0% found this document useful (0 votes)

721 views3 pagesCash Flow: Assumptions

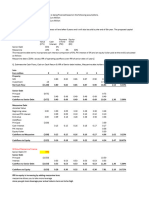

The document presents a discounted cash flow model to value a company. It lists assumptions for tax rate, discount rate, perpetual growth rate, and EV/EBITDA multiple. It then shows projected cash flows, capital expenditures, and net working capital changes over five years. It discounts these cash flows using the WACC to calculate an intrinsic equity value per share of $33.63, higher than the current market price of $25.

Uploaded by

GolamMostafaCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as XLSX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

721 views3 pagesCash Flow: Assumptions

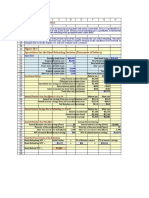

The document presents a discounted cash flow model to value a company. It lists assumptions for tax rate, discount rate, perpetual growth rate, and EV/EBITDA multiple. It then shows projected cash flows, capital expenditures, and net working capital changes over five years. It discounts these cash flows using the WACC to calculate an intrinsic equity value per share of $33.63, higher than the current market price of $25.

Uploaded by

GolamMostafaCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as XLSX, PDF, TXT or read online on Scribd

/ 3