You might also like

- 09-Marikinacity2013 Part2-Observations and RecommendationsDocument50 pages09-Marikinacity2013 Part2-Observations and RecommendationsLa AlvarezNo ratings yet

- 09-AntiqueProv2021 Part2-Observations and RecommDocument58 pages09-AntiqueProv2021 Part2-Observations and RecommJ JaNo ratings yet

- 09-GuimarasProv2021 Part2-Observations and RecommDocument44 pages09-GuimarasProv2021 Part2-Observations and RecommJ JaNo ratings yet

- 07a ReviewedWithComment BAR2021 Carpenter-Hill KorCity Part1-Notes-to-FS CorrectedDocument8 pages07a ReviewedWithComment BAR2021 Carpenter-Hill KorCity Part1-Notes-to-FS Correctedkipar_16No ratings yet

- Draft AOM - Inventory ReportDocument8 pagesDraft AOM - Inventory ReportGuiller MagsumbolNo ratings yet

- Part Iv - AnnexesDocument21 pagesPart Iv - AnnexesAlicia NhsNo ratings yet

- 09-PPA2015 Part2-Observations and RecommDocument17 pages09-PPA2015 Part2-Observations and RecommJohn Mark RaguindinNo ratings yet

- (All Amounts in Philippine Pesos Unless Otherwise Stated) : Notes To Financial StatementsDocument11 pages(All Amounts in Philippine Pesos Unless Otherwise Stated) : Notes To Financial StatementsErwin LachicaNo ratings yet

- Cash in Bank - Foreign Currency, Savings Account Cash in Bank - Foreign Currency, Time DepositsDocument24 pagesCash in Bank - Foreign Currency, Savings Account Cash in Bank - Foreign Currency, Time DepositsGabriel OrolfoNo ratings yet

- AOM 2019-02 Brgy Look, LapinigDocument4 pagesAOM 2019-02 Brgy Look, LapinigKen BocsNo ratings yet

- COA's Observation and Recommendations (2019 Audit Report On OVP)Document20 pagesCOA's Observation and Recommendations (2019 Audit Report On OVP)VERA FilesNo ratings yet

- V. Financial Feasibility StudyDocument14 pagesV. Financial Feasibility StudyEumar FabruadaNo ratings yet

- PA Budget 2020Document93 pagesPA Budget 2020Zyreen Kate BCNo ratings yet

- Detailed Balance Sheet 2022 1st QuarterDocument3 pagesDetailed Balance Sheet 2022 1st QuarterMikx LeeNo ratings yet

- Statement of Financial Position Ass 1Document10 pagesStatement of Financial Position Ass 1MaitaNo ratings yet

- LBP NO. 3A (Consolidated Programmed Appropriation and Obligation by Object of Expenditure) (2013)Document6 pagesLBP NO. 3A (Consolidated Programmed Appropriation and Obligation by Object of Expenditure) (2013)Bar2012No ratings yet

- LBPF No. 2 - Budget Estimate 2020Document2 pagesLBPF No. 2 - Budget Estimate 2020Bplo CaloocanNo ratings yet

- Poultry 071708Document4 pagesPoultry 071708Clay MaaliwNo ratings yet

- Fs 2015Document15 pagesFs 2015junel pepitoNo ratings yet

- Dmpi - 5 Year Fs Compilation (Updated)Document275 pagesDmpi - 5 Year Fs Compilation (Updated)Precious Santos Corpuz100% (1)

- AOM 2023 001 BahayDocument16 pagesAOM 2023 001 BahayKen BocsNo ratings yet

- Barangay Buenasuerte Notes To Financial StatementsDocument5 pagesBarangay Buenasuerte Notes To Financial StatementsRose Macoy CastilloNo ratings yet

- 6.1 Financial Feasibility Major AssumptionsDocument48 pages6.1 Financial Feasibility Major AssumptionsGizelle Joy Paningbatan MercurioNo ratings yet

- BSG F 12312011Document4 pagesBSG F 12312011Ernest AtonNo ratings yet

- 12 TaclobanCity2018 Part4 Annex 5Document24 pages12 TaclobanCity2018 Part4 Annex 5robert lachicaNo ratings yet

- PP 58 TAX enDocument6 pagesPP 58 TAX enDEODATUSNo ratings yet

- Fs 2016Document15 pagesFs 2016junel pepitoNo ratings yet

- Account Number Account Name Preliminary: Paje 1Document4 pagesAccount Number Account Name Preliminary: Paje 1Maria Fatima AlambraNo ratings yet

- Municipality of Mainit: Notes To Financial StatementsDocument9 pagesMunicipality of Mainit: Notes To Financial StatementsLeo SindolNo ratings yet

- Bicol State College of Applied Sciences and Technology: (With Comparative Figures For CY 2017)Document14 pagesBicol State College of Applied Sciences and Technology: (With Comparative Figures For CY 2017)jaymark camachoNo ratings yet

- BPI - FinaliziranoDocument13 pagesBPI - FinaliziranoSead DzananovicNo ratings yet

- Taxation: MD Mashiur Rahaman Robin KPMG-RRHDocument12 pagesTaxation: MD Mashiur Rahaman Robin KPMG-RRHZidan ZaifNo ratings yet

- Bajrabarahi Sana Krishi Firm Godavari Municipality - 13, LalitpurDocument5 pagesBajrabarahi Sana Krishi Firm Godavari Municipality - 13, LalitpurheroNo ratings yet

- Financial StatementDocument10 pagesFinancial StatementRaven PandacNo ratings yet

- Govacc AnswersDocument24 pagesGovacc AnswersAndrei TimajoNo ratings yet

- Tupol Este 1.docx Landscape - DoneDocument23 pagesTupol Este 1.docx Landscape - DoneJoshua AssinNo ratings yet

- Financia ASPECT - AlarmDocument26 pagesFinancia ASPECT - AlarmEumar FabruadaNo ratings yet

- Inventory Report JUNE 2020Document32 pagesInventory Report JUNE 2020alexisNo ratings yet

- Foreign Service Institute Notes To Financial Statements For The Year Ended December 31, 2017Document14 pagesForeign Service Institute Notes To Financial Statements For The Year Ended December 31, 2017EmosNo ratings yet

- Chapter 5 - Financial Study 5%Document16 pagesChapter 5 - Financial Study 5%Louris NuquiNo ratings yet

- Lect 14TVDocument22 pagesLect 14TVsalman siddiquiNo ratings yet

- ACN II - Home Assignment 1Document8 pagesACN II - Home Assignment 1Mehrab Hussain ZainNo ratings yet

- Piliart Nuts Rizal Street, Sagpon, Daraga, AlbayDocument5 pagesPiliart Nuts Rizal Street, Sagpon, Daraga, AlbayHazel Mae HerreraNo ratings yet

- FSNAV As of JUNE 2023Document96 pagesFSNAV As of JUNE 2023Almarie GarciaNo ratings yet

- COA DECISION NO. 2022-079 Payment of CNA BenefitsDocument13 pagesCOA DECISION NO. 2022-079 Payment of CNA BenefitsLovely MacarioNo ratings yet

- FINANCIAL POSITION June302017Document10 pagesFINANCIAL POSITION June302017Reginald ValenciaNo ratings yet

- Answer Key Quiz 1Document8 pagesAnswer Key Quiz 1Shaira Mae ManalastasNo ratings yet

- Financial MaamDocument7 pagesFinancial MaamFandinola BeverlyNo ratings yet

- 08-WVSU2021 Part1-Financial StatementsDocument15 pages08-WVSU2021 Part1-Financial StatementsMiss_AccountantNo ratings yet

- V!s!t!l!ty Statement of Financial Performance Table 1Document15 pagesV!s!t!l!ty Statement of Financial Performance Table 1Carl Toks Bien InocetoNo ratings yet

- Status of Appropriations, Allotments, Obligations and Balances (Pre-Closing, As of December 2010)Document94 pagesStatus of Appropriations, Allotments, Obligations and Balances (Pre-Closing, As of December 2010)Alexis Cañizar ChuaNo ratings yet

- Financial Aspect FinalDocument12 pagesFinancial Aspect Finalmelvanne tamboboyNo ratings yet

- Province of Antique Unadjusted Trial Balance As of August 2017 All FundsDocument4 pagesProvince of Antique Unadjusted Trial Balance As of August 2017 All FundsDom Minix del RosarioNo ratings yet

- CABWAD Balance Sheet 2019Document5 pagesCABWAD Balance Sheet 2019EunicaNo ratings yet

- IBM Balance SheetDocument7 pagesIBM Balance Sheettahseen7fNo ratings yet

- Surgical, Orthopaedic & Prosthetic Appliances & Supplies World Summary: Market Sector Values & Financials by CountryFrom EverandSurgical, Orthopaedic & Prosthetic Appliances & Supplies World Summary: Market Sector Values & Financials by CountryNo ratings yet

- Sporting & Athletic Goods World Summary: Market Values & Financials by CountryFrom EverandSporting & Athletic Goods World Summary: Market Values & Financials by CountryNo ratings yet

- Navigational, Measuring, Medical & Control Instruments World Summary: Market Values & Financials by CountryFrom EverandNavigational, Measuring, Medical & Control Instruments World Summary: Market Values & Financials by CountryNo ratings yet

- Sporting Goods Store Revenues World Summary: Market Values & Financials by CountryFrom EverandSporting Goods Store Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Marine Machinery, Equipment & Supplies Wholesale Revenues World Summary: Market Values & Financials by CountryFrom EverandMarine Machinery, Equipment & Supplies Wholesale Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- 04-MunCantilan2019 Executive SummaryDocument7 pages04-MunCantilan2019 Executive Summarysandra bolokNo ratings yet

- Executive Summary A. Introduction: Governmen T Equity 42%Document5 pagesExecutive Summary A. Introduction: Governmen T Equity 42%sandra bolokNo ratings yet

- Agency Action Plan and Status of Implementation Audit Observations and RecommendationsDocument1 pageAgency Action Plan and Status of Implementation Audit Observations and Recommendationssandra bolokNo ratings yet

- Part I - Audited Financial StatementsDocument1 pagePart I - Audited Financial Statementssandra bolokNo ratings yet

- 02-MunBarobo2019 Transmittal LettersDocument5 pages02-MunBarobo2019 Transmittal Letterssandra bolokNo ratings yet

- 01-MunCantilan2018 CoverDocument1 page01-MunCantilan2018 Coversandra bolokNo ratings yet

- 03-MunCantilan2019 AAPSIDocument1 page03-MunCantilan2019 AAPSIsandra bolokNo ratings yet

- 02-MunCantilan2019 Transmittal LettersDocument5 pages02-MunCantilan2019 Transmittal Letterssandra bolokNo ratings yet

- 01-MunBarobo2019 CoverDocument1 page01-MunBarobo2019 Coversandra bolokNo ratings yet

- 08-OrmocCity2018 Part1-Notes To FSDocument33 pages08-OrmocCity2018 Part1-Notes To FSsandra bolokNo ratings yet

- Catanauan2019 Audit ReportDocument135 pagesCatanauan2019 Audit Reportsandra bolokNo ratings yet

- Status of Implementation of Prior Years' Unimplemented Audit RecommendationsDocument35 pagesStatus of Implementation of Prior Years' Unimplemented Audit Recommendationssandra bolokNo ratings yet

- 01-RoxasCity2019 Transmittal LettersDocument4 pages01-RoxasCity2019 Transmittal Letterssandra bolokNo ratings yet

- Catanauan2019 Audit ReportDocument135 pagesCatanauan2019 Audit Reportsandra bolokNo ratings yet

- 04-OrmocCity2018 Table of ContentsDocument2 pages04-OrmocCity2018 Table of Contentssandra bolokNo ratings yet

- 11 OrmocCity2018 - Part4 AppendicesDocument36 pages11 OrmocCity2018 - Part4 Appendicessandra bolokNo ratings yet

- 03-OrmocCity2018 Executive SummaryDocument6 pages03-OrmocCity2018 Executive Summarysandra bolokNo ratings yet

- Statement of Financial Position - General Fund: Current AssetsDocument15 pagesStatement of Financial Position - General Fund: Current Assetssandra bolokNo ratings yet

- Independent Auditor's Report: Commission On Audit Office of The Audit Team LeaderDocument2 pagesIndependent Auditor's Report: Commission On Audit Office of The Audit Team Leadersandra bolokNo ratings yet

- 02 OrmocCity2018 CoverDocument1 page02 OrmocCity2018 Coversandra bolokNo ratings yet

- Ormoc City Comparative Statements of Financial Position: Total Current AssetsDocument6 pagesOrmoc City Comparative Statements of Financial Position: Total Current Assetssandra bolokNo ratings yet

- 04-OrmocCity2018 Table of ContentsDocument2 pages04-OrmocCity2018 Table of Contentssandra bolokNo ratings yet

- Commission On Audit: Qualified OpinionDocument2 pagesCommission On Audit: Qualified Opinionsandra bolokNo ratings yet

- Part I - Audited Financial StatementsDocument4 pagesPart I - Audited Financial Statementssandra bolokNo ratings yet

- Part 1 - Financial Statements: Audit RecommendationsDocument1 pagePart 1 - Financial Statements: Audit Recommendationssandra bolokNo ratings yet

- Statement of Financial Position - All Funds: Current AssetsDocument7 pagesStatement of Financial Position - All Funds: Current Assetssandra bolokNo ratings yet

- 10-Compostela2016 Part1-Notes To FSDocument84 pages10-Compostela2016 Part1-Notes To FSsandra bolokNo ratings yet

- Part II - Audit Observations and RecommendationsDocument32 pagesPart II - Audit Observations and Recommendationssandra bolokNo ratings yet

- Annual Audit Report: Republic of The Philippines Commission On Audit Regional Office No. Xi Davao CityDocument1 pageAnnual Audit Report: Republic of The Philippines Commission On Audit Regional Office No. Xi Davao Citysandra bolokNo ratings yet

- Executive Summary: A. Introduction The AgencyDocument5 pagesExecutive Summary: A. Introduction The Agencysandra bolokNo ratings yet

- IAS 16 PPE Lecture Slides (Updated)Document39 pagesIAS 16 PPE Lecture Slides (Updated)Ndila mangalisoNo ratings yet

- ICAB Professional Level Syllabus For Taxation-2 PDFDocument3 pagesICAB Professional Level Syllabus For Taxation-2 PDFnurulaminNo ratings yet

- Annual Neonatal Report 2013Document192 pagesAnnual Neonatal Report 2013Drake ScholasticusNo ratings yet

- Internal Audit ISO 9001:2015 ProcedureDocument4 pagesInternal Audit ISO 9001:2015 ProcedureAzizul Azmi Abdul Rani100% (2)

- Ernst & YoungDocument6 pagesErnst & YoungAnonymous DduElf20ONo ratings yet

- Sabir Commercial Proposal ManagerDocument11 pagesSabir Commercial Proposal ManagerSABIRNo ratings yet

- Sa 315Document3 pagesSa 315shivam wadhwaNo ratings yet

- AUDIT REPORT CompressedDocument8 pagesAUDIT REPORT CompressedSigantengPisanNo ratings yet

- Evan Schwartz ResumeDocument1 pageEvan Schwartz ResumeEvan Efraim SchwartzNo ratings yet

- Role of Internal AuditorDocument2 pagesRole of Internal AuditorArgie Adduru100% (1)

- Acceptance of Evidence Based On The Results of Probability SamplingDocument6 pagesAcceptance of Evidence Based On The Results of Probability SamplingdgkmurtiNo ratings yet

- Bukti Audit-Prosedur Audit-Kertas KerjaDocument47 pagesBukti Audit-Prosedur Audit-Kertas KerjagandhunkNo ratings yet

- Internal Audit MethodologyDocument34 pagesInternal Audit MethodologyChris seyNo ratings yet

- Computer Aided Audit ToolsDocument8 pagesComputer Aided Audit ToolsRahul GargNo ratings yet

- Philippine Taxation Encyclopedia Third Release 2019 - 01Document173 pagesPhilippine Taxation Encyclopedia Third Release 2019 - 01Patricia Arpilleda100% (1)

- Mock Departmentals COSTQDocument7 pagesMock Departmentals COSTQHannah Joyce MirandaNo ratings yet

- AT QuizDocument15 pagesAT QuizClydeNo ratings yet

- Sample of Receipt & Payment AccountDocument19 pagesSample of Receipt & Payment AccountIbrahim Sjah PaduNo ratings yet

- Chapter 1 Nature and Scope of The NGASDocument3 pagesChapter 1 Nature and Scope of The NGASShaira BugayongNo ratings yet

- Soneri Bank A-Report 2013 FinalDocument144 pagesSoneri Bank A-Report 2013 FinalMuqaddas IsrarNo ratings yet

- CACC 521 W20 Outline 2020Document8 pagesCACC 521 W20 Outline 2020helloNo ratings yet

- At (3) - Auditor'S Responsibility: Employee Fraud. It Involves The Theft of AnDocument1 pageAt (3) - Auditor'S Responsibility: Employee Fraud. It Involves The Theft of AnPau SantosNo ratings yet

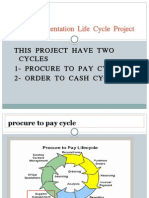

- Full Implementation Life Cycle ProjectDocument27 pagesFull Implementation Life Cycle ProjectSaif AhmedNo ratings yet

- OPCRF LaburDocument7 pagesOPCRF LaburDennis Corsino RamirezNo ratings yet

- Superior University: Advance Auditing Mid AssignmentDocument34 pagesSuperior University: Advance Auditing Mid AssignmentMirza Ehsan Ullah MughalNo ratings yet

- Related Party Transactions - ReadDocument86 pagesRelated Party Transactions - ReadUroobaShiekhNo ratings yet

- Pragati Life Insurance Ltd. 26.08.2020 PDFDocument122 pagesPragati Life Insurance Ltd. 26.08.2020 PDFRo B In IINo ratings yet

- Knowledge ReportDocument15 pagesKnowledge ReportarsenalmanikandanNo ratings yet

- Group Reflection Paper On EthicsDocument4 pagesGroup Reflection Paper On EthicsVan TisbeNo ratings yet

- Renovation, Modernization and Life Extension of Power PlantsDocument24 pagesRenovation, Modernization and Life Extension of Power PlantskrcdewanewNo ratings yet