You might also like

- Greek Financial Crisis May 2011Document5 pagesGreek Financial Crisis May 2011Marco Antonio RaviniNo ratings yet

- 2023 07 28 EurozoneUS-GDPDocument14 pages2023 07 28 EurozoneUS-GDPadilfarooqaNo ratings yet

- Extracto Del Informe de La Agencia DBRSDocument2 pagesExtracto Del Informe de La Agencia DBRSdperez3205No ratings yet

- Spain's Financial CrisisDocument15 pagesSpain's Financial CrisisPurnendu SinghNo ratings yet

- Weekly Market Commentary 6-12-2012Document3 pagesWeekly Market Commentary 6-12-2012monarchadvisorygroupNo ratings yet

- Euro Briefing: Crisis Resolution Enters New PhaseDocument24 pagesEuro Briefing: Crisis Resolution Enters New PhaseJavier EscribaNo ratings yet

- Eurozone Forecast Summer2011 GreeceDocument8 pagesEurozone Forecast Summer2011 GreeceBenin Uthup ThomasNo ratings yet

- Fitch Ratings Downgraded Spain's Long Term ForeignDocument14 pagesFitch Ratings Downgraded Spain's Long Term ForeignmelvineNo ratings yet

- Policy Brief: Impact of Italy's Draft Budget On Growth and Fiscal SolvencyDocument19 pagesPolicy Brief: Impact of Italy's Draft Budget On Growth and Fiscal SolvencyAntonio Annicchiarico RenoNo ratings yet

- The Global Debt ProblemDocument3 pagesThe Global Debt Problemrichardck61No ratings yet

- Paper - The Fiscal Crisis in Europe - 01Document9 pagesPaper - The Fiscal Crisis in Europe - 01290105No ratings yet

- Responding to the European Sovereign Debt CrisisDocument25 pagesResponding to the European Sovereign Debt CrisisJJ Amanda ChenNo ratings yet

- Managing and Monitoring Credit Risk After The COVID-19 PandemicDocument12 pagesManaging and Monitoring Credit Risk After The COVID-19 PandemicJabu MpolokengNo ratings yet

- OECD - Turkey - Economic Survey Executive SummaryDocument8 pagesOECD - Turkey - Economic Survey Executive SummaryfineksusgroupNo ratings yet

- PWC Philippines M&A Challenge Preliminary Round: November 06, 2020Document22 pagesPWC Philippines M&A Challenge Preliminary Round: November 06, 2020Mary Anne JamisolaNo ratings yet

- Highlights: Economy and Strategy GroupDocument33 pagesHighlights: Economy and Strategy GroupvladvNo ratings yet

- La Crisis de Deuda en Zona Euro 2011Document10 pagesLa Crisis de Deuda en Zona Euro 2011InformaNo ratings yet

- Global Economic Outlook October-2020Document27 pagesGlobal Economic Outlook October-2020Husain ADNo ratings yet

- 82115595-10 Countries With The Most Debt in The World 21-2-2012 PDFDocument10 pages82115595-10 Countries With The Most Debt in The World 21-2-2012 PDFAthanassiosNo ratings yet

- The Unicredit Economics Chartbook: QuarterlyDocument41 pagesThe Unicredit Economics Chartbook: QuarterlyOrestis VelmachosNo ratings yet

- Commerzbank ForecastDocument16 pagesCommerzbank ForecastgordjuNo ratings yet

- Assessment 2A. International Monetary EconomicsDocument6 pagesAssessment 2A. International Monetary EconomicsBình MinhNo ratings yet

- Open Europe BriefingDocument11 pagesOpen Europe BriefingZerohedgeNo ratings yet

- The European Sovereign Debt Crisis: Philip R. LaneDocument27 pagesThe European Sovereign Debt Crisis: Philip R. LaneatifchaudhryNo ratings yet

- European Debt Crisis Explained: Causes, Countries Involved and SolutionsDocument19 pagesEuropean Debt Crisis Explained: Causes, Countries Involved and SolutionsAmit BhardwajNo ratings yet

- Hellenic Republic WasDocument2 pagesHellenic Republic WasAdriana DhaniyahNo ratings yet

- André Sapir-Why Has COVID-19 Hit Different European Union Economies So DifferentlyDocument13 pagesAndré Sapir-Why Has COVID-19 Hit Different European Union Economies So DifferentlyJast NaufalNo ratings yet

- Coordinated macroeconomic policies needed for global growthDocument7 pagesCoordinated macroeconomic policies needed for global growthddufourtNo ratings yet

- The Effect of Global Crisis Into Euro Region: A Case Study of Greek CrisisDocument6 pagesThe Effect of Global Crisis Into Euro Region: A Case Study of Greek CrisisujjwalenigmaNo ratings yet

- Debt CrisisDocument3 pagesDebt CrisisAshNo ratings yet

- Global Wind Energy Council - GWEC Annual Report 2011Document68 pagesGlobal Wind Energy Council - GWEC Annual Report 2011Ipdmaq Abimaq100% (1)

- Moody's Downgrades Spain's Government Bond Ratings To A1Document4 pagesMoody's Downgrades Spain's Government Bond Ratings To A1MuJQNo ratings yet

- Greece: Financing Risks: Greece Has Run Persistent Twin Deficits (2000-08 Average)Document5 pagesGreece: Financing Risks: Greece Has Run Persistent Twin Deficits (2000-08 Average)Frode HaukenesNo ratings yet

- EIB Investment Report 2023/2024 - Key Findings: Transforming for competitivenessFrom EverandEIB Investment Report 2023/2024 - Key Findings: Transforming for competitivenessNo ratings yet

- Greece Seeks EU-Led SolutionDocument40 pagesGreece Seeks EU-Led SolutionRusMartinNo ratings yet

- Barc Strategy ElementsDocument11 pagesBarc Strategy ElementspdoorNo ratings yet

- Ci17 5Document11 pagesCi17 5robmeijerNo ratings yet

- Greece DsaDocument9 pagesGreece DsaEric WhitfieldNo ratings yet

- Greece Crisis and The Consequences For IndiaDocument4 pagesGreece Crisis and The Consequences For IndiaAditya KharkiaNo ratings yet

- Allianz Trade - Défaillances Prévues Et Hisotrique 2022 - 10 - 20 - Business - Insolvency - AZT - FINALDocument21 pagesAllianz Trade - Défaillances Prévues Et Hisotrique 2022 - 10 - 20 - Business - Insolvency - AZT - FINALredalouziriNo ratings yet

- Mediobanca Securities Report - 17 Giugno 2013 - "Italy Seizing Up - Caution Required" - Di Antonio GuglielmiDocument88 pagesMediobanca Securities Report - 17 Giugno 2013 - "Italy Seizing Up - Caution Required" - Di Antonio GuglielmiEmanuele Sabetta100% (1)

- European Economic Outlook: No Room For Optimism: June2014 1Document2 pagesEuropean Economic Outlook: No Room For Optimism: June2014 1pathanfor786No ratings yet

- Moment - of - Truth - Martn WolfDocument3 pagesMoment - of - Truth - Martn Wolf3bandhuNo ratings yet

- How Did Ireland Melt Down So Quickly?Document3 pagesHow Did Ireland Melt Down So Quickly?Sunil GuptaNo ratings yet

- Greek RestructuringDocument8 pagesGreek RestructuringSeven LoveNo ratings yet

- The Debt Challenge in Europe: HighlightsDocument28 pagesThe Debt Challenge in Europe: HighlightsBruegelNo ratings yet

- IMF Debt Sustainability UpdateDocument4 pagesIMF Debt Sustainability UpdateZerohedgeNo ratings yet

- Is Greece Tip of Iceberg 022210Document7 pagesIs Greece Tip of Iceberg 022210Shahzad DalalNo ratings yet

- MIR August 2021Document15 pagesMIR August 2021Ronakk MoondraNo ratings yet

- Rating Action:: Moody's Downgrades Italy's Government Bond Rating To Baa2 From A3, Maintains Negative OutlookDocument5 pagesRating Action:: Moody's Downgrades Italy's Government Bond Rating To Baa2 From A3, Maintains Negative OutlookmichelerovattiNo ratings yet

- Italian Risks To The EurozoneDocument12 pagesItalian Risks To The EurozoneSuparna BhattacharyaNo ratings yet

- Monthly: La Reforma Del Sector Servicios OUTLOOK 2012Document76 pagesMonthly: La Reforma Del Sector Servicios OUTLOOK 2012Anonymous OY8hR2NNo ratings yet

- The Greek Economy & Its Stability Programme: Written byDocument44 pagesThe Greek Economy & Its Stability Programme: Written bypapaki2No ratings yet

- BNP Paribas The Financial Crisis and Household Savings Behaviour in France 11102010Document12 pagesBNP Paribas The Financial Crisis and Household Savings Behaviour in France 11102010YUGANDHAR016577No ratings yet

- Sov Debt CrisisDocument9 pagesSov Debt CrisisAzra Hanić SućeskaNo ratings yet

- Portugal & The Eurozone Crises Project By: Akash Saxena Gaurav Mohan Aditya ChaudharyDocument15 pagesPortugal & The Eurozone Crises Project By: Akash Saxena Gaurav Mohan Aditya ChaudharyAkash SaxenaNo ratings yet

- CIBC Faded Euphoria 11-1-11Document3 pagesCIBC Faded Euphoria 11-1-11Penna111No ratings yet

- Spain's Economic Growth Rebounds but Inflation RisesDocument15 pagesSpain's Economic Growth Rebounds but Inflation RisesJaime SánchezNo ratings yet

- 2020 External Debt Sustainability and DevelopmentDocument22 pages2020 External Debt Sustainability and DevelopmentjamelNo ratings yet

- Investment Report 2022/2023 - Key Findings: Resilience and renewal in EuropeFrom EverandInvestment Report 2022/2023 - Key Findings: Resilience and renewal in EuropeNo ratings yet

- Manafort Ny IndictmentDocument11 pagesManafort Ny IndictmentZerohedge Janitor100% (1)

- The $10 Trillion Rescue: How Governments Can Deliver ImpactDocument13 pagesThe $10 Trillion Rescue: How Governments Can Deliver ImpactAasrith KandulaNo ratings yet

- Doug Smith - Digital Signal Processing Technology - Essentials of The Communications Revolution-American Radio Relay League (ARRL) (2001)Document231 pagesDoug Smith - Digital Signal Processing Technology - Essentials of The Communications Revolution-American Radio Relay League (ARRL) (2001)Gonzalo Hernán Barría PérezNo ratings yet

- Theory and Practice of GVAR Modeling: Federal Reserve Bank of Dallas Globalization and Monetary Policy InstituteDocument55 pagesTheory and Practice of GVAR Modeling: Federal Reserve Bank of Dallas Globalization and Monetary Policy InstituteSaadBourouisNo ratings yet

- Firms' Size and China's Industrial Water Pollution: Replication InstructionsDocument10 pagesFirms' Size and China's Industrial Water Pollution: Replication InstructionsGonzalo Hernán Barría PérezNo ratings yet

- (The R Series) Yihui Xie, Joseph J. Allaire, Garrett Grolemund-R Markdown - The Definitive Guide (Conversion) - CRC Press (2019)Document189 pages(The R Series) Yihui Xie, Joseph J. Allaire, Garrett Grolemund-R Markdown - The Definitive Guide (Conversion) - CRC Press (2019)Gonzalo Hernán Barría PérezNo ratings yet

- Introduction to Data Science Course SyllabusDocument9 pagesIntroduction to Data Science Course SyllabusGonzalo Hernán Barría PérezNo ratings yet

- Fallo Movilh PastorDocument501 pagesFallo Movilh PastorGonzalo Hernán Barría PérezNo ratings yet

- SSRNDocument41 pagesSSRNGonzalo Hernán Barría PérezNo ratings yet

- Bahamonde Social Sciences Epistemology UGRAD SyllabusDocument13 pagesBahamonde Social Sciences Epistemology UGRAD SyllabusGonzalo Hernán Barría PérezNo ratings yet

- LSavati Regression AnalysisDocument25 pagesLSavati Regression AnalysisGonzalo Hernán Barría PérezNo ratings yet

- 978 3 319 57475 2Document364 pages978 3 319 57475 2Gonzalo Hernán Barría PérezNo ratings yet

- Econometrics I Course SyllabusDocument3 pagesEconometrics I Course SyllabusGonzalo Hernán Barría PérezNo ratings yet

- 2004 Introduction To Symposium Two Paths To A Science of PoliticsDocument7 pages2004 Introduction To Symposium Two Paths To A Science of PoliticsGonzalo Hernán Barría PérezNo ratings yet

- International Review For The Sociology of Sport Volume Issue 2016 (Doi 10.1177/1012690216656807) Bradbury, S. Van Sterkenburg, J. Mignon, P. - The Under-Representation and Experiences of Elite LeDocument22 pagesInternational Review For The Sociology of Sport Volume Issue 2016 (Doi 10.1177/1012690216656807) Bradbury, S. Van Sterkenburg, J. Mignon, P. - The Under-Representation and Experiences of Elite LeGonzalo Hernán Barría PérezNo ratings yet

- Why Friendly A IDocument8 pagesWhy Friendly A IGonzalo Hernán Barría PérezNo ratings yet

- BLK Sponsor ReleaseDocument5 pagesBLK Sponsor ReleaseGonzalo Hernán Barría PérezNo ratings yet

- LOCKER STORAGEDocument2 pagesLOCKER STORAGEGonzalo Hernán Barría PérezNo ratings yet

- 978 981 10 6620 7Document742 pages978 981 10 6620 7Gonzalo Hernán Barría Pérez100% (1)

- Convergence of The Self-Dual Ginzburg-Landau Gradient Flow: 1 Introduction and Statement of ResultsDocument15 pagesConvergence of The Self-Dual Ginzburg-Landau Gradient Flow: 1 Introduction and Statement of ResultsGonzalo Hernán Barría PérezNo ratings yet

- Control3 SolucinDocument2 pagesControl3 SolucinGonzalo Hernán Barría PérezNo ratings yet

- CurrentDocument15 pagesCurrentGonzalo Hernán Barría PérezNo ratings yet

- Business EnvironmentDocument115 pagesBusiness EnvironmentTarusengaNo ratings yet

- Curriculum Financing in Basic School Education in NigeriaDocument9 pagesCurriculum Financing in Basic School Education in NigeriaAcademic JournalNo ratings yet

- Dissertation On Debt Securities Market in IndiaDocument103 pagesDissertation On Debt Securities Market in Indiaumesh kumar sahu0% (2)

- Domestic bond markets in Latin America: achievements and challengesDocument14 pagesDomestic bond markets in Latin America: achievements and challengesThomas RobertsNo ratings yet

- Adaptive Market Hypothesis Evidence From Indian Bond MarketDocument14 pagesAdaptive Market Hypothesis Evidence From Indian Bond MarketsaravanakrisNo ratings yet

- Anukret On Tax Incentive in Securities Sector EnglishDocument4 pagesAnukret On Tax Incentive in Securities Sector EnglishChou ChantraNo ratings yet

- Foreign Currency Denominated DebtDocument16 pagesForeign Currency Denominated DebtAfaq AhmadNo ratings yet

- African Economic Outlook 2021Document180 pagesAfrican Economic Outlook 2021CNBC AfricaNo ratings yet

- R56 Fundamentals of Credit AnalysisDocument23 pagesR56 Fundamentals of Credit AnalysisDiegoNo ratings yet

- Practice Macro Economics Multiple Choice QuestionsDocument8 pagesPractice Macro Economics Multiple Choice QuestionsmarjankasiNo ratings yet

- Forex Factory 1Document9 pagesForex Factory 1Idon WahidinNo ratings yet

- © The Institute of Chartered Accountants of IndiaDocument9 pages© The Institute of Chartered Accountants of IndiaIBBF FitnessNo ratings yet

- Janney Fixed Income StrategyDocument7 pagesJanney Fixed Income StrategyJohn CortapassoNo ratings yet

- A Theory of Debt OverhangDocument16 pagesA Theory of Debt Overhangprince marcNo ratings yet

- Eco Sem6Document8 pagesEco Sem6smarttalksaurabhNo ratings yet

- Public Sector Risk Management BagamoyoDocument38 pagesPublic Sector Risk Management BagamoyosakoauditorNo ratings yet

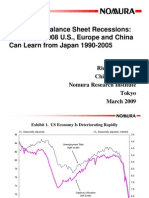

- Richard Koo PresentationDocument34 pagesRichard Koo Presentationpkedrosky100% (14)

- Foreign Direct Investment and Cross Border Acquisitions Eun8e CH 016 PPT MXQJDocument37 pagesForeign Direct Investment and Cross Border Acquisitions Eun8e CH 016 PPT MXQJXuan LyNo ratings yet

- Financial Markets ModuleDocument248 pagesFinancial Markets ModuleTrường Nguyễn100% (2)

- Important Meetings Today: Morning ReportDocument3 pagesImportant Meetings Today: Morning Reportnaudaslietas_lvNo ratings yet

- African Economic Outlook Aeo 2023Document238 pagesAfrican Economic Outlook Aeo 2023Lmv 2022No ratings yet

- Great Red Dragon Short VersionDocument88 pagesGreat Red Dragon Short VersionChristTriumphetNo ratings yet

- Wpcif 082003Document32 pagesWpcif 082003n_paganiNo ratings yet

- Sip Project Report 1701145Document66 pagesSip Project Report 1701145sai prasadNo ratings yet

- Public Finance (Sharbani)Document5 pagesPublic Finance (Sharbani)Sumitava PaulNo ratings yet

- Central Banking and Monetary Policy CourseDocument16 pagesCentral Banking and Monetary Policy CourseNahidul Islam IUNo ratings yet

- PetrozuataDocument13 pagesPetrozuataMikhail TitkovNo ratings yet

- L06 (1) - IMF's Vulnerability Exercise For Emerging Economies (VEE)Document48 pagesL06 (1) - IMF's Vulnerability Exercise For Emerging Economies (VEE)Dekon MakroNo ratings yet

- Central BankingDocument43 pagesCentral BankingOche TjNo ratings yet