You might also like

- AE-036411-001 INDEX For Drawing and EquipmentDocument1 pageAE-036411-001 INDEX For Drawing and Equipmentnarutothunderjet216No ratings yet

- General Guide For CranesDocument19 pagesGeneral Guide For CranesArisNo ratings yet

- CIVIL LAW-Innocent Purchaser in Good Faith and For Value, Presidential Decree (P.D.) 1529Document2 pagesCIVIL LAW-Innocent Purchaser in Good Faith and For Value, Presidential Decree (P.D.) 1529jdonNo ratings yet

- G.R. No. 231581 Tax RemediesDocument11 pagesG.R. No. 231581 Tax RemediesKat100% (1)

- How - To - Guide - List - Classic - Cloud - S4 - Solution ManagerDocument11 pagesHow - To - Guide - List - Classic - Cloud - S4 - Solution ManagerEkrem ErdoganNo ratings yet

- 105 IMPSA Construction Corporation vs. CIR (CTA EB Case No. 685, May 24, 2011)Document10 pages105 IMPSA Construction Corporation vs. CIR (CTA EB Case No. 685, May 24, 2011)Alfred GarciaNo ratings yet

- Reflective EssayDocument13 pagesReflective Essaylufemos OlufemiNo ratings yet

- FAR IFRS QB SampleDocument50 pagesFAR IFRS QB SampleIssa Boy50% (2)

- 02-Analysing BIM Implementation in EgyptianDocument14 pages02-Analysing BIM Implementation in EgyptianAhmed Youssef El-Arabi100% (1)

- Advertising Agency Business PlanDocument16 pagesAdvertising Agency Business PlanProtikshya100% (2)

- 197760Document11 pages197760The Supreme Court Public Information OfficeNo ratings yet

- CIR V Team Energy (2019)Document10 pagesCIR V Team Energy (2019)iptrinidadNo ratings yet

- Northern Mini Hydro vs. CIR CTADocument11 pagesNorthern Mini Hydro vs. CIR CTACamille Yasmeen SamsonNo ratings yet

- TaxDocument34 pagesTaxMichelleNo ratings yet

- 31/epnl - Llir of Tbe I8Bilippines Nprente Qi:Onrt: Iaflanila Third DivisionDocument16 pages31/epnl - Llir of Tbe I8Bilippines Nprente Qi:Onrt: Iaflanila Third DivisionMonocrete Construction Philippines, Inc.No ratings yet

- Court: Republic of The Philippines of Tax Appeals Quezon CityDocument18 pagesCourt: Republic of The Philippines of Tax Appeals Quezon CityDiana BaldozaNo ratings yet

- Misnet Vs CIR PDFDocument9 pagesMisnet Vs CIR PDFMiley LangNo ratings yet

- GR 255470 2023Document12 pagesGR 255470 2023licenselessriderNo ratings yet

- Cta 2D CV 06792 D 2008nov25 RefDocument27 pagesCta 2D CV 06792 D 2008nov25 RefSharon AgapuyanNo ratings yet

- Republic v. First Gas Power Corporation (G.R. No. 214933)Document14 pagesRepublic v. First Gas Power Corporation (G.R. No. 214933)carloNo ratings yet

- Republic Cement vs. CIRDocument25 pagesRepublic Cement vs. CIRDaryl YangaNo ratings yet

- Cta 3D CV 09446 D 2021mar12 RefDocument23 pagesCta 3D CV 09446 D 2021mar12 RefFirenze PHNo ratings yet

- Upreme (!court: L/cpublic of TBC F'bilippincsDocument12 pagesUpreme (!court: L/cpublic of TBC F'bilippincsMonocrete Construction Philippines, Inc.No ratings yet

- TEAM ENERGY CORPORATION vs. COMMISSIONER OF INTERNAL REVENUE January 13, 2014Document5 pagesTEAM ENERGY CORPORATION vs. COMMISSIONER OF INTERNAL REVENUE January 13, 2014ABEGAIL VILLAPANDONo ratings yet

- Court Oft Ax Appeals: Special Third DivisionDocument47 pagesCourt Oft Ax Appeals: Special Third DivisionDean MarkNo ratings yet

- Philex Mining Corporation,: DecisionDocument15 pagesPhilex Mining Corporation,: DecisionHenson MontalvoNo ratings yet

- CIR V Standard Chartered BankDocument9 pagesCIR V Standard Chartered BankFrancesca Isabel MontenegroNo ratings yet

- Duty Free Philippines V Bir DotDocument46 pagesDuty Free Philippines V Bir Dotjaera.unaNo ratings yet

- Lapanday Vs CIRDocument19 pagesLapanday Vs CIRClarissa SawaliNo ratings yet

- CTA Case No. 9074 - Subic Water vs. CIRDocument83 pagesCTA Case No. 9074 - Subic Water vs. CIRJeffrey JosolNo ratings yet

- Upreme Qcourt: Epublit of Tbe Jlbilippines !fflanilaDocument8 pagesUpreme Qcourt: Epublit of Tbe Jlbilippines !fflanilaMonocrete Construction Philippines, Inc.No ratings yet

- Cta Eb CV 00736 D 2012jan10 RefDocument18 pagesCta Eb CV 00736 D 2012jan10 RefFervin VelascoNo ratings yet

- Cta Eb CV 00652 D 2011jul12 RefDocument31 pagesCta Eb CV 00652 D 2011jul12 RefIan InandanNo ratings yet

- Second Division: Republic of The Philippines Court of Tax Appeals Quezon CityDocument50 pagesSecond Division: Republic of The Philippines Court of Tax Appeals Quezon CityJela OasinNo ratings yet

- Cta Eb CV 02527 D 2023apr20 RefDocument31 pagesCta Eb CV 02527 D 2023apr20 RefFirenze PHNo ratings yet

- Cta Eb CV 01515 D 2018mar07 AssDocument20 pagesCta Eb CV 01515 D 2018mar07 AssMaryanne UnoNo ratings yet

- Tax 2 Case 5Document5 pagesTax 2 Case 5carlo_tabangcuraNo ratings yet

- CIR V CE Luzon GeothermalDocument8 pagesCIR V CE Luzon GeothermalAna BelleNo ratings yet

- Cta Eb CV 02729 D 2024mar12 AssDocument22 pagesCta Eb CV 02729 D 2024mar12 AssAnastasia BaliloNo ratings yet

- AC Corporation v. CIR (CTA Case No. 8485)Document29 pagesAC Corporation v. CIR (CTA Case No. 8485)aitoomuchtvNo ratings yet

- CIR v. Standard Chartered BankDocument11 pagesCIR v. Standard Chartered Bankf919No ratings yet

- Nippon Express v. CIRDocument10 pagesNippon Express v. CIRMarchini Sandro Cañizares KongNo ratings yet

- Rhombus Vs CIR - JBersamin - Irrevocability Rule - That When Taxpayer Opted For Taxcredit or Tax Refund, He May Do So It Is Unjustly Rntiched Tha GovernorDocument10 pagesRhombus Vs CIR - JBersamin - Irrevocability Rule - That When Taxpayer Opted For Taxcredit or Tax Refund, He May Do So It Is Unjustly Rntiched Tha Governorsandra mae bonrustroNo ratings yet

- CIR v. SVI TechnologiesDocument23 pagesCIR v. SVI Technologiesaudreydql5No ratings yet

- Republic of The Philippines Court of Tax Appeals Quezon CityDocument19 pagesRepublic of The Philippines Court of Tax Appeals Quezon CityJonJon MivNo ratings yet

- $ Upreme Ql:ourt: 3aepublic Tbe BilippineDocument16 pages$ Upreme Ql:ourt: 3aepublic Tbe BilippineCesar ValeraNo ratings yet

- Second Division: Republic of The Philippines Court of Tax Appeals Quezon CityDocument33 pagesSecond Division: Republic of The Philippines Court of Tax Appeals Quezon CityCJNo ratings yet

- Cta 3D CV 08908 D 2016jul19 RefDocument10 pagesCta 3D CV 08908 D 2016jul19 RefAvelino Garchitorena Alfelor Jr.No ratings yet

- Republic O The Philippines Court of Tax Appeals Quezon CityDocument11 pagesRepublic O The Philippines Court of Tax Appeals Quezon CityAurelia GeeNo ratings yet

- TAXATION - Republic-CIR Vs Team Energy Corp - Tax Refund Credit PDFDocument12 pagesTAXATION - Republic-CIR Vs Team Energy Corp - Tax Refund Credit PDFNatura ManilaNo ratings yet

- L/epublit of Tbe Bilippines Upreme QI::ourt::flllanila: ChairpersonDocument17 pagesL/epublit of Tbe Bilippines Upreme QI::ourt::flllanila: ChairpersonMonocrete Construction Philippines, Inc.No ratings yet

- Panay Power v. CIRDocument10 pagesPanay Power v. CIRaudreydql5No ratings yet

- Cta 2D CV 10175 D 2023jul10 AssDocument27 pagesCta 2D CV 10175 D 2023jul10 AssVince Lupango (imistervince)No ratings yet

- Cta Eb CV 00630 D 2011jan12 RefDocument18 pagesCta Eb CV 00630 D 2011jan12 Refkyla_0111No ratings yet

- Tax 2 CasesDocument33 pagesTax 2 CasessalpanditaNo ratings yet

- Special Second Divisio: P NES LS YDocument13 pagesSpecial Second Divisio: P NES LS YPengNo ratings yet

- Second Division: Republic of The Philippines Court of Tax Appeals Quezon CityDocument8 pagesSecond Division: Republic of The Philippines Court of Tax Appeals Quezon CityCamille CastilloNo ratings yet

- Cta Eb CV 00520 D 2010dec10 RefDocument17 pagesCta Eb CV 00520 D 2010dec10 Refkyla_0111No ratings yet

- Cta 3D CV 08694 A 2018jun28 AssDocument25 pagesCta 3D CV 08694 A 2018jun28 AssLady Paul SyNo ratings yet

- Manasoft CaseDocument12 pagesManasoft CaseRuby Patricia MaronillaNo ratings yet

- Cta Eb CV 01569 D 2018jun07 AssDocument29 pagesCta Eb CV 01569 D 2018jun07 AssnorieNo ratings yet

- (!court Ffmantla: of Tbe !lbtltpptnesDocument8 pages(!court Ffmantla: of Tbe !lbtltpptnesMeg AnudonNo ratings yet

- Cta Eb CV 00417 D 2009may21 AssDocument27 pagesCta Eb CV 00417 D 2009may21 AssAnonymous SJHoVmq5No ratings yet

- Ref 3Document49 pagesRef 3yakyakxxNo ratings yet

- Cta - Eb - CV - 01388 - D - 2017mar15 - Ass 2Document28 pagesCta - Eb - CV - 01388 - D - 2017mar15 - Ass 2Le SonneNo ratings yet

- Republic of The Philippines Quezon City: Commissioner InternalDocument13 pagesRepublic of The Philippines Quezon City: Commissioner InternalElmer AbesiaNo ratings yet

- First Division: Republic of The Philippines Court of Tax Appeals Quezon CityDocument36 pagesFirst Division: Republic of The Philippines Court of Tax Appeals Quezon CityYna YnaNo ratings yet

- CIVIL LAW Accretion Ownership, TorrensDocument2 pagesCIVIL LAW Accretion Ownership, TorrensjdonNo ratings yet

- 16) NIPPON EXPRESS Vs CIR - J.MartiresDocument9 pages16) NIPPON EXPRESS Vs CIR - J.MartiresjdonNo ratings yet

- 17) SAN ROQUE Vs CIR - J. MartiresDocument7 pages17) SAN ROQUE Vs CIR - J. MartiresjdonNo ratings yet

- 14) KEPCO SPC Vs BOARD OF INVESTMETS - J.CarandangDocument3 pages14) KEPCO SPC Vs BOARD OF INVESTMETS - J.CarandangjdonNo ratings yet

- 13) DEUTCHE KNOWLEDGE Vs CIR - J Perlas - BernabeDocument3 pages13) DEUTCHE KNOWLEDGE Vs CIR - J Perlas - BernabejdonNo ratings yet

- Employee Voice ThesisDocument6 pagesEmployee Voice Thesissusancoxarlington100% (2)

- Economic Order Quantity (EOQ) : Prepared By: Talha Majeed Khan (M.Phil) Lecturer, UCP, Faculty of Management StudiesDocument7 pagesEconomic Order Quantity (EOQ) : Prepared By: Talha Majeed Khan (M.Phil) Lecturer, UCP, Faculty of Management StudieszubairNo ratings yet

- Proximity Manufacturing For Enhancing Clothing Supply Chain SustainabilityDocument33 pagesProximity Manufacturing For Enhancing Clothing Supply Chain Sustainabilityarafat saleheenNo ratings yet

- OEM Predictive Maintenance Monitoring - Litmus Automation Case Study - John - YounesDocument2 pagesOEM Predictive Maintenance Monitoring - Litmus Automation Case Study - John - Younesdeepaksaini138No ratings yet

- ACC 02 PROCESS MANUAL Liquidation of Cash AdvancesDocument2 pagesACC 02 PROCESS MANUAL Liquidation of Cash AdvancesMaricrisNo ratings yet

- 3.2 Commissioner V CADocument8 pages3.2 Commissioner V CAJayNo ratings yet

- Probate - WillDocument8 pagesProbate - WillClarence MbeteraNo ratings yet

- Jurnal 2Document15 pagesJurnal 2Dharini MustikaNo ratings yet

- Sampathcards December Seasonal Offers 2022Document18 pagesSampathcards December Seasonal Offers 2022I.M JayawickramaNo ratings yet

- Application Note Metallography of WeldsDocument8 pagesApplication Note Metallography of WeldsLorena Grijalba LeónNo ratings yet

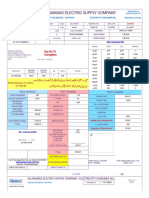

- Iesco Online BillDocument1 pageIesco Online BillRocky BhaiNo ratings yet

- Employee Signature Name/Signature: To Be Fiiled Out by Hr/ManagerDocument1 pageEmployee Signature Name/Signature: To Be Fiiled Out by Hr/ManagerHR Dept - Gemini Agri Farm Solutions Corp.No ratings yet

- Chapter 1 - Accounting For Partnership Firms - Fundamentals - Volume IDocument68 pagesChapter 1 - Accounting For Partnership Firms - Fundamentals - Volume IVISHNUKUMAR S VNo ratings yet

- SemiconductorDocument10 pagesSemiconductorYulia KartikaningrumNo ratings yet

- The Impact of Political Risk On Foreign Direct Inv PDFDocument20 pagesThe Impact of Political Risk On Foreign Direct Inv PDFGeovani Hernandez MartinezNo ratings yet

- The Revised Corporation Code of The Philippines Republic Act No. 11232Document30 pagesThe Revised Corporation Code of The Philippines Republic Act No. 11232Poison IvyNo ratings yet

- Cultural Drivers of Corruption in GovernanceDocument2 pagesCultural Drivers of Corruption in GovernanceJonalvin KENo ratings yet

- ANNEX B - CPMD Secretary's Certificate Basic Def2Document2 pagesANNEX B - CPMD Secretary's Certificate Basic Def2jhesa faith magnanao100% (1)

- MBA First Year First Semester - October - February Course Code Course Credit Units StatusDocument2 pagesMBA First Year First Semester - October - February Course Code Course Credit Units StatusLadipo AilaraNo ratings yet

- An Experimental Analysis On Overall Equipment EffectivenessDocument16 pagesAn Experimental Analysis On Overall Equipment EffectivenessInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Course Note 2 - RA6117284 - Sofia Rizki AuliaDocument2 pagesCourse Note 2 - RA6117284 - Sofia Rizki Auliasofia auliaNo ratings yet

- Coach Ticket EUMAF424Document1 pageCoach Ticket EUMAF424Abhilash SreekumarNo ratings yet

- Big DataDocument6 pagesBig DataSankari SoniNo ratings yet