You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5813)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- DMCC REG COMPANIES UpdatedDocument125 pagesDMCC REG COMPANIES UpdatedSajidZia75% (4)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- 1721 A1 English VersionDocument2 pages1721 A1 English VersionSeptian Bayu Kristanto43% (7)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Chapter Thirteen SolutionsDocument18 pagesChapter Thirteen Solutionsapi-3705855No ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Reward ManagementDocument15 pagesReward ManagementBuddhima De Silva100% (1)

- DXB To OsakaDocument1 pageDXB To OsakaSajidZiaNo ratings yet

- 205Document1 page205SajidZiaNo ratings yet

- DXB To Osaka 1-7 Aug AnjanaDocument1 pageDXB To Osaka 1-7 Aug AnjanaSajidZiaNo ratings yet

- Application For EmploymentDocument6 pagesApplication For EmploymentSajidZiaNo ratings yet

- Pradeep Chandelia: Sub: Appropriate Career Opening in Your Esteemed OrganizationDocument4 pagesPradeep Chandelia: Sub: Appropriate Career Opening in Your Esteemed OrganizationSajidZiaNo ratings yet

- PRADEEP CHANDELIA Resume PDFDocument3 pagesPRADEEP CHANDELIA Resume PDFSajidZiaNo ratings yet

- Employee Joining Report-2020Document1 pageEmployee Joining Report-2020SajidZiaNo ratings yet

- Ca Final Indirect Tax: ABC Analysis (Nov 2020 Exams)Document1 pageCa Final Indirect Tax: ABC Analysis (Nov 2020 Exams)SajidZiaNo ratings yet

- Pradeep Chandelia CV PDFDocument3 pagesPradeep Chandelia CV PDFSajidZiaNo ratings yet

- Basic STD CostingDocument5 pagesBasic STD CostingSajidZiaNo ratings yet

- Supplies - Place of Supplies - Time of SuppliesDocument12 pagesSupplies - Place of Supplies - Time of SuppliesSajidZiaNo ratings yet

- My New Form of CVDocument1 pageMy New Form of CVSajidZiaNo ratings yet

- WorkDocument2 pagesWorkSajidZiaNo ratings yet

- Integrated MCQ'S: Ans: (B)Document4 pagesIntegrated MCQ'S: Ans: (B)SajidZiaNo ratings yet

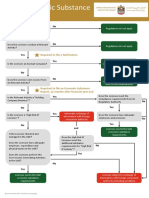

- Flowchart: Required To File A NotificationDocument2 pagesFlowchart: Required To File A NotificationSajidZiaNo ratings yet

- P7 Summary Notes (2017 - 08 - 11 15 - 36 - 51 Utc)Document150 pagesP7 Summary Notes (2017 - 08 - 11 15 - 36 - 51 Utc)SajidZiaNo ratings yet

- F4ENG 2014 Jun ADocument13 pagesF4ENG 2014 Jun ASajidZiaNo ratings yet

- Advanced Financial Management: Tuesday 3 June 2014Document13 pagesAdvanced Financial Management: Tuesday 3 June 2014SajidZiaNo ratings yet

- F8 Chapter 2Document8 pagesF8 Chapter 2SajidZiaNo ratings yet

- AnswersDocument9 pagesAnswersSajidZiaNo ratings yet

- AnswersDocument10 pagesAnswersSajidZiaNo ratings yet

- Audit and Assurance (International) : Thursday 5 June 2014Document6 pagesAudit and Assurance (International) : Thursday 5 June 2014SajidZiaNo ratings yet

- j14 F7int AnsDocument10 pagesj14 F7int AnsSajidZiaNo ratings yet

- SSS BenefitsDocument2 pagesSSS BenefitsALIAHDAYNE POLIDARIONo ratings yet

- DE7Document2 pagesDE7Ronnie Lee MickleNo ratings yet

- Revised Leave RulesDocument22 pagesRevised Leave RulesArshad JehanNo ratings yet

- SssDocument15 pagesSssarianna0624No ratings yet

- PercentDocument24 pagesPercentmidas66No ratings yet

- Japan Pension RefundDocument6 pagesJapan Pension RefundKathleen Catubay SamsonNo ratings yet

- Maven Minds Budget Brief 2022Document24 pagesMaven Minds Budget Brief 2022Salman AhmedNo ratings yet

- Pop SP PDFDocument93 pagesPop SP PDFkkkNo ratings yet

- Income Taxation LectureDocument78 pagesIncome Taxation LectureMa Jodelyn RosinNo ratings yet

- Annuities Business-Math PDFDocument20 pagesAnnuities Business-Math PDFElmer John Patropes100% (1)

- Adzu Tax 01 B Learning Packet 3 Concept of IncomeDocument5 pagesAdzu Tax 01 B Learning Packet 3 Concept of IncomeDanielle JoenNo ratings yet

- Kerala Shops and Commercial Establishment Rules PDFDocument15 pagesKerala Shops and Commercial Establishment Rules PDFarunlal100% (1)

- Module 4 - Income TaxationDocument6 pagesModule 4 - Income TaxationLumbay, Jolly MaeNo ratings yet

- Itr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 371707780280620 Assessment Year: 2020-21Document7 pagesItr-1 Sahaj Indian Income Tax Return: Acknowledgement Number: 371707780280620 Assessment Year: 2020-21Upen PalNo ratings yet

- Edelweiss Tokio Life - Cashflow Protection Plus - : OverviewDocument2 pagesEdelweiss Tokio Life - Cashflow Protection Plus - : OverviewarunNo ratings yet

- TSDBF Answering Affidavit (Signed) 020919-OCRDocument147 pagesTSDBF Answering Affidavit (Signed) 020919-OCRjillianNo ratings yet

- Scan1 PDFDocument3 pagesScan1 PDFAdamolekun OmololaNo ratings yet

- Lok Sabha Unstarred Question No.1794Document7 pagesLok Sabha Unstarred Question No.1794satyamNo ratings yet

- Payroll - Internal Audit Report: City of MarionDocument31 pagesPayroll - Internal Audit Report: City of MarionMudassar NawazNo ratings yet

- Deccan Chronicle Holdings Limited No. 5th Floor, B.M.T.C Commercial Comples, 80ft Road, Koramangala. Benguluru - 560 095Document1 pageDeccan Chronicle Holdings Limited No. 5th Floor, B.M.T.C Commercial Comples, 80ft Road, Koramangala. Benguluru - 560 095David PenNo ratings yet

- TE OutlineDocument113 pagesTE OutlineJavier RosadoNo ratings yet

- Topic 1 Introduction To TaxationDocument28 pagesTopic 1 Introduction To TaxationZebedee Taltal0% (1)

- Form C Corporate Income Tax Return Taxpayer GuideDocument31 pagesForm C Corporate Income Tax Return Taxpayer GuideDanielNo ratings yet

- #13Document43 pages#13itsanyuserNo ratings yet

- Policies of Telangana State in TeluguDocument3 pagesPolicies of Telangana State in TeluguGameloftersupportNo ratings yet

- 35intercontinental Broadcasting Corporation VDocument2 pages35intercontinental Broadcasting Corporation Vcrisanto perezNo ratings yet

- New Detailed Affidavit of Income and Assessts June 2017Document29 pagesNew Detailed Affidavit of Income and Assessts June 2017MohiniChoudharyNo ratings yet