You might also like

- Syllabus Law of Torts Semester Iii Course Teachers: Dr. Dipak Das & Dr. Kiran KoriDocument3 pagesSyllabus Law of Torts Semester Iii Course Teachers: Dr. Dipak Das & Dr. Kiran KoriTaruna ShandilyaNo ratings yet

- Child Labour in IndiaDocument26 pagesChild Labour in IndiaMuskan KhatriNo ratings yet

- Meva Devi Vs JagannathDocument11 pagesMeva Devi Vs JagannathTaruna ShandilyaNo ratings yet

- In The Honourable Supreme Court of IndiaDocument11 pagesIn The Honourable Supreme Court of IndiaTaruna ShandilyaNo ratings yet

- Scope and Significance of Dividend Policy: Debenture and Debenture Trustee A Project of Corporate Law OnDocument25 pagesScope and Significance of Dividend Policy: Debenture and Debenture Trustee A Project of Corporate Law OnTaruna ShandilyaNo ratings yet

- Brundtland CommissionDocument3 pagesBrundtland CommissionApoorvaChandraNo ratings yet

- Agenda 21Document1 pageAgenda 21HemantVermaNo ratings yet

- Admin 6 RepeatDocument20 pagesAdmin 6 RepeatTaruna ShandilyaNo ratings yet

- Abrogation of Article 370 of Indian Constitution: A Politico-Legal AnalysisDocument21 pagesAbrogation of Article 370 of Indian Constitution: A Politico-Legal AnalysisTaruna Shandilya100% (1)

- PPP EssayDocument14 pagesPPP EssayTaruna ShandilyaNo ratings yet

- Legal Fiction by Heny Maine As A Tool For Legal DevelopmentDocument18 pagesLegal Fiction by Heny Maine As A Tool For Legal DevelopmentTaruna ShandilyaNo ratings yet

- Extra Judicial Confession Not Referred During N Investigation Amounts To ConfessionDocument18 pagesExtra Judicial Confession Not Referred During N Investigation Amounts To ConfessionTaruna ShandilyaNo ratings yet

- Land Law 8repeatDocument17 pagesLand Law 8repeatTaruna ShandilyaNo ratings yet

- Dr. Kaumudhi Challa: The Distinction Between Sovereign Function and Non-Sovereign Functions and Its RelevanceDocument19 pagesDr. Kaumudhi Challa: The Distinction Between Sovereign Function and Non-Sovereign Functions and Its RelevanceTaruna ShandilyaNo ratings yet

- Winding Up of A Company: Paradigm Change in View of Insolvency and Bankruptcy CodeDocument15 pagesWinding Up of A Company: Paradigm Change in View of Insolvency and Bankruptcy CodeTaruna Shandilya100% (1)

- Abrogation of Article 370 of Indian Constitution: A Politico-Legal AnalysisDocument21 pagesAbrogation of Article 370 of Indian Constitution: A Politico-Legal AnalysisTaruna Shandilya100% (1)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Rent Control LawsDocument57 pagesRent Control Lawsd_scorpion50% (2)

- dpc8 REPEATDocument14 pagesdpc8 REPEATTaruna ShandilyaNo ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Standard RentDocument2 pagesStandard RentTaruna ShandilyaNo ratings yet

- Memo3 Meva Devi Vs JagannathDocument11 pagesMemo3 Meva Devi Vs JagannathTaruna ShandilyaNo ratings yet

- Westphalian Sovereignty: Draft Declaration On Rights and Duties of StatesDocument4 pagesWestphalian Sovereignty: Draft Declaration On Rights and Duties of StatesTaruna ShandilyaNo ratings yet

- Dr. Kaumudhi Challa: The Distinction Between Sovereign Function and Non-Sovereign Functions and Its RelevanceDocument19 pagesDr. Kaumudhi Challa: The Distinction Between Sovereign Function and Non-Sovereign Functions and Its RelevanceTaruna ShandilyaNo ratings yet

- Extra Judicial Confession Not Referred During N Investigation Amounts To ConfessionDocument18 pagesExtra Judicial Confession Not Referred During N Investigation Amounts To ConfessionTaruna ShandilyaNo ratings yet

- Admin 6 RepeatDocument20 pagesAdmin 6 RepeatTaruna ShandilyaNo ratings yet

- Evidence Law ProjectDocument21 pagesEvidence Law ProjectAnha Rizvi50% (2)

- ADRDocument18 pagesADRTaruna ShandilyaNo ratings yet

- Profits & Gains of Business or ProfessionDocument11 pagesProfits & Gains of Business or ProfessionTaruna ShandilyaNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Uhura Company Has Decided To Expand Its Operations The BookkeepDocument1 pageUhura Company Has Decided To Expand Its Operations The BookkeepM Bilal SaleemNo ratings yet

- Evike Order 3939175Document3 pagesEvike Order 3939175Carlos CrisostomoNo ratings yet

- Option Valuation Black ScholesDocument18 pagesOption Valuation Black ScholessanchiNo ratings yet

- STATICVendor Document Submission Checklist 12 Feb 2015Document9 pagesSTATICVendor Document Submission Checklist 12 Feb 2015zhangjieNo ratings yet

- Inquiry Ali Vasquez The Florida Bar Re UPL Marty Stone MRLPDocument10 pagesInquiry Ali Vasquez The Florida Bar Re UPL Marty Stone MRLPNeil GillespieNo ratings yet

- Std. X Ch. 3 Money and Credit WS (21 - 22)Document3 pagesStd. X Ch. 3 Money and Credit WS (21 - 22)YASHVI MODINo ratings yet

- Management 8th Edition Kinicki Solutions Manual 1Document66 pagesManagement 8th Edition Kinicki Solutions Manual 1rodney100% (52)

- Consolidated Financial Statement Excercise 3-4Document2 pagesConsolidated Financial Statement Excercise 3-4Winnie TanNo ratings yet

- Law Chapter 3Document6 pagesLaw Chapter 3Yap AustinNo ratings yet

- CV Template 0018Document1 pageCV Template 0018Rahma idahNo ratings yet

- QC Senior Compliance Attorney in Washington DC Resume Tina GreeneDocument2 pagesQC Senior Compliance Attorney in Washington DC Resume Tina GreeneTinaGreeneNo ratings yet

- Change Management at UnileverDocument10 pagesChange Management at UnileverAnika JahanNo ratings yet

- Principles of Taxation Law 2022 Chapter4Document30 pagesPrinciples of Taxation Law 2022 Chapter4Kaylah NewcombeNo ratings yet

- Study Regarding Innovation and Entrepreneurship in Romanian SmesDocument6 pagesStudy Regarding Innovation and Entrepreneurship in Romanian SmesAlex ObrejanNo ratings yet

- Other SourceDocument43 pagesOther SourceJai RajNo ratings yet

- Practice Question (Accounting Cycle) With Solution v2Document17 pagesPractice Question (Accounting Cycle) With Solution v2Laiba ManzoorNo ratings yet

- Financial Statements of Banking CompaniesDocument29 pagesFinancial Statements of Banking CompaniesPlatonic100% (12)

- Accenture Cover LetterDocument8 pagesAccenture Cover Letterafjwrcqmzuxzxg100% (2)

- Oilsafe Identification LabelsDocument12 pagesOilsafe Identification LabelsHesham MahdyNo ratings yet

- Orient Air Services & Hotel Representatives vs. Court of AppealsDocument3 pagesOrient Air Services & Hotel Representatives vs. Court of AppealsRafael AdanNo ratings yet

- Market Segmentation Strategic Analysis and Positioning ToolDocument4 pagesMarket Segmentation Strategic Analysis and Positioning ToolshadrickNo ratings yet

- Capstone Project-Grainger and Bosch: Digital Marketing CampaignDocument25 pagesCapstone Project-Grainger and Bosch: Digital Marketing Campaignk.saikumar100% (1)

- Research On Fastrack WatchesDocument23 pagesResearch On Fastrack Watcheskk_kamal40% (5)

- SM SX 52 SpecificatonDocument2 pagesSM SX 52 SpecificatonAli HussnainNo ratings yet

- MCom - Accounts ch-13 Topic3Document19 pagesMCom - Accounts ch-13 Topic3Sameer GoyalNo ratings yet

- MARINGO Category 1 (HOUSE 1310) Occupier For January 2023Document1 pageMARINGO Category 1 (HOUSE 1310) Occupier For January 2023sophia sambaNo ratings yet

- Presentation 4 - Cost & Management Accounting - March 10, 209 - 3pm To 6pmDocument45 pagesPresentation 4 - Cost & Management Accounting - March 10, 209 - 3pm To 6pmBhunesh KumarNo ratings yet

- Chapter IDocument6 pagesChapter IRamir Zsamski Samon100% (2)

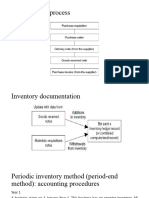

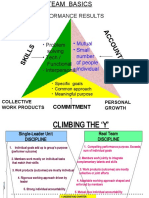

- Team BasicsDocument3 pagesTeam BasicsSoumya Jyoti BhattacharyaNo ratings yet

- Master in Business Administration: Join Our Global CommunityDocument8 pagesMaster in Business Administration: Join Our Global Communityfrans1593No ratings yet