You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- PDF 379546690310722Document1 pagePDF 379546690310722DarshanNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Ceigall India Limited: (ICRA) A - (Stable) Assigned: Summary of Rating ActionDocument7 pagesCeigall India Limited: (ICRA) A - (Stable) Assigned: Summary of Rating ActionDarshanNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Obeetee Textiles - R-10122020Document7 pagesObeetee Textiles - R-10122020DarshanNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- 24x7 Powerline CUSTOMER CARE CENTRE/CORRESPONDENCE ADDRESS/INTERNAL GRIEVANCE REDRESSAL CELL (IGRCDocument2 pages24x7 Powerline CUSTOMER CARE CENTRE/CORRESPONDENCE ADDRESS/INTERNAL GRIEVANCE REDRESSAL CELL (IGRCDarshanNo ratings yet

- Gipsa Chairmans ReplyDocument1 pageGipsa Chairmans ReplyDarshanNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Link 6Document1 pageLink 6DarshanNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- February 2021Document670 pagesFebruary 2021DarshanNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Advisory For Performing Marriages & EventsDocument2 pagesAdvisory For Performing Marriages & EventsDarshanNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- HealthCaps India Limited - R - 02122020Document8 pagesHealthCaps India Limited - R - 02122020DarshanNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Environmental Baseline of Orphanages in BangaloreDocument68 pagesEnvironmental Baseline of Orphanages in BangaloreDarshan0% (1)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Aventis Pharma to acquire Universal Medicare's nutraceutical businessDocument2 pagesAventis Pharma to acquire Universal Medicare's nutraceutical businessDarshanNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Saregama India Limited - R - 27112020Document8 pagesSaregama India Limited - R - 27112020DarshanNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Link 9Document25 pagesLink 9DarshanNo ratings yet

- Mahesh Value Products Private - R - 03122020Document6 pagesMahesh Value Products Private - R - 03122020DarshanNo ratings yet

- Mutual Nondisclosure AgreementDocument3 pagesMutual Nondisclosure AgreementDarshanNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- HealthCaps India Limited - R - 02122020Document8 pagesHealthCaps India Limited - R - 02122020DarshanNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Scorpios Apparels Private - R - 25112020Document6 pagesScorpios Apparels Private - R - 25112020DarshanNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Sun Home Appliances Private - R - 25082020Document7 pagesSun Home Appliances Private - R - 25082020DarshanNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Rreconstituted DCfor Machine Tools Indust 0001Document9 pagesRreconstituted DCfor Machine Tools Indust 0001DarshanNo ratings yet

- Prateek Wires (P) LTD - R - 08102020Document6 pagesPrateek Wires (P) LTD - R - 08102020DarshanNo ratings yet

- Company Address Details For The Year 2020 Packer of TobaccoDocument2 pagesCompany Address Details For The Year 2020 Packer of TobaccoDarshanNo ratings yet

- Team Computers Private - R - 09102020Document8 pagesTeam Computers Private - R - 09102020DarshanNo ratings yet

- Sanghi Jewellers PVT - R - 20102020Document7 pagesSanghi Jewellers PVT - R - 20102020DarshanNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Palamur Biosciences Private - R - 15102020Document7 pagesPalamur Biosciences Private - R - 15102020DarshanNo ratings yet

- MSL Driveline Systems - R - 16102020Document8 pagesMSL Driveline Systems - R - 16102020DarshanNo ratings yet

- Zenith Precision PVT LTD - R - 23102020Document7 pagesZenith Precision PVT LTD - R - 23102020DarshanNo ratings yet

- Pondy Oxides and Chemicals 22apr2019Document6 pagesPondy Oxides and Chemicals 22apr2019DarshanNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Bharat Fritz Werner Limited - R - 16102020Document7 pagesBharat Fritz Werner Limited - R - 16102020DarshanNo ratings yet

- Ashoka Concessions Limited - R - 16102020Document8 pagesAshoka Concessions Limited - R - 16102020DarshanNo ratings yet

- RSPL Limited - R - 16102020Document8 pagesRSPL Limited - R - 16102020DarshanNo ratings yet

- Our Town November 30, 1944Document4 pagesOur Town November 30, 1944narberthcivicNo ratings yet

- SJFM Coop ByLawsDocument10 pagesSJFM Coop ByLawsruth sab-itNo ratings yet

- Pump Quotation DetailsDocument2 pagesPump Quotation Detailsdhavalesh1No ratings yet

- Chapter 7 Acctg For Financial InstrumentsDocument32 pagesChapter 7 Acctg For Financial InstrumentsjammuuuNo ratings yet

- Section 2. Original Certificates of Title Shall Be Reconstituted From Such of TheDocument2 pagesSection 2. Original Certificates of Title Shall Be Reconstituted From Such of TheAlexylle ConcepcionNo ratings yet

- Mechanics Liens in Practice Contractor Rights NC W 015 8524Document7 pagesMechanics Liens in Practice Contractor Rights NC W 015 8524Brandace HopperNo ratings yet

- Garcia vs. Court of AppealsDocument12 pagesGarcia vs. Court of AppealsJoannah SalamatNo ratings yet

- HandelsbankenDocument37 pagesHandelsbankenFrank CalbergNo ratings yet

- Manual Instructions Surcharge 80EEBDocument11 pagesManual Instructions Surcharge 80EEBSuprasannaPradhanNo ratings yet

- MBA 631rift Valley OutlineDocument4 pagesMBA 631rift Valley OutlineTatekia DanielNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- FHA Credit Policy Manual GuideDocument146 pagesFHA Credit Policy Manual GuideWeb BinghamNo ratings yet

- Three Point SystemDocument2 pagesThree Point SystemtrionjetNo ratings yet

- Vietnamese Law On Credit InstitutionDocument101 pagesVietnamese Law On Credit InstitutionBosin NhiNo ratings yet

- Faysal BankDocument113 pagesFaysal BanksaharsaeedNo ratings yet

- 2015 SALN Form (PDF) 1 PDFDocument2 pages2015 SALN Form (PDF) 1 PDFAnonymous xJvt1QHseNo ratings yet

- Teacher's Manual - Financial Acctg 2Document233 pagesTeacher's Manual - Financial Acctg 2Adrian Mallari71% (21)

- A Study On Some Financial Ratios of Bangladeshi Companies by TURINDocument41 pagesA Study On Some Financial Ratios of Bangladeshi Companies by TURINTurin Iqbal100% (1)

- Chapter 6 Quiz KeyDocument3 pagesChapter 6 Quiz Keymar8357No ratings yet

- Top 15 Financial FunctionsDocument31 pagesTop 15 Financial Functionsv_u_ingle2003No ratings yet

- Almc - Cash Position - 11may2021Document246 pagesAlmc - Cash Position - 11may2021ACYATAN & CO., CPAs 2020No ratings yet

- Final Exam With AnswerDocument8 pagesFinal Exam With Answerg409863No ratings yet

- Who Is The Ostensible OwnerDocument10 pagesWho Is The Ostensible OwnerdeepakNo ratings yet

- Investor Presentation Highlights Hudbay's Diversified PortfolioDocument67 pagesInvestor Presentation Highlights Hudbay's Diversified PortfolioAndrewNo ratings yet

- PNB allowed to foreclose on mortgaged propertiesDocument2 pagesPNB allowed to foreclose on mortgaged propertiesRaymond ChengNo ratings yet

- Sri Sai Srinivasa Cotton Industries PVT LTDDocument36 pagesSri Sai Srinivasa Cotton Industries PVT LTDManisha NerellaNo ratings yet

- SEI INVESTMENTS CO 10-K (Annual Reports) 2009-02-25Document113 pagesSEI INVESTMENTS CO 10-K (Annual Reports) 2009-02-25http://secwatch.comNo ratings yet

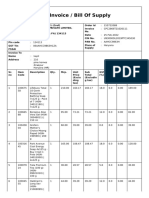

- Tax Invoice / Bill of SupplyDocument2 pagesTax Invoice / Bill of SupplyKapil SinglaNo ratings yet

- Davit Pivot Trading Intermediate Trade EvaluationDocument1 pageDavit Pivot Trading Intermediate Trade EvaluationBucur ImanuelNo ratings yet

- Education Loans For Higher StudiesDocument7 pagesEducation Loans For Higher StudiesSREYANo ratings yet

- Citibank SingaporeDocument8 pagesCitibank SingaporeYudis TiawanNo ratings yet

- The Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeFrom EverandThe Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeRating: 4.5 out of 5 stars4.5/5 (87)

- Summary of Zero to One: Notes on Startups, or How to Build the FutureFrom EverandSummary of Zero to One: Notes on Startups, or How to Build the FutureRating: 4.5 out of 5 stars4.5/5 (100)

- Transformed: Moving to the Product Operating ModelFrom EverandTransformed: Moving to the Product Operating ModelRating: 4 out of 5 stars4/5 (1)

- ChatGPT Side Hustles 2024 - Unlock the Digital Goldmine and Get AI Working for You Fast with More Than 85 Side Hustle Ideas to Boost Passive Income, Create New Cash Flow, and Get Ahead of the CurveFrom EverandChatGPT Side Hustles 2024 - Unlock the Digital Goldmine and Get AI Working for You Fast with More Than 85 Side Hustle Ideas to Boost Passive Income, Create New Cash Flow, and Get Ahead of the CurveNo ratings yet

- 12 Months to $1 Million: How to Pick a Winning Product, Build a Real Business, and Become a Seven-Figure EntrepreneurFrom Everand12 Months to $1 Million: How to Pick a Winning Product, Build a Real Business, and Become a Seven-Figure EntrepreneurRating: 4 out of 5 stars4/5 (2)

- Summary of The Subtle Art of Not Giving A F*ck: A Counterintuitive Approach to Living a Good Life by Mark Manson: Key Takeaways, Summary & Analysis IncludedFrom EverandSummary of The Subtle Art of Not Giving A F*ck: A Counterintuitive Approach to Living a Good Life by Mark Manson: Key Takeaways, Summary & Analysis IncludedRating: 4.5 out of 5 stars4.5/5 (38)

- SYSTEMology: Create time, reduce errors and scale your profits with proven business systemsFrom EverandSYSTEMology: Create time, reduce errors and scale your profits with proven business systemsRating: 5 out of 5 stars5/5 (48)

- Without a Doubt: How to Go from Underrated to UnbeatableFrom EverandWithout a Doubt: How to Go from Underrated to UnbeatableRating: 4 out of 5 stars4/5 (23)