrath DholeNo ratings yet

- Assumptions of CAPM: Rate of Return Asset Portfolio DiversifiableDocument10 pagesAssumptions of CAPM: Rate of Return Asset Portfolio Diversifiableখালেদ কায়ছার রনিNo ratings yet

- Stock MarketDocument3 pagesStock MarketDanial KhawajaNo ratings yet

- Financial Matter1 PDFDocument42 pagesFinancial Matter1 PDFDrNaveed Ul HaqNo ratings yet

- Stokc ExhangeDocument11 pagesStokc Exhange✬ SHANZA MALIK ✬No ratings yet

- Chapter 13 The Stock MarketDocument7 pagesChapter 13 The Stock Marketlasha KachkachishviliNo ratings yet

- Investment Chapter 4 Organizing SecuritiesDocument15 pagesInvestment Chapter 4 Organizing SecuritiesEsraa TarekNo ratings yet

- Stock Market How It WorksDocument3 pagesStock Market How It WorksMeghananda s oNo ratings yet

- Equity Market: Sub-Parts DescriptionDocument5 pagesEquity Market: Sub-Parts Descriptionalajar opticalNo ratings yet

- Financial Economics 2007 Lecture 6 Slides..Document20 pagesFinancial Economics 2007 Lecture 6 Slides..pkc6465504No ratings yet

- Session 2 Trading: Dr. Himanshu JoshiDocument50 pagesSession 2 Trading: Dr. Himanshu JoshiKANVI KAUSHIKNo ratings yet

- Option Strategies Kay 2016Document78 pagesOption Strategies Kay 2016ravi gantaNo ratings yet

- Introduction To DeivativesDocument44 pagesIntroduction To Deivativesanirbanccim8493No ratings yet

- Common Stock Basics-1Document37 pagesCommon Stock Basics-1Exclusively Farhana'sNo ratings yet

- How Do The Stock Market Works?Document48 pagesHow Do The Stock Market Works?Jezza Mae Gomba RegidorNo ratings yet

- Structure of Equity MarketDocument16 pagesStructure of Equity MarketMahar Kamran AshiqNo ratings yet

- Secondary Market StructureDocument13 pagesSecondary Market StructureTanvir Hasan SohanNo ratings yet

- Evaluation of Investor Awareness On Techniques UseDocument12 pagesEvaluation of Investor Awareness On Techniques UseRonat JainNo ratings yet

- Topic 7 Equity MarketsDocument25 pagesTopic 7 Equity MarketsKelly Chan Yun JieNo ratings yet

- Dym Sew Kaczm AstocktradingexpertsystemDocument22 pagesDym Sew Kaczm Astocktradingexpertsystemluca pilottiNo ratings yet

- 0+ - A Double Digit Sharpe HFT StrategyDocument17 pages0+ - A Double Digit Sharpe HFT Strategyluca pilottiNo ratings yet

- Calculate Information Ratio With ExcelDocument2 pagesCalculate Information Ratio With Excelluca pilottiNo ratings yet

- Quanto Option Fixed Rate Foreign EquityDocument1 pageQuanto Option Fixed Rate Foreign Equityluca pilottiNo ratings yet

- European Exchange OptionDocument1 pageEuropean Exchange Optionluca pilottiNo ratings yet

- Draft Ietf Calext Icalendar Jscalendar Extensions 00Document9 pagesDraft Ietf Calext Icalendar Jscalendar Extensions 00luca pilottiNo ratings yet

- How Long Is A .NET DateTime - TimeSpan Tick - Stack OverflowDocument3 pagesHow Long Is A .NET DateTime - TimeSpan Tick - Stack Overflowluca pilottiNo ratings yet

- Gap OptionsDocument1 pageGap Optionsluca pilottiNo ratings yet

- SupershareDocument1 pageSupershareluca pilottiNo ratings yet

- Asian OptionsDocument2 pagesAsian Optionsluca pilottiNo ratings yet

- Templates - JasonetteDocument18 pagesTemplates - Jasonetteluca pilottiNo ratings yet

- The Market Structure Crisis Electronic Stock Markets, High Frequency Trading, and Dark Pools (Haim Bodek, Stanislav Dolgopolov) (Z-Library)Document163 pagesThe Market Structure Crisis Electronic Stock Markets, High Frequency Trading, and Dark Pools (Haim Bodek, Stanislav Dolgopolov) (Z-Library)luca pilottiNo ratings yet

- Probacktest 7e032d14Document104 pagesProbacktest 7e032d14luca pilottiNo ratings yet

- Camarilla Pivot PointsDocument1 pageCamarilla Pivot Pointsluca pilottiNo ratings yet

- Trading With Pivot Points - Understanding The Ins, Outs and FormulasDocument8 pagesTrading With Pivot Points - Understanding The Ins, Outs and Formulasluca pilottiNo ratings yet

- ADBB18AB PivotPointsTradingStrategyDocument6 pagesADBB18AB PivotPointsTradingStrategyluca pilottiNo ratings yet

- Sierra Chart-Bar Time DurationDocument2 pagesSierra Chart-Bar Time Durationluca pilottiNo ratings yet

- Sierra Chart-Range Bar PredictorDocument2 pagesSierra Chart-Range Bar Predictorluca pilottiNo ratings yet

- Continued Fractions - Sacred GeometryDocument13 pagesContinued Fractions - Sacred Geometryluca pilottiNo ratings yet

- Sierra Chart-Square of 9Document4 pagesSierra Chart-Square of 9luca pilottiNo ratings yet

- DeMark Pivot Points Definition - MyPivotsDocument1 pageDeMark Pivot Points Definition - MyPivotsluca pilottiNo ratings yet

- Woodie Pivot Points Definition - MyPivotsDocument1 pageWoodie Pivot Points Definition - MyPivotsluca pilottiNo ratings yet

- DeMark Pivot PointsDocument1 pageDeMark Pivot Pointsluca pilottiNo ratings yet

- How Are The Pivot Points Derived While Using The Central Pivot Range (CPR)Document2 pagesHow Are The Pivot Points Derived While Using The Central Pivot Range (CPR)luca pilottiNo ratings yet

- Pivot Points - How To Calculate (Explanation & Examples)Document6 pagesPivot Points - How To Calculate (Explanation & Examples)luca pilottiNo ratings yet

- PIVOT (Pivot Levels)Document3 pagesPIVOT (Pivot Levels)luca pilottiNo ratings yet

- Does Anonymity Matter in Electronic Limit Order Markets?Document47 pagesDoes Anonymity Matter in Electronic Limit Order Markets?luca pilottiNo ratings yet

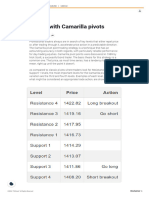

- Trading Stocks With Camarilla PivotsDocument6 pagesTrading Stocks With Camarilla Pivotsluca pilottiNo ratings yet

- FWD 3Document53 pagesFWD 3luca pilottiNo ratings yet

- Modern Retail Needs Modern Rules - NasdaqDocument4 pagesModern Retail Needs Modern Rules - Nasdaqluca pilottiNo ratings yet

- Trump Inaugural Big DonorsDocument2 pagesTrump Inaugural Big DonorsChristina Wilkie100% (4)

- Suhail Khan Bank Statement 02-09-2021Document4 pagesSuhail Khan Bank Statement 02-09-2021Suhail KhanNo ratings yet

- Russell 2000 Membership ListDocument26 pagesRussell 2000 Membership ListSatyabrota DasNo ratings yet

- Divestment List Latest PDFDocument32 pagesDivestment List Latest PDFYongky ANo ratings yet

- Russell3000 Membership List 2011Document38 pagesRussell3000 Membership List 2011trgnicoleNo ratings yet

- Paypal ByvbDocument8 pagesPaypal Byvbadilson100% (1)

- Norwey Pharmaceuticals Drug Medicine Package Prices 2013-04-01Document780 pagesNorwey Pharmaceuticals Drug Medicine Package Prices 2013-04-01Anuj MairhNo ratings yet

- High Frequency Trading - Shawn DurraniDocument49 pagesHigh Frequency Trading - Shawn DurraniShawnDurraniNo ratings yet

- Brenda Lange - The Stock Market Crash of 1929 The End of Prosperity by Brenda LangeDocument122 pagesBrenda Lange - The Stock Market Crash of 1929 The End of Prosperity by Brenda LangeSiwakorn SangwornNo ratings yet

- Virginia HarrasmentDocument41 pagesVirginia HarrasmentJoseph Matthias Zao100% (1)

- Re Its 16052021Document21 pagesRe Its 16052021Ricardo LimaNo ratings yet

- WachagonaduDocument2 pagesWachagonaduRich LDNo ratings yet

- Ticker Company Name ISIN CodeDocument13 pagesTicker Company Name ISIN CodeshoaibNo ratings yet

- Syllabus 1532088641Document91 pagesSyllabus 1532088641aman3327No ratings yet

- Russell 2000 Value Membership ListDocument18 pagesRussell 2000 Value Membership ListSatyabrota DasNo ratings yet

- Fortune 1000 US List 2019 - Someka V1Document8 pagesFortune 1000 US List 2019 - Someka V1Brajesh Kumar SinghNo ratings yet

- Sydney 1757414384Document3 pagesSydney 1757414384otsrNo ratings yet

- 2022 Fortune 500 List of Companies in The World in Xls FormatDocument127 pages2022 Fortune 500 List of Companies in The World in Xls FormatMohammed showkatNo ratings yet

- LN-Session 2-Chapter 3-How Securities Are TradedDocument72 pagesLN-Session 2-Chapter 3-How Securities Are Tradedchaudhari vishalNo ratings yet

- OGI Who'SWho 2011Document76 pagesOGI Who'SWho 2011spinsta11100% (1)

- NYSEDocument7 pagesNYSEJitender Thakur50% (2)

- 2020 CAGNY Conference Participating Company List PDFDocument3 pages2020 CAGNY Conference Participating Company List PDFjiayi1No ratings yet

- Credit Card GeneratorDocument2 pagesCredit Card GeneratorStefan Radu100% (11)

- Investment Banking Summer Internship OpportunitiesDocument5 pagesInvestment Banking Summer Internship OpportunitiesAzzurra123No ratings yet

- Intermodal Weekly 16-2013Document8 pagesIntermodal Weekly 16-2013Wisnu KertaningnagoroNo ratings yet

- New York Stock ExchangeDocument9 pagesNew York Stock ExchangeMahendra SharmaNo ratings yet

- Lista de PedidosDocument15 pagesLista de PedidosSergio HenriqueNo ratings yet

- Creditcardrush JSONDocument31 pagesCreditcardrush JSONReymark Baldo100% (1)

- TOP 100 of "Fortune 500": Rank Company Revenues ($ Millions) Profits ($ Millions)Document4 pagesTOP 100 of "Fortune 500": Rank Company Revenues ($ Millions) Profits ($ Millions)jyoti verma100% (2)

- UntitledDocument8 pagesUntitledPreeti SinghNo ratings yet