You might also like

- Income TAX: Prof. Jeanefer Reyes CPA, MPADocument37 pagesIncome TAX: Prof. Jeanefer Reyes CPA, MPAmark anthony espiritu75% (4)

- Special Topics in Income TaxationDocument78 pagesSpecial Topics in Income TaxationPantas DiwaNo ratings yet

- Value Added TaxDocument5 pagesValue Added TaxRaven Vargas DayritNo ratings yet

- Real Property: Prof. Jeanefer Reyes Cpa. MpaDocument9 pagesReal Property: Prof. Jeanefer Reyes Cpa. Mpamark anthony espirituNo ratings yet

- Consumption Tax On Sales (Percentage Tax)Document32 pagesConsumption Tax On Sales (Percentage Tax)Alicia Feliciano100% (1)

- 3 Floor, Business & Engineering Building, Matina, Davao City Telefax: (082) 300-1496 Phone No.: (082) 244-34-00 Local 137Document13 pages3 Floor, Business & Engineering Building, Matina, Davao City Telefax: (082) 300-1496 Phone No.: (082) 244-34-00 Local 137Abigail Ann PasiliaoNo ratings yet

- Report of Law1 - Other Percentage TaxDocument16 pagesReport of Law1 - Other Percentage TaxJonalyn Maraña-ManuelNo ratings yet

- Percentage TaxDocument21 pagesPercentage TaxCarla Zante0% (1)

- TAX Major Quiz 1 Answer KeyDocument9 pagesTAX Major Quiz 1 Answer KeyTeresaNo ratings yet

- Corporation Quiz PDFDocument8 pagesCorporation Quiz PDFangelo vasquezNo ratings yet

- Chapter 13 Mixed Business TransactionsDocument10 pagesChapter 13 Mixed Business TransactionsGeraldNo ratings yet

- Value Added Tax Quiz ReviewerDocument2 pagesValue Added Tax Quiz ReviewerLouiseNo ratings yet

- M3 Excise Tax Students Copy Revised PDFDocument73 pagesM3 Excise Tax Students Copy Revised PDFTokis SabaNo ratings yet

- Final Income TaxationDocument4 pagesFinal Income TaxationJean Diane Jovelo100% (1)

- Estate Tax Activities (Questions)Document4 pagesEstate Tax Activities (Questions)Christine Nathalie BalmesNo ratings yet

- Tax MockboardDocument8 pagesTax MockboardJaneNo ratings yet

- Chapter 01 Introduction To Internal Revenue TaxesDocument12 pagesChapter 01 Introduction To Internal Revenue TaxesNikki BucatcatNo ratings yet

- IntAcc 3 Non-Financial LiabilitiesDocument10 pagesIntAcc 3 Non-Financial LiabilitiesKim EllaNo ratings yet

- M5 - Deductions From Gross Estate - Students'Document33 pagesM5 - Deductions From Gross Estate - Students'micaella pasionNo ratings yet

- Tax Lecture Estate Tax Part 2Document7 pagesTax Lecture Estate Tax Part 2Kathreen Aya ExcondeNo ratings yet

- Chapter 10 - Concepts of Vat 7thDocument11 pagesChapter 10 - Concepts of Vat 7thEl Yang100% (3)

- TX12 - Estate TaxDocument14 pagesTX12 - Estate TaxPatrick Kyle AgraviadorNo ratings yet

- Evaluate 1 - Estate Taxation Answer KeyDocument3 pagesEvaluate 1 - Estate Taxation Answer KeyNicolas AlonsoNo ratings yet

- Departmental Finals Answer Key PDFDocument4 pagesDepartmental Finals Answer Key PDFJacob AcostaNo ratings yet

- 04.1 S4 VAT PPT AquinoDocument112 pages04.1 S4 VAT PPT Aquinosaeloun hrdNo ratings yet

- VatDocument16 pagesVatCPA100% (1)

- Income Taxation Finals Quiz 2Document7 pagesIncome Taxation Finals Quiz 2Jericho DupayaNo ratings yet

- Gross IncomeDocument68 pagesGross IncomeNour Aira NaoNo ratings yet

- Accounting Review: TaxationDocument3 pagesAccounting Review: TaxationPatriciaNo ratings yet

- Preferential TaxationDocument8 pagesPreferential TaxationAngelica Nicole TamayoNo ratings yet

- University of Perpetual Help System DaltaDocument9 pagesUniversity of Perpetual Help System DaltaJeanette LampitocNo ratings yet

- Gross Estate ReviewerDocument9 pagesGross Estate ReviewerMark Noel SanteNo ratings yet

- Estate Taxation TestbankDocument54 pagesEstate Taxation TestbankAlly Capacio100% (1)

- MCL - TAX.106 - Income Taxation of Individuals CorporationsDocument58 pagesMCL - TAX.106 - Income Taxation of Individuals CorporationsKim TividadNo ratings yet

- TAX.02 Exercises On Individual TaxationDocument5 pagesTAX.02 Exercises On Individual Taxationleon gumboc100% (1)

- Tax 2Document6 pagesTax 2Zerjo CantalejoNo ratings yet

- Exempt Sale of Goods Properties and Services NotesDocument2 pagesExempt Sale of Goods Properties and Services NotesSelene DimlaNo ratings yet

- Basic Terminologies Basic Terminologies: Estate Tax Estate TaxDocument52 pagesBasic Terminologies Basic Terminologies: Estate Tax Estate TaxFrances Marella CristobalNo ratings yet

- TX 201 PDFDocument5 pagesTX 201 PDFFriedeagle OilNo ratings yet

- Vat OptDocument24 pagesVat OptCharity Venus100% (1)

- Gross Estate Tax QuizzerDocument6 pagesGross Estate Tax QuizzerLloyd Sonica100% (1)

- Notes in Preferential TaxationDocument57 pagesNotes in Preferential TaxationJeremae Ann Ceriaco100% (1)

- TBT CH1Document10 pagesTBT CH1darkNo ratings yet

- Development of Financial Reporting Framework, Standard-Setting Bodies and Regulation of The Accountancy ProfessionDocument3 pagesDevelopment of Financial Reporting Framework, Standard-Setting Bodies and Regulation of The Accountancy ProfessionJUST KINGNo ratings yet

- Theory of Accounts On Business CombinationDocument2 pagesTheory of Accounts On Business CombinationheyNo ratings yet

- Chapter 9 Part 1 Input VatDocument25 pagesChapter 9 Part 1 Input VatChristian PelimcoNo ratings yet

- Au Business Tax Final ExamDocument7 pagesAu Business Tax Final ExamKeira TanNo ratings yet

- Module 2 - Bases Conversion and Development ActDocument14 pagesModule 2 - Bases Conversion and Development ActIm NayeonNo ratings yet

- Deductions From Gross Estate: Business and Transfer Taxation 6Th Edition (By: Valencia & Roxas) Suggested AnswersDocument9 pagesDeductions From Gross Estate: Business and Transfer Taxation 6Th Edition (By: Valencia & Roxas) Suggested AnswersGhatz CondaNo ratings yet

- VAT On Sale of Goods and PropertiesDocument55 pagesVAT On Sale of Goods and PropertiesKarlo PalerNo ratings yet

- Chapter 10 v2Document15 pagesChapter 10 v2Sheilamae Sernadilla Gregorio0% (1)

- Introduction of Income TaxDocument29 pagesIntroduction of Income TaxKathlyn PostreNo ratings yet

- Exercise DrillDocument6 pagesExercise DrillAbigail Ann PasiliaoNo ratings yet

- Introduction To Business TaxationDocument41 pagesIntroduction To Business TaxationJeane Mae Boo0% (1)

- Quiz On VAT154623Document5 pagesQuiz On VAT154623Sandy100% (1)

- R.A. 10963 (TRAIN) - Income Tax ProvisionsDocument50 pagesR.A. 10963 (TRAIN) - Income Tax ProvisionsKrishtineRapisoraBolivarNo ratings yet

- Revised Tax QuestionsDocument25 pagesRevised Tax QuestionssophiaNo ratings yet

- Excise Tax WowoweeDocument18 pagesExcise Tax WowoweeAmado Vallejo IIINo ratings yet

- Aud Prob Part 1Document106 pagesAud Prob Part 1Ma. Hazel Donita DiazNo ratings yet

- Gains or Losses in Dealings in PropertyDocument6 pagesGains or Losses in Dealings in PropertyRussel RuizNo ratings yet

- Business Tax SummaryDocument10 pagesBusiness Tax SummaryJohn Raymond MarzanNo ratings yet

- Briefing On Republic Act (RA) 10963: Tax Reform For Acceleration and Inclusion (TRAIN)Document32 pagesBriefing On Republic Act (RA) 10963: Tax Reform For Acceleration and Inclusion (TRAIN)mark anthony espirituNo ratings yet

- Briefing On Republic Act (RA) 10963: Tax Reform For Acceleration and Inclusion (TRAIN)Document10 pagesBriefing On Republic Act (RA) 10963: Tax Reform For Acceleration and Inclusion (TRAIN)mark anthony espirituNo ratings yet

- Revenue Regulation 21-2018: Prof. Jeanefer ReyesDocument5 pagesRevenue Regulation 21-2018: Prof. Jeanefer Reyesmark anthony espirituNo ratings yet

- Briefing On RA 10963: Tax Reform For Acceleration and Inclusion (TRAIN)Document14 pagesBriefing On RA 10963: Tax Reform For Acceleration and Inclusion (TRAIN)mark anthony espirituNo ratings yet

- Variance AnalysisDocument21 pagesVariance Analysismark anthony espiritu0% (1)

- MS HandOut 02Document1 pageMS HandOut 02mark anthony espirituNo ratings yet

- Quantitative Analysis, and Decision Sciences) Is Part of The Fundamental Curriculum of Most Programs in BusinessDocument3 pagesQuantitative Analysis, and Decision Sciences) Is Part of The Fundamental Curriculum of Most Programs in Businessmark anthony espirituNo ratings yet

- Demand Pre - Intimation LetterDocument2 pagesDemand Pre - Intimation LetterAMIT TIWARINo ratings yet

- En Banc: Republic of The Philippines Quezon CityDocument19 pagesEn Banc: Republic of The Philippines Quezon CityJonas CruzNo ratings yet

- PF PFi Terms and ConditionsDocument20 pagesPF PFi Terms and ConditionsAzeizulNo ratings yet

- Standard Charted - SaadiqDocument16 pagesStandard Charted - SaadiqkirshanlalNo ratings yet

- Tender BaseDocument45 pagesTender BasevirtechNo ratings yet

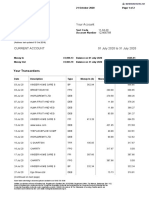

- Current Account 01 July 2020 To 31 July 2020: Your TransactionsDocument2 pagesCurrent Account 01 July 2020 To 31 July 2020: Your TransactionssadNo ratings yet

- E PaymentDocument22 pagesE PaymentxanshahNo ratings yet

- Payment Schedule: Buyer: Buyer Request Code: StatusDocument8 pagesPayment Schedule: Buyer: Buyer Request Code: Statusbrian9211No ratings yet

- ChapterizationDocument133 pagesChapterizationPRERANA MISHRANo ratings yet

- VAT GuideZRADocument56 pagesVAT GuideZRADaniel Glen-WilliamsonNo ratings yet

- Taxation Case Digest 1Document14 pagesTaxation Case Digest 1Jong Perraren100% (1)

- Integrating With HCM PDFDocument572 pagesIntegrating With HCM PDFFerasHamdanNo ratings yet

- PMA Dated October 11, 2022 - Clay ArfaDocument12 pagesPMA Dated October 11, 2022 - Clay ArfaEmir ArfaNo ratings yet

- IELTS Application Form Terms & ConditionsDocument12 pagesIELTS Application Form Terms & Conditionsrv nidinNo ratings yet

- Chegg QA Guideline - v10Document34 pagesChegg QA Guideline - v10Buha BuhaNo ratings yet

- General Terms and Conditions of Delivery and Payment: 1. Conclusion of The ContractDocument3 pagesGeneral Terms and Conditions of Delivery and Payment: 1. Conclusion of The ContractMociran ClaudiuNo ratings yet

- Difficulty of Care PaymentsDocument4 pagesDifficulty of Care PaymentsKevin KellyNo ratings yet

- Transactions 650 344366000 20200827 200640 PDFDocument15 pagesTransactions 650 344366000 20200827 200640 PDFKiran AdhikariNo ratings yet

- Export/Import Procedures: Md. Sarwar Hossain Deputy General Manager Bangladesh BankDocument12 pagesExport/Import Procedures: Md. Sarwar Hossain Deputy General Manager Bangladesh BankAlam (MDO)No ratings yet

- Device Payment T C 122016Document4 pagesDevice Payment T C 122016Amy Steele100% (1)

- General Banking Activities of Sonali BanDocument56 pagesGeneral Banking Activities of Sonali BanKazi Abu SayeedNo ratings yet

- Tamilnad Mercantile Bank LimitedDocument60 pagesTamilnad Mercantile Bank LimitedRinkesh Agarwal100% (1)

- GST Good Sex Tonight: Input CreditDocument23 pagesGST Good Sex Tonight: Input CreditaltmashNo ratings yet

- Service Manual enDocument40 pagesService Manual enkhaled nawazNo ratings yet

- GRC RulesetDocument6 pagesGRC RulesetDAVIDNo ratings yet

- Document 1: Why Sweden Is Close To Becoming A Cashless EconomyDocument4 pagesDocument 1: Why Sweden Is Close To Becoming A Cashless EconomyfatimaNo ratings yet

- E-Commerce: Digital Markets, Digital Goods: © 2010 by PearsonDocument33 pagesE-Commerce: Digital Markets, Digital Goods: © 2010 by PearsonPatrickNo ratings yet

- Multiple Award Schedule: Angus-Hamer IncDocument14 pagesMultiple Award Schedule: Angus-Hamer IncBriana BaptisteNo ratings yet

- Tibajia, Jr. vs. Court of Appeals, 223 SCRA 163, June 04, 1993Document5 pagesTibajia, Jr. vs. Court of Appeals, 223 SCRA 163, June 04, 1993RenNo ratings yet

- Avs Fencing Catalogue 2011Document44 pagesAvs Fencing Catalogue 2011AVSFencingNo ratings yet