You might also like

- Challenges Faced by Local Councils in ZambiaDocument18 pagesChallenges Faced by Local Councils in ZambiaEvangelist Kabaso Sydney78% (9)

- A Study On Working Capital Management at Traco Cable Company LTD NewDocument95 pagesA Study On Working Capital Management at Traco Cable Company LTD Newneesh50% (2)

- Corporate Governance: A practical guide for accountantsFrom EverandCorporate Governance: A practical guide for accountantsRating: 5 out of 5 stars5/5 (1)

- 2016 PLAN7141 Course OutlineDocument12 pages2016 PLAN7141 Course Outlinechristy.laiNo ratings yet

- Audit Report Lag and The Effectiveness of Audit Committee Among Malaysian Listed CompaniesDocument12 pagesAudit Report Lag and The Effectiveness of Audit Committee Among Malaysian Listed Companiesxaxif8265100% (1)

- Ado 2020Document7 pagesAdo 2020arielNo ratings yet

- Audit Report LagDocument22 pagesAudit Report LagalfionitaNo ratings yet

- Does Ownership Characteristics Have Any Impact On Audit Report Lag? Evidence of Malaysian Listed CompaniesDocument13 pagesDoes Ownership Characteristics Have Any Impact On Audit Report Lag? Evidence of Malaysian Listed CompaniesahmadhidrNo ratings yet

- Audit Quality: A Literature Overview and Research Synthesis: IOSR Journal of Business and Management February 2020Document12 pagesAudit Quality: A Literature Overview and Research Synthesis: IOSR Journal of Business and Management February 2020siti rizki ayuniahNo ratings yet

- Corporate Governanceand Financial Performanceof Nigeria Listed BanksDocument7 pagesCorporate Governanceand Financial Performanceof Nigeria Listed BanksFathin SyifayaniNo ratings yet

- Audit Committee Composition and Auditor Reporting: A Malaysian CaseDocument8 pagesAudit Committee Composition and Auditor Reporting: A Malaysian CaseBara HakikiNo ratings yet

- Also, TTDocument11 pagesAlso, TTNUR FARAH ALIAH RAMLANNo ratings yet

- Corporate Governance and Financial Performance of Nigeria Listed BanksDocument7 pagesCorporate Governance and Financial Performance of Nigeria Listed Banksadegokeoladayo0106No ratings yet

- 10.1108@maj 09 2019 2405Document36 pages10.1108@maj 09 2019 2405Rusli RusliNo ratings yet

- Earnings Management and Quality of Accounting Information in JordanDocument14 pagesEarnings Management and Quality of Accounting Information in JordanVeronika BellaNo ratings yet

- The Impact of Audit Quality On The Financial Performance of Listed Companies NigeriaDocument6 pagesThe Impact of Audit Quality On The Financial Performance of Listed Companies NigeriaKathlyn BrawleyNo ratings yet

- Inggris s2Document6 pagesInggris s2Irma CakeNo ratings yet

- 944-Texte de L'article-2977-1-10-20221219Document15 pages944-Texte de L'article-2977-1-10-20221219boubker moulineNo ratings yet

- MakaB SureshN 2018 ReviewofFinancialPerformanceanalysisofCorporateOrganizations AsianJournalofManagement91500-506Document8 pagesMakaB SureshN 2018 ReviewofFinancialPerformanceanalysisofCorporateOrganizations AsianJournalofManagement91500-506TharunyaNo ratings yet

- Jurnal Manajemen KeuanganDocument7 pagesJurnal Manajemen Keuanganla ode muhamad nurrakhmadNo ratings yet

- Audit Committee and LagDocument18 pagesAudit Committee and Lagraihan.aisNo ratings yet

- Liquidity Analysis of Selected Public-Listed CompaDocument21 pagesLiquidity Analysis of Selected Public-Listed CompanhishamNo ratings yet

- Al-Qublani, Kamardin, Shafie - 2020 - Audit Committee Chair Attributes and Audit Report Lag in An Emerging Market-AnnotatedDocument18 pagesAl-Qublani, Kamardin, Shafie - 2020 - Audit Committee Chair Attributes and Audit Report Lag in An Emerging Market-Annotatedahmad lutfieNo ratings yet

- Non-Audit Services, Audit Firm Tenure and Earnings Management in MalaysiaDocument24 pagesNon-Audit Services, Audit Firm Tenure and Earnings Management in MalaysiaRafni JulitaNo ratings yet

- Audit Committee Effectiveness and Company PerformaDocument14 pagesAudit Committee Effectiveness and Company PerformaShaquila DNo ratings yet

- Factors Determining Quality of Financial Information in Bangladesh's Cement SectorDocument9 pagesFactors Determining Quality of Financial Information in Bangladesh's Cement SectorZeeni KhanNo ratings yet

- 10 The Internal Control Practice of Jumhouria and Sahara Banks in LibyaDocument11 pages10 The Internal Control Practice of Jumhouria and Sahara Banks in Libyadek wikNo ratings yet

- Liquidity Analysis of Selected Public-Listed Companies in MalaysiaDocument21 pagesLiquidity Analysis of Selected Public-Listed Companies in MalaysiaAhmad AimanNo ratings yet

- Auditor Client RelationshipDocument14 pagesAuditor Client Relationshipekka_mollyNo ratings yet

- A STUDY ON RATIO ANALYSIS OF SundaramDocument64 pagesA STUDY ON RATIO ANALYSIS OF SundaramDivyansh VermaNo ratings yet

- Analysis of Key Audit Matters Disclosures and Corporate GovernanceDocument25 pagesAnalysis of Key Audit Matters Disclosures and Corporate GovernanceNUR FARAH ALIAH RAMLANNo ratings yet

- Corporate Governance & Key Audit MattersDocument25 pagesCorporate Governance & Key Audit MattersNUR FARAH ALIAH RAMLANNo ratings yet

- Conceptual Relationship Between Corporate Governance and Audit Quality in Shari'ah Compliant Companies Listed On Bursa MalaysiaDocument9 pagesConceptual Relationship Between Corporate Governance and Audit Quality in Shari'ah Compliant Companies Listed On Bursa MalaysiaRecca DamayantiNo ratings yet

- Does Audit Fees and Non-Audit Fees Matters in Audit Quality?Document11 pagesDoes Audit Fees and Non-Audit Fees Matters in Audit Quality?Addoula TOUNSINo ratings yet

- The Effect of Audit Evidence On The Auditor'S Report: Akram Niktaba Azim AslaniDocument5 pagesThe Effect of Audit Evidence On The Auditor'S Report: Akram Niktaba Azim AslaniNinaRzk SNo ratings yet

- An Examination of The Utilization of Audit TechnologyDocument28 pagesAn Examination of The Utilization of Audit TechnologyHEMALA A/P VEERASINGAM MoeNo ratings yet

- Impact of Audit Failures and Internal Control On Performance of Public Companies in OmanDocument9 pagesImpact of Audit Failures and Internal Control On Performance of Public Companies in OmanBOHR International Journal of Business Ethics and Corporate GovernanceNo ratings yet

- Effectsof Applicationof IFRSonthe Qualityof FinancialDocument13 pagesEffectsof Applicationof IFRSonthe Qualityof FinancialAbdullahNo ratings yet

- Draft Ria 1Document23 pagesDraft Ria 1NUR FARAH ALIAH RAMLANNo ratings yet

- Chief Executive Officer Characteristics and Financial Restatements in MalaysiaDocument15 pagesChief Executive Officer Characteristics and Financial Restatements in MalaysiaHassan MujtabaNo ratings yet

- Factors Affecting Audit Switching: A Logistic Regression StudyDocument21 pagesFactors Affecting Audit Switching: A Logistic Regression StudyAnnisa FithriNo ratings yet

- Audit Report Lag FactorsDocument20 pagesAudit Report Lag FactorsferiajaNo ratings yet

- 290-Article Text-637-1-10-20160929Document15 pages290-Article Text-637-1-10-20160929Faraz Khoso BalochNo ratings yet

- Corporate GovernanceDocument24 pagesCorporate GovernanceUlly Nur Eka PutriNo ratings yet

- Working Capital Management and Financial Performance: Evidence From Listed Food and Beverage Companies in South AfricaDocument11 pagesWorking Capital Management and Financial Performance: Evidence From Listed Food and Beverage Companies in South AfricaKatherine HoàngNo ratings yet

- Denny Novi Satria, Syahril Ali, Denny Yohana: Faculty of Economics Andalas University Padang, West Sumatera, IndonesiaDocument8 pagesDenny Novi Satria, Syahril Ali, Denny Yohana: Faculty of Economics Andalas University Padang, West Sumatera, IndonesiaKarina AprilliaNo ratings yet

- The Relationship Between Cash Conversion Cycle and Firm Profitability: Special Reference To Themanufacturing Companies in Colombo Stock ExchangeDocument11 pagesThe Relationship Between Cash Conversion Cycle and Firm Profitability: Special Reference To Themanufacturing Companies in Colombo Stock ExchangeMuhammad RaafayNo ratings yet

- Ijsar 6048 PDFDocument10 pagesIjsar 6048 PDFInsyiraah Oxaichiko ArissintaNo ratings yet

- Precious Mbah Project OriginalDocument47 pagesPrecious Mbah Project Originaladebowale adejengbeNo ratings yet

- Assignment On: "Impact of Cost Accounting On Business Decision Making in Manufacturing Industries of Bangladesh''Document9 pagesAssignment On: "Impact of Cost Accounting On Business Decision Making in Manufacturing Industries of Bangladesh''Enaiya IslamNo ratings yet

- Hanya AbstrakDocument35 pagesHanya AbstrakNisrinaNo ratings yet

- Bai Nghien Cuu 5Document12 pagesBai Nghien Cuu 5Ưng Nguyễn Thị KimNo ratings yet

- Effects of Internal Audit Practice On Organizational Performance of Remittance Companies in Modadishu-SomaliaDocument22 pagesEffects of Internal Audit Practice On Organizational Performance of Remittance Companies in Modadishu-SomaliaFaraz Khoso BalochNo ratings yet

- Sujarwo, 2019Document10 pagesSujarwo, 2019Putu Krisna Bayu PutraNo ratings yet

- DOC-20240417-WA0012Document124 pagesDOC-20240417-WA0012josmyshamginNo ratings yet

- InternalDocument6 pagesInternalalmeiidany97No ratings yet

- Impact of Working Capital On Corporate Performance A Case Study From Cement, Chemical and Engineering Sectors of PakistanDocument11 pagesImpact of Working Capital On Corporate Performance A Case Study From Cement, Chemical and Engineering Sectors of PakistanAlex NjingaNo ratings yet

- Audit committee effectiveness and timely financial reportingDocument22 pagesAudit committee effectiveness and timely financial reportingahmadhidrNo ratings yet

- The Development of Shariah Audit Scope in Malaysian Takaful Industry: A Preliminary AnalysisDocument22 pagesThe Development of Shariah Audit Scope in Malaysian Takaful Industry: A Preliminary AnalysisnsNo ratings yet

- ASIC Audit ReportDocument10 pagesASIC Audit ReportVidyaa IndiaNo ratings yet

- Towards an XBRL-enabled corporate governance reporting taxonomy.: An empirical study of NYSE-listed Financial InstitutionsFrom EverandTowards an XBRL-enabled corporate governance reporting taxonomy.: An empirical study of NYSE-listed Financial InstitutionsRating: 1 out of 5 stars1/5 (1)

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- Karawang International Industrial City Annual Report 2020Document181 pagesKarawang International Industrial City Annual Report 2020Irma CakeNo ratings yet

- Ar.2 JababekaDocument362 pagesAr.2 JababekaIrma CakeNo ratings yet

- 3.patricia Diana PDFDocument10 pages3.patricia Diana PDFirmaNo ratings yet

- Weathering Challenges, Capturing Opportunities (WCCODocument264 pagesWeathering Challenges, Capturing Opportunities (WCCOAndry WirawanNo ratings yet

- E-Payment: Buzz Word or Reality: Vishal Acharya, S. O. Junare, Dharmesh D. GadhaviDocument8 pagesE-Payment: Buzz Word or Reality: Vishal Acharya, S. O. Junare, Dharmesh D. GadhaviIrma CakeNo ratings yet

- What Drives The Adoption of Mobile Payment? A Malaysian PerspectiveDocument16 pagesWhat Drives The Adoption of Mobile Payment? A Malaysian PerspectiveIrma CakeNo ratings yet

- AfifyDocument3 pagesAfifyIrma CakeNo ratings yet

- Inggris s2Document6 pagesInggris s2Irma CakeNo ratings yet

- The Future of Jobs: Employment, Skills and Workforce Strategy For The Fourth Industrial RevolutionDocument66 pagesThe Future of Jobs: Employment, Skills and Workforce Strategy For The Fourth Industrial RevolutionIrma CakeNo ratings yet

- Jurnal 2Document16 pagesJurnal 2Irma CakeNo ratings yet

- WEF Future of Jobs MarkedDocument167 pagesWEF Future of Jobs Markedharuhi.karasunoNo ratings yet

- Jurnal 2Document16 pagesJurnal 2Irma CakeNo ratings yet

- Agensi 1Document17 pagesAgensi 1Irma CakeNo ratings yet

- Audit Tenure and Quality To Audit Report Lag in Banking: L.S. Wiyantoro, F. UsmanDocument12 pagesAudit Tenure and Quality To Audit Report Lag in Banking: L.S. Wiyantoro, F. UsmanIrma CakeNo ratings yet

- ShoesDocument31 pagesShoesIrma CakeNo ratings yet

- Behavioral Accounting in Retrospect and Prospect : London School of Economics and Political ScienceDocument22 pagesBehavioral Accounting in Retrospect and Prospect : London School of Economics and Political ScienceIrma CakeNo ratings yet

- WEF Future of Jobs2Document177 pagesWEF Future of Jobs2Irma CakeNo ratings yet

- IPPTChap 011Document43 pagesIPPTChap 011Nia ニア MulyaningsihNo ratings yet

- IPPTChap 011Document43 pagesIPPTChap 011Nia ニア MulyaningsihNo ratings yet

- P/N's UP AUC Dollars TPDocument2 pagesP/N's UP AUC Dollars TPIrma CakeNo ratings yet

- Ode Tabaco CompanyDocument21 pagesOde Tabaco CompanyIrma CakeNo ratings yet

- ShoesDocument31 pagesShoesIrma CakeNo ratings yet

- Presentasi CA MKL PDFDocument21 pagesPresentasi CA MKL PDFIrma CakeNo ratings yet

- Part D - Disclosure and TransparencyDocument21 pagesPart D - Disclosure and TransparencyIrma CakeNo ratings yet

- PLDT Asean Corporate Governance Scorecard 2014Document92 pagesPLDT Asean Corporate Governance Scorecard 2014Irma CakeNo ratings yet

- Supplemental Note #1 - General Principles of Taxation, Intro To Income TaxationDocument9 pagesSupplemental Note #1 - General Principles of Taxation, Intro To Income TaxationRicojay FernandezNo ratings yet

- NDU Thesis Final After Def - Maritime Security Challenges in The Indian Ocean RegionDocument70 pagesNDU Thesis Final After Def - Maritime Security Challenges in The Indian Ocean Regionsyed_sazidNo ratings yet

- Abstract - Tropen Tag 2011 PDFDocument634 pagesAbstract - Tropen Tag 2011 PDFzmoghesNo ratings yet

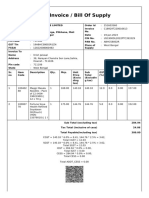

- Tax Invoice / Bill of SupplyDocument2 pagesTax Invoice / Bill of SupplyKrish JaiswalNo ratings yet

- Barbados Elects First President as Island Becomes RepublicDocument2 pagesBarbados Elects First President as Island Becomes Republiccemre türkmenNo ratings yet

- Philippine Constitution, General Information, Current EventsDocument19 pagesPhilippine Constitution, General Information, Current EventsAr-Ar CallejaNo ratings yet

- MCCG 2021 Effective Date & Key ChangesDocument63 pagesMCCG 2021 Effective Date & Key ChangesUKLead ServicesNo ratings yet

- Chapter 2 Note Audit From The Book. Learning Object 1 Define The Various Types of Fraud That Affect OrganizationDocument12 pagesChapter 2 Note Audit From The Book. Learning Object 1 Define The Various Types of Fraud That Affect OrganizationkimkimNo ratings yet

- Ainun NaimDocument4 pagesAinun NaimAnita CeceNo ratings yet

- Environmental Governance in the PhilippinesDocument37 pagesEnvironmental Governance in the PhilippinesEira Raye100% (2)

- Trustee Recruitment 2023: Closing Date 23:59 Sunday 6 AUGUST 2023Document12 pagesTrustee Recruitment 2023: Closing Date 23:59 Sunday 6 AUGUST 2023Stace INo ratings yet

- Ieps 2 Information TechnoDocument63 pagesIeps 2 Information TechnofelixjmhNo ratings yet

- Proposals approved by Steering Committee under IMPRESS schemeDocument88 pagesProposals approved by Steering Committee under IMPRESS schemeAmit AgrawalNo ratings yet

- Define a Concept PaperDocument46 pagesDefine a Concept PaperChristian De Guzman100% (2)

- BA4 Notes CimaDocument25 pagesBA4 Notes CimakateNo ratings yet

- Democratic Governance Within The European Union and The African UnionDocument15 pagesDemocratic Governance Within The European Union and The African UnionSandra Ochieng SpringerNo ratings yet

- Pillar 3 Disclosure 2021Document13 pagesPillar 3 Disclosure 2021Khadim HussainNo ratings yet

- Constitution (PDF)Document221 pagesConstitution (PDF)Noômen Ben HassinNo ratings yet

- Lesson Plan in PPG Laws of ElectionDocument9 pagesLesson Plan in PPG Laws of ElectionMarlon CuevasNo ratings yet

- Negri - Philosophy of Law Against Sovereignty - New Excesses, Old FragmentationsDocument9 pagesNegri - Philosophy of Law Against Sovereignty - New Excesses, Old FragmentationsZahra HussainNo ratings yet

- Philippine Development Plan 2023 2028 With LinkDocument450 pagesPhilippine Development Plan 2023 2028 With LinkAdrian PhNo ratings yet

- MVF Business Guide:: Reporting To Directors, Advisors, and InvestorsDocument10 pagesMVF Business Guide:: Reporting To Directors, Advisors, and InvestorsJeetesh HarjaniNo ratings yet

- UNDEF Project Proposal Guidelines 2016 EN - 2Document15 pagesUNDEF Project Proposal Guidelines 2016 EN - 2irmaNo ratings yet

- 12 Municipal V International Law DiffDocument18 pages12 Municipal V International Law Diffrahulchaudhary9730No ratings yet

- Format. Hum - An Intensive Study of Governance and Sustainability of CMRC - Community Managed Resource CentreDocument12 pagesFormat. Hum - An Intensive Study of Governance and Sustainability of CMRC - Community Managed Resource CentreImpact JournalsNo ratings yet

- Application Handbook VM004 Optimise Procurement Cost Banking Value ManagementDocument6 pagesApplication Handbook VM004 Optimise Procurement Cost Banking Value Managementsopon567No ratings yet

- Table of ContentsDocument289 pagesTable of ContentsScientia Asian Institute Inc.No ratings yet

- The City We Need TCWN - 2.0Document38 pagesThe City We Need TCWN - 2.0Francisco Jose Rovira MejiaNo ratings yet