You might also like

- CIR v. ESSO Standard 1989Document4 pagesCIR v. ESSO Standard 1989Mark Ebenezer BernardoNo ratings yet

- E. CIR v. ESSO Standard Eastern Inc.Document2 pagesE. CIR v. ESSO Standard Eastern Inc.pb Stan accountNo ratings yet

- Commissioner of Internal Revenue v. Esso Standard Eastern, Inc.Document4 pagesCommissioner of Internal Revenue v. Esso Standard Eastern, Inc.ショーンカトリーナNo ratings yet

- Cir v. Esso Standard Eastern Inc 172 Scra 3646.Document3 pagesCir v. Esso Standard Eastern Inc 172 Scra 3646.Joshua RodriguezNo ratings yet

- G.R. Nos. L-28502-03Document2 pagesG.R. Nos. L-28502-03JohnnyPenafloridaNo ratings yet

- CIR vs. Esso Standard EasternDocument4 pagesCIR vs. Esso Standard EasternCharish DanaoNo ratings yet

- (G.R. Nos. L-28502-03, April 18, 1989)Document3 pages(G.R. Nos. L-28502-03, April 18, 1989)rommel alimagnoNo ratings yet

- STC PresumptionsDocument12 pagesSTC PresumptionsKate FielNo ratings yet

- CIR Vs Esso StandardDocument2 pagesCIR Vs Esso StandardKenmar NoganNo ratings yet

- CIR vs. Esso Standard: Compensation and Set-OffDocument2 pagesCIR vs. Esso Standard: Compensation and Set-OffGabriel HernandezNo ratings yet

- CIR vs. ESSODocument1 pageCIR vs. ESSOmaximum jicaNo ratings yet

- Commissioner of Internal Revenue vs. Esso Standard Eastern, Inc.Document9 pagesCommissioner of Internal Revenue vs. Esso Standard Eastern, Inc.Jayson FranciscoNo ratings yet

- Commissioner of Internal Revenue vs. Esso Standard Eastern IncDocument2 pagesCommissioner of Internal Revenue vs. Esso Standard Eastern IncVeen Galicinao FernandezNo ratings yet

- Commissioner of Internal Revenue vs. Esso Standard Eastern IncDocument2 pagesCommissioner of Internal Revenue vs. Esso Standard Eastern IncVeen Galicinao FernandezNo ratings yet

- Cir VS EssoDocument2 pagesCir VS EssoApril Joyce NatadNo ratings yet

- 142360-1969-Commissioner of Internal Revenue V.20180927-5466-1g9rexeDocument4 pages142360-1969-Commissioner of Internal Revenue V.20180927-5466-1g9rexethirdy demaisipNo ratings yet

- Cir V Itogon-Suyoc MinESDocument2 pagesCir V Itogon-Suyoc MinESkeloNo ratings yet

- CIR Vs ESSoDocument1 pageCIR Vs ESSoJhoey BuenoNo ratings yet

- Case Digest - Doctrines in TaxationDocument3 pagesCase Digest - Doctrines in TaxationBryne Angelo BrillantesNo ratings yet

- Palanca v. CIR PDFDocument11 pagesPalanca v. CIR PDFnichols greenNo ratings yet

- First DivisionDocument45 pagesFirst DivisionmifajNo ratings yet

- Supreme Court: Office of The Solicitor General For Petitioner. Ross, Selph and Carrascoso For Respondent CompanyDocument9 pagesSupreme Court: Office of The Solicitor General For Petitioner. Ross, Selph and Carrascoso For Respondent CompanyRaziele RanesesNo ratings yet

- 5 Percentage CasesDocument42 pages5 Percentage CasesRichelle Grace LagguiNo ratings yet

- 25 G.R. No. 160528Document6 pages25 G.R. No. 160528Jessel MaglinteNo ratings yet

- 123722-1999-Commissioner of Internal Revenue v. Court Of20210423-12-13dw8k8Document24 pages123722-1999-Commissioner of Internal Revenue v. Court Of20210423-12-13dw8k8ChukyowtNo ratings yet

- Taxation Cases Relevant DoctrinesDocument11 pagesTaxation Cases Relevant DoctrinesClarisse-joan GarmaNo ratings yet

- 6 Arches Vs BellosilloDocument6 pages6 Arches Vs BellosilloJeanne CalalinNo ratings yet

- Digest RR 8-2019Document2 pagesDigest RR 8-2019Nikki GarciaNo ratings yet

- Republic vs. Intermediate Appellate Court 196 SCRA 335Document8 pagesRepublic vs. Intermediate Appellate Court 196 SCRA 335BernsNo ratings yet

- 1 - 115674-2001-Vda. de San Agustin v. Commissioner ofDocument8 pages1 - 115674-2001-Vda. de San Agustin v. Commissioner ofKing ForondaNo ratings yet

- 28.d PNOC vs. CA (G.R. No. 109976 April 26, 2005) - H DigestDocument2 pages28.d PNOC vs. CA (G.R. No. 109976 April 26, 2005) - H DigestHarleneNo ratings yet

- Padilla Law Office For PetitionerDocument5 pagesPadilla Law Office For PetitionerShiela MarieNo ratings yet

- Atlas Fertilizer Vs CIRDocument49 pagesAtlas Fertilizer Vs CIRemgraceNo ratings yet

- ATLAS PrescriptionDocument4 pagesATLAS PrescriptionJesterNo ratings yet

- In Re Sapphire Steamship Lines, Inc., Debtor. Internal Revenue Service v. Trustee, Sapphire Steamship Lines, Inc., 762 F.2d 13, 2d Cir. (1985)Document6 pagesIn Re Sapphire Steamship Lines, Inc., Debtor. Internal Revenue Service v. Trustee, Sapphire Steamship Lines, Inc., 762 F.2d 13, 2d Cir. (1985)Scribd Government DocsNo ratings yet

- Vda. de San Agustin Vs CIRDocument9 pagesVda. de San Agustin Vs CIRKevin MatibagNo ratings yet

- Philex Mining Corporation Vs Commissioner of Internal Revenue GR No. 125704 August 28, 1998Document6 pagesPhilex Mining Corporation Vs Commissioner of Internal Revenue GR No. 125704 August 28, 1998nildin danaNo ratings yet

- 10.d ACCRA Investment Corporation vs. CA (G.R. No. 96322 December 20, 1991) - H DigestDocument2 pages10.d ACCRA Investment Corporation vs. CA (G.R. No. 96322 December 20, 1991) - H DigestHarleneNo ratings yet

- 19 LimacoDocument4 pages19 LimacoChristiane Marie BajadaNo ratings yet

- 22 - GR No. 25299Document1 page22 - GR No. 25299Lloyd LiwagNo ratings yet

- 5 Commissioner - of - Internal - Revenue - v. - Court - of PDFDocument23 pages5 Commissioner - of - Internal - Revenue - v. - Court - of PDFdenbar15No ratings yet

- ESSO STANDARD EASTERN Vs CIR (G.R. No. L-28508-9, July 07, 1989)Document6 pagesESSO STANDARD EASTERN Vs CIR (G.R. No. L-28508-9, July 07, 1989)Gwen Alistaer CanaleNo ratings yet

- CIR vs. San MiguelDocument4 pagesCIR vs. San MiguelJoshua Erik MadriaNo ratings yet

- Anderson Vs Posadas, GR 44100, 22 Sept 1938Document5 pagesAnderson Vs Posadas, GR 44100, 22 Sept 1938Nor-Alissa M DisoNo ratings yet

- Alabang Vs MuntinlupaDocument2 pagesAlabang Vs MuntinlupaLauriz EsquivelNo ratings yet

- AsianBank Corp Vs CIR - CTADocument8 pagesAsianBank Corp Vs CIR - CTAMeg Villarica100% (1)

- Office of The Solicitor General and Atty. G. H. Mantolino For Petitioner. Benedicto and Martinez For RespondentsDocument3 pagesOffice of The Solicitor General and Atty. G. H. Mantolino For Petitioner. Benedicto and Martinez For RespondentsMacky L. Delos ReyesNo ratings yet

- Atlas Fertilizer vs. CommissionerDocument10 pagesAtlas Fertilizer vs. CommissionerBenedick LedesmaNo ratings yet

- Commissioner of Lnternal Revenue vs. Cebu Portlandcement Company 156 Scra 535, December 15, 1987Document50 pagesCommissioner of Lnternal Revenue vs. Cebu Portlandcement Company 156 Scra 535, December 15, 1987AnatheaAcabanNo ratings yet

- G.R.-No.-108576Document11 pagesG.R.-No.-108576Fe Myra LagrosasNo ratings yet

- Accra Investments Corp Vs CADocument4 pagesAccra Investments Corp Vs CAnazhNo ratings yet

- SPIT Cases - Day 5 - EndDocument624 pagesSPIT Cases - Day 5 - EndPeter Lloyd CarpioNo ratings yet

- en Banc - Alabang Supermarket v. City of MuntinlupaDocument2 pagesen Banc - Alabang Supermarket v. City of MuntinlupaPaul Joshua SubaNo ratings yet

- Tax II Case DigestDocument9 pagesTax II Case DigestCesar P ValeraNo ratings yet

- Commissioner of Internal Revenue Vs TMX Sales Inc Et Al 205 SCRA 184 PDFDocument6 pagesCommissioner of Internal Revenue Vs TMX Sales Inc Et Al 205 SCRA 184 PDFTAU MU OFFICIALNo ratings yet

- China Banking Corp Vs CADocument19 pagesChina Banking Corp Vs CAChristelle Ayn BaldosNo ratings yet

- Domingo vs. GarlitosDocument4 pagesDomingo vs. GarlitosJenNo ratings yet

- Republic Vs IACDocument7 pagesRepublic Vs IACnomercykillingNo ratings yet

- 25.d Vda. de San Agustin vs. CIR (G.R. No. 138485 September 10, 2001) - H DigestDocument1 page25.d Vda. de San Agustin vs. CIR (G.R. No. 138485 September 10, 2001) - H DigestHarleneNo ratings yet

- Bar Review Companion: Taxation: Anvil Law Books Series, #4From EverandBar Review Companion: Taxation: Anvil Law Books Series, #4No ratings yet

- CONCEPT OF DOUBLE JEOPARDY IDocument16 pagesCONCEPT OF DOUBLE JEOPARDY IShanen LimNo ratings yet

- RA 9344 - Juvenile Justice LawDocument21 pagesRA 9344 - Juvenile Justice LawArnold OniaNo ratings yet

- Sources LawDocument4 pagesSources LawJoey Villas MaputiNo ratings yet

- Plaintiff-Appellee Vs Vs Accused-Appellant The Solicitor General Public Attorney's OfficeDocument17 pagesPlaintiff-Appellee Vs Vs Accused-Appellant The Solicitor General Public Attorney's OfficeShanen LimNo ratings yet

- DO 10, Series of 1998 - Guidelines On The Imposition of Double Indemnity For Non Compliance of The Prescribed Increases or Adjustments in Wage RatesDocument2 pagesDO 10, Series of 1998 - Guidelines On The Imposition of Double Indemnity For Non Compliance of The Prescribed Increases or Adjustments in Wage RatesAlen Joel PitaNo ratings yet

- Petitioner Vs Vs Respondents: Second DivisionDocument6 pagesPetitioner Vs Vs Respondents: Second DivisionShanen LimNo ratings yet

- 119949-2003-Hambon v. Court of AppealsDocument5 pages119949-2003-Hambon v. Court of AppealsGermaine CarreonNo ratings yet

- Case BriefDocument3 pagesCase BriefDonna Pantoja-Dela FuenteNo ratings yet

- New Applicants PDFDocument6 pagesNew Applicants PDFStella LynNo ratings yet

- How To Read Case LawDocument8 pagesHow To Read Case LawTariq720No ratings yet

- RA 9344 - Juvenile Justice LawDocument21 pagesRA 9344 - Juvenile Justice LawArnold OniaNo ratings yet

- Azarraga vs. GayDocument8 pagesAzarraga vs. GaySNo ratings yet

- Res-020480.html OkDocument6 pagesRes-020480.html OkPetrovichNo ratings yet

- A Liberty Viewed Through American Constitutional Lens: Dissection of Religious Freedom Rights in The PhilippinesDocument6 pagesA Liberty Viewed Through American Constitutional Lens: Dissection of Religious Freedom Rights in The PhilippinesShanen LimNo ratings yet

- The Right of An Accused To Bail in Capital Offenses - An: IllusionDocument24 pagesThe Right of An Accused To Bail in Capital Offenses - An: IllusionShanen LimNo ratings yet

- CONCEPT OF DOUBLE JEOPARDY IDocument16 pagesCONCEPT OF DOUBLE JEOPARDY IShanen LimNo ratings yet

- Juvenile Justice and Welfare Law Implementation: The Philippine Urban Poor City CaseDocument7 pagesJuvenile Justice and Welfare Law Implementation: The Philippine Urban Poor City CaseShanen LimNo ratings yet

- Ratio Decidendi and Obiter Dictum: Introductory RemarksDocument13 pagesRatio Decidendi and Obiter Dictum: Introductory RemarksShanen Lim0% (1)

- Law On Ownership and Other Real Rights PDFDocument62 pagesLaw On Ownership and Other Real Rights PDFkujtim78No ratings yet

- The History of The Per Curiam Opinion: Consensus and Individual Expression On The Supreme CourtDocument18 pagesThe History of The Per Curiam Opinion: Consensus and Individual Expression On The Supreme CourtShanen LimNo ratings yet

- New Applicants PDFDocument6 pagesNew Applicants PDFStella LynNo ratings yet

- Commentary - Greek Legal History - Its Functions and Potentialities PDFDocument15 pagesCommentary - Greek Legal History - Its Functions and Potentialities PDFShanen LimNo ratings yet

- Trial Trial Trial TrialDocument1 pageTrial Trial Trial TrialShanen LimNo ratings yet

- Democracy and Judicial Review: Are They Really Incompatible?Document48 pagesDemocracy and Judicial Review: Are They Really Incompatible?Shanen LimNo ratings yet

- CV Template 0018Document1 pageCV Template 0018Rahma idahNo ratings yet

- Market Segmentation Strategic Analysis and Positioning ToolDocument4 pagesMarket Segmentation Strategic Analysis and Positioning ToolshadrickNo ratings yet

- Std. X Ch. 3 Money and Credit WS (21 - 22)Document3 pagesStd. X Ch. 3 Money and Credit WS (21 - 22)YASHVI MODINo ratings yet

- GiftDocument6 pagesGiftalive2flirtNo ratings yet

- Economic Influences On Logistics - Business Case Study 2023Document3 pagesEconomic Influences On Logistics - Business Case Study 2023Bowie LeckieNo ratings yet

- AIS Review QuestionnairesDocument4 pagesAIS Review QuestionnairesKesiah FortunaNo ratings yet

- While It Is True That Increases in Efficiency Generate Productivity IncreasesDocument3 pagesWhile It Is True That Increases in Efficiency Generate Productivity Increasesgod of thunder ThorNo ratings yet

- Capstone Project-Grainger and Bosch: Digital Marketing CampaignDocument25 pagesCapstone Project-Grainger and Bosch: Digital Marketing Campaignk.saikumar100% (1)

- Amul Project Report FinalsssDocument38 pagesAmul Project Report FinalsssPratik Rakesh BakliwalNo ratings yet

- Separate and Consolidated Dayag Part 6Document4 pagesSeparate and Consolidated Dayag Part 6NinaNo ratings yet

- Teaching PowerPoint Slides - Chapter 16Document36 pagesTeaching PowerPoint Slides - Chapter 16Seo ChangBinNo ratings yet

- Model LLP AgreementDocument20 pagesModel LLP AgreementSoumitra Chawathe71% (21)

- Management Information SystemDocument1 pageManagement Information Systemgomsan7No ratings yet

- Causes of Low Literacy Rate in PakistanDocument27 pagesCauses of Low Literacy Rate in PakistanSaba Naeem82% (17)

- Pengaruh Kompensasi Dan MotivasiDocument9 pagesPengaruh Kompensasi Dan Motivasibpbj kabproboNo ratings yet

- Al-Baraka Islamic Bank Internship ReportDocument69 pagesAl-Baraka Islamic Bank Internship Reportbbaahmad89100% (8)

- Listening Test Unit 6Document2 pagesListening Test Unit 6Xuân Bách0% (1)

- What Is Enterprise Agility and Why Is It ImportantDocument4 pagesWhat Is Enterprise Agility and Why Is It ImportantJaveed A. KhanNo ratings yet

- Salem2019 PDFDocument10 pagesSalem2019 PDFRifa ArvandoNo ratings yet

- PMP 2022Document96 pagesPMP 2022Kim Katey KanorNo ratings yet

- Operational Guidelines For Open Banking in NigeriaDocument68 pagesOperational Guidelines For Open Banking in NigeriaCYNTHIA Jumoke100% (1)

- Working Capital Management (Bhavani)Document86 pagesWorking Capital Management (Bhavani)gangatulasiNo ratings yet

- Strategic Analysis and ChoiceDocument13 pagesStrategic Analysis and ChoiceAbhitak MoradabadNo ratings yet

- Midterm International Economics 2023Document4 pagesMidterm International Economics 2023Nhi Nguyễn YếnNo ratings yet

- frdA190220A1421665 PDFDocument2 pagesfrdA190220A1421665 PDFVeritaserumNo ratings yet

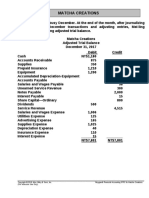

- MC4 Matcha Creations: (For Instructor Use Only)Document2 pagesMC4 Matcha Creations: (For Instructor Use Only)Reza eka PutraNo ratings yet

- PKGS Shipping BillDocument2 pagesPKGS Shipping BillAjay DarlingNo ratings yet

- Strother v. 3464920 Canada Inc.Document2 pagesStrother v. 3464920 Canada Inc.Alice JiangNo ratings yet

- QUIZ1Document1 pageQUIZ1Janysse CalderonNo ratings yet

- HDFC Bank Notice For SettlementDocument1 pageHDFC Bank Notice For Settlementtomarankit44No ratings yet