You might also like

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- Report BCBLDocument98 pagesReport BCBLTanvir Ahamed100% (1)

- An Internship Report On General Banking Operation of EXIM Bank LimitedDocument64 pagesAn Internship Report On General Banking Operation of EXIM Bank LimitedNafiz FahimNo ratings yet

- Internship Report On Foreign Exchange Operation of Jamuna Bank LimitedDocument154 pagesInternship Report On Foreign Exchange Operation of Jamuna Bank LimitedAtikul Arif0% (1)

- Credit Management of Sonali Bank Limited27 6Document49 pagesCredit Management of Sonali Bank Limited27 6Md Alamgir KabirNo ratings yet

- Foreign Exchange of Janata BankDocument35 pagesForeign Exchange of Janata BankNolaNo ratings yet

- Financial Inclusion Study on Rocket Mobile BankingDocument56 pagesFinancial Inclusion Study on Rocket Mobile BankingTanjin UrmiNo ratings yet

- Internship Report On General Banking Operation of EXIM Bank LimitedDocument39 pagesInternship Report On General Banking Operation of EXIM Bank LimitedJohnathan Rice50% (2)

- Credit Risk Management For EXIM Bank FinalDocument69 pagesCredit Risk Management For EXIM Bank Finalkhansha ComputersNo ratings yet

- Agrani BankDocument28 pagesAgrani BankSh1r1nNo ratings yet

- Internship ReportDocument54 pagesInternship ReportZubayer HossainNo ratings yet

- Loan & Advances of IFIC Bank LimitedDocument28 pagesLoan & Advances of IFIC Bank LimitedAbubakkar SiddiqueNo ratings yet

- Credit Risk Management of National Bank Ltd.Document51 pagesCredit Risk Management of National Bank Ltd.Mou Tushi100% (1)

- Understanding General Banking Functions of Agrani BankDocument41 pagesUnderstanding General Banking Functions of Agrani BankArefeen HridoyNo ratings yet

- Credit Risk Management of NBL1Document119 pagesCredit Risk Management of NBL1Mir FaiazNo ratings yet

- Comparative Analysis Between Islami Bank Bangladesh Limited and Jamuna Bank Limite1Document42 pagesComparative Analysis Between Islami Bank Bangladesh Limited and Jamuna Bank Limite1Tahsin Monabil0% (1)

- Customer Satisfaction of bKash LimitedDocument49 pagesCustomer Satisfaction of bKash Limitedjackson100% (1)

- Intern Report On Bank AsiaDocument89 pagesIntern Report On Bank Asiaziko777No ratings yet

- SJIBL Internship ReportDocument101 pagesSJIBL Internship ReportsaminbdNo ratings yet

- Credit Management of Mercantile Bank LimitedDocument61 pagesCredit Management of Mercantile Bank LimitedMoyan Hossain100% (1)

- Foreign Exchange of Jamuna Bank Ltd.Document56 pagesForeign Exchange of Jamuna Bank Ltd.arifNo ratings yet

- Foreign Exchange Operation of Commercial BankDocument24 pagesForeign Exchange Operation of Commercial BankShawon100% (1)

- Banking Report: NCC Bank InternshipDocument62 pagesBanking Report: NCC Bank InternshipJahangir AlamNo ratings yet

- JBL Full - S. M. Abdul MukitDocument50 pagesJBL Full - S. M. Abdul MukithabibNo ratings yet

- Investment Mechanism of Islami Bank BangladeshDocument67 pagesInvestment Mechanism of Islami Bank BangladeshImranAhamedShakhor50% (2)

- Internship Report at UCBL: A Comprehensive OverviewDocument46 pagesInternship Report at UCBL: A Comprehensive Overviewsourov shahaNo ratings yet

- Marketing Activities of Grameen BankDocument35 pagesMarketing Activities of Grameen BankHarunur Rashid100% (1)

- Project Report ON: Foreign Exchange Operation: A Study On Social Islami Bank Limited Submitted ToDocument55 pagesProject Report ON: Foreign Exchange Operation: A Study On Social Islami Bank Limited Submitted ToJannatul FerdousNo ratings yet

- Foreign Exchange On First Security Islami Bank LTDDocument60 pagesForeign Exchange On First Security Islami Bank LTDAhadul Islam100% (2)

- Internship Report (Sakibul Alam)Document36 pagesInternship Report (Sakibul Alam)Mohammad MamunNo ratings yet

- Investment Analysis of Jamuna Bank Ltd.Document53 pagesInvestment Analysis of Jamuna Bank Ltd.SharifMahmud50% (6)

- Historical Background of IBBLDocument5 pagesHistorical Background of IBBLSISkobirNo ratings yet

- Analysis of Investment Procedure and Performance of Al-Arafah Islami Bank Limited (AIBL)Document47 pagesAnalysis of Investment Procedure and Performance of Al-Arafah Islami Bank Limited (AIBL)MohammadSajjadHossain100% (1)

- Exim BankDocument48 pagesExim BankAnonymous w7zJFTwqiQNo ratings yet

- 1.1 Background: " A Study On SME Banking Practices in Janata Bank Limited"Document56 pages1.1 Background: " A Study On SME Banking Practices in Janata Bank Limited"Tareq AlamNo ratings yet

- Digital Marketing ActivitiesDocument52 pagesDigital Marketing ActivitiesMehedi HasanNo ratings yet

- Mission of IBBLDocument19 pagesMission of IBBLTayyaba AkramNo ratings yet

- Internship Report On Jamuna Bank Ltd.Document92 pagesInternship Report On Jamuna Bank Ltd.Shaker Sazzad100% (1)

- Financial Analysis of EBLDocument49 pagesFinancial Analysis of EBLAbu TaherNo ratings yet

- Jamuna BankDocument88 pagesJamuna BankMasood PervezNo ratings yet

- Internship - HRM Practice in Dhaka BANK Limited"Document58 pagesInternship - HRM Practice in Dhaka BANK Limited"Rasel SarderNo ratings yet

- The City Bank Ltd.Document34 pagesThe City Bank Ltd.Shamsuddin AhmedNo ratings yet

- Internship Report On Loan and AdvanceDocument72 pagesInternship Report On Loan and AdvanceAsad KhanNo ratings yet

- Internship Report On General Banking Activities of Basic BankDocument55 pagesInternship Report On General Banking Activities of Basic BankAfroza KhanomNo ratings yet

- A Project Report On: Customer Preference & Attributes Towards Saving-AccountDocument68 pagesA Project Report On: Customer Preference & Attributes Towards Saving-AccountchinunanaNo ratings yet

- Banking Sector Report of Azad Jammu & KashmirDocument61 pagesBanking Sector Report of Azad Jammu & Kashmirsamreen kNo ratings yet

- Submitted To:: "The Scenario of Non-Performing Loans in Bangladesh: Causes, Pitfalls and Remedies"Document26 pagesSubmitted To:: "The Scenario of Non-Performing Loans in Bangladesh: Causes, Pitfalls and Remedies"Siddharth ShrivastavNo ratings yet

- Internship Report OnDocument52 pagesInternship Report OnFarjana RahmanNo ratings yet

- Financial Performance Analysis of Banking Sector in Bangladesh - A Case Study On Selected Commercial BanksDocument70 pagesFinancial Performance Analysis of Banking Sector in Bangladesh - A Case Study On Selected Commercial BanksAshaduzzamanNo ratings yet

- Internship Report On General Banking of Janata Bank LimitedDocument35 pagesInternship Report On General Banking of Janata Bank LimitedMd. Tareq AzizNo ratings yet

- Ibbl Investment Portfolio ofDocument47 pagesIbbl Investment Portfolio ofঘুমন্ত বালক100% (2)

- Agrani Bank Internship ReportDocument71 pagesAgrani Bank Internship ReportRobiRashedNo ratings yet

- Internship Report of IFIC BankDocument40 pagesInternship Report of IFIC BankJāfri WāhidNo ratings yet

- Foreign Exchange Policy of EXIM Bank BangladeshDocument76 pagesForeign Exchange Policy of EXIM Bank BangladeshMd MostakNo ratings yet

- ADC PresentationDocument16 pagesADC PresentationNusha TabassumNo ratings yet

- A Study On Bank of Maharashtra: Commercial Banking SystemDocument13 pagesA Study On Bank of Maharashtra: Commercial Banking SystemGovind N VNo ratings yet

- Internship ReportDocument42 pagesInternship ReportBoby PodderNo ratings yet

- EBL internship report on HRM practicesDocument54 pagesEBL internship report on HRM practicesHossan SabbirNo ratings yet

- General Banking Practices of Southeast BankDocument74 pagesGeneral Banking Practices of Southeast BankTamim SikderNo ratings yet

- An Internship Report on General Banking of Southeast Bank LimitedDocument64 pagesAn Internship Report on General Banking of Southeast Bank LimitedAnnex BUBTNo ratings yet

- General Banking Activities of Standard Bank Ltd.Document40 pagesGeneral Banking Activities of Standard Bank Ltd.Moyan HossainNo ratings yet

- General Banking of EXPORT IMPORT BANK OF BANGLADESH LIMITED (EXIM BANK)Document45 pagesGeneral Banking of EXPORT IMPORT BANK OF BANGLADESH LIMITED (EXIM BANK)Moyan HossainNo ratings yet

- Foreign Exchange Function of UBLDocument31 pagesForeign Exchange Function of UBLMoyan HossainNo ratings yet

- Credit Management of Mercantile Bank LimitedDocument61 pagesCredit Management of Mercantile Bank LimitedMoyan Hossain100% (1)

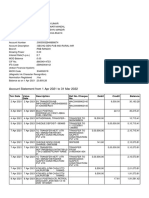

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument1 pageStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceLuckyNo ratings yet

- The Housing Industrial ComplexDocument12 pagesThe Housing Industrial ComplexNational Press FoundationNo ratings yet

- Department of Psychology Cordially Invites You For The: Holy Cross College (Autonomous)Document1 pageDepartment of Psychology Cordially Invites You For The: Holy Cross College (Autonomous)aayisha banuNo ratings yet

- Account StatementDocument46 pagesAccount Statementogagz ogagzNo ratings yet

- Citi Statement Jan 2023Document5 pagesCiti Statement Jan 2023Neeraj_Kumar_Agrawal80% (5)

- Kabboudi: Problem NotesDocument7 pagesKabboudi: Problem NotesamanittaNo ratings yet

- Sree Narayana Guru College Banking ProjectDocument53 pagesSree Narayana Guru College Banking ProjectSathvik ReddyNo ratings yet

- How To Measure Bank SizeDocument24 pagesHow To Measure Bank SizeAsniNo ratings yet

- Sales Presentation - BankingDocument18 pagesSales Presentation - BankingdrifterliverNo ratings yet

- Uco Bank: Head Office: Kolkata-700 001Document3 pagesUco Bank: Head Office: Kolkata-700 001itsmeadiNo ratings yet

- "Banking Regulation Act 1969": Shreeraj HariharanDocument71 pages"Banking Regulation Act 1969": Shreeraj HariharanVi JayNo ratings yet

- Development Financial InstitutionsDocument9 pagesDevelopment Financial Institutionsapi-3739522No ratings yet

- Electronic Payment MediaDocument31 pagesElectronic Payment MediaAnubha100% (1)

- OpTransactionHistory (2017 Dec - 2018 Dec)Document22 pagesOpTransactionHistory (2017 Dec - 2018 Dec)Lakshmi Narayana SindiriNo ratings yet

- 2023-DOA Buy&Sell BG-SBLC CreditDocument18 pages2023-DOA Buy&Sell BG-SBLC CreditLouis Y100% (2)

- Account Statement From 1 Apr 2021 To 31 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument14 pagesAccount Statement From 1 Apr 2021 To 31 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRishav AnandNo ratings yet

- General Banking Law of 2000Document13 pagesGeneral Banking Law of 2000JyNo ratings yet

- Vietnam Money Market Gr1Document18 pagesVietnam Money Market Gr1Kiềuu AnnhNo ratings yet

- Bms (BANKING MANAGEMENT SYSTEM)Document25 pagesBms (BANKING MANAGEMENT SYSTEM)Nidhish raj mouryaNo ratings yet

- "Study On Loan and Credit Facility at SDCC Bank, Rourkela ": Summer Internship Project Report OnDocument81 pages"Study On Loan and Credit Facility at SDCC Bank, Rourkela ": Summer Internship Project Report OnASIT EKKANo ratings yet

- S4 BAFS 1st Term Test 2020-2021 Q PaperDocument5 pagesS4 BAFS 1st Term Test 2020-2021 Q PaperjjjjjjjjjjjjjjjjjjNo ratings yet

- Reserve Bank of IndiaDocument6 pagesReserve Bank of IndiaKhushboo HedaNo ratings yet

- April 2019Document72 pagesApril 2019Sunil UndarNo ratings yet

- CharterOak EBanking E-BrochureDocument1 pageCharterOak EBanking E-BrochureRhoads ClemmieNo ratings yet

- PAC - Bank Reconciliations and Accounting Concepts TestDocument5 pagesPAC - Bank Reconciliations and Accounting Concepts TestNadir MuhammadNo ratings yet

- Study Material for Promotion ExamsDocument197 pagesStudy Material for Promotion ExamsamarNo ratings yet

- 2018 Annual Report ING Bank N.V.Document288 pages2018 Annual Report ING Bank N.V.Pau LaguertaNo ratings yet

- Bank StatementDocument4 pagesBank StatementKristin BrooksNo ratings yet

- Concurrent AuditDocument15 pagesConcurrent AuditAkash Agarwal100% (2)

- Loan Application Cash Advance BonusDocument1 pageLoan Application Cash Advance BonusSharlene338No ratings yet