You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5810)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Sorp 4Document13 pagesSorp 4flippermiloNo ratings yet

- KPCB Internet Trends 2012Document112 pagesKPCB Internet Trends 2012Kleiner Perkins Caufield & Byers100% (14)

- Workbook From Desktop Lawyer Generic Lawyer (2012!06!06 09-22-58 UTC)Document691 pagesWorkbook From Desktop Lawyer Generic Lawyer (2012!06!06 09-22-58 UTC)Armond Trakarian100% (2)

- Bill of Supply: For Any Queries On This Bill Please Contact MSEDCL CallDocument1 pageBill of Supply: For Any Queries On This Bill Please Contact MSEDCL CallrahulNo ratings yet

- Heidrun Ihechiloru Egbuta: 7 Alhaja Adetola Street, Apapa, LagosDocument75 pagesHeidrun Ihechiloru Egbuta: 7 Alhaja Adetola Street, Apapa, LagosheidyegbutaNo ratings yet

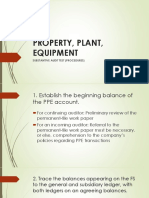

- Property, Plant, Equipment: Substantive Audit Test (Procedures)Document10 pagesProperty, Plant, Equipment: Substantive Audit Test (Procedures)jexNo ratings yet

- 05a Aravind Eye Hospital, Madurai, IndiaDocument4 pages05a Aravind Eye Hospital, Madurai, IndiaSubhadra HaribabuNo ratings yet

- Asis Mo 6: Supply Chain ManagementDocument8 pagesAsis Mo 6: Supply Chain ManagementTalitha GranitaNo ratings yet

- RIU HotelsDocument3 pagesRIU HotelszakaNo ratings yet

- Map OF ELANTE MALLDocument1 pageMap OF ELANTE MALLday nightNo ratings yet

- Online Payment PortalDocument2 pagesOnline Payment PortalArjunNo ratings yet

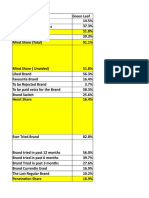

- Brand Health Analysis TemplateDocument4 pagesBrand Health Analysis Templateanon_493704527No ratings yet

- PhilAmLife V SEc of FinanceDocument2 pagesPhilAmLife V SEc of FinanceOro Chamber100% (2)

- Ramadan Rate Offer Far-East 2023Document1 pageRamadan Rate Offer Far-East 2023Ryan DarmawanNo ratings yet

- Machine InformationDocument21 pagesMachine InformationSk KalamNo ratings yet

- Alis Flow ChartDocument1 pageAlis Flow ChartMahesh KumarNo ratings yet

- Jammu and Kashmir Bank Clerk Prelims Model Paper 2: English LanguageDocument26 pagesJammu and Kashmir Bank Clerk Prelims Model Paper 2: English LanguageShubham VermaNo ratings yet

- Leasing Presentation of Ashima Mall BhopalDocument38 pagesLeasing Presentation of Ashima Mall BhopalVipin 16No ratings yet

- LaporanDocument55 pagesLaporanArisHadiansyahNo ratings yet

- 10 Contracts For Your Next Agile Software ProjectDocument12 pages10 Contracts For Your Next Agile Software ProjectSharpman Fine Fikky OtunNo ratings yet

- Power IndustryDocument11 pagesPower IndustryMinesh Chand MeenaNo ratings yet

- Assignment 1 (Fiscal Deficit and Trade Balance)Document5 pagesAssignment 1 (Fiscal Deficit and Trade Balance)Ansab QureshiNo ratings yet

- Geochemical Methods in Mineral ExplorationDocument22 pagesGeochemical Methods in Mineral ExplorationSandeep GawandeNo ratings yet

- SL - No. Employer Code Employer Name Number of Employees Employees' State Insurance CorporationDocument204 pagesSL - No. Employer Code Employer Name Number of Employees Employees' State Insurance Corporationraju mudigondaNo ratings yet

- Metro Bank PLC ArticleDocument2 pagesMetro Bank PLC ArticleDave LiNo ratings yet

- Audited Financial StatementDocument17 pagesAudited Financial StatementVictor BiacoloNo ratings yet

- Course Work On SMEDocument9 pagesCourse Work On SMEPett PeeveNo ratings yet

- International Business Machines Corporation: Type Traded AsDocument4 pagesInternational Business Machines Corporation: Type Traded AsSoyi PsNo ratings yet

- FT 20141208Document48 pagesFT 20141208NastyaKalesnikovaNo ratings yet

- The Economic Impact of COVID 19 With Special Reference To IndiaDocument8 pagesThe Economic Impact of COVID 19 With Special Reference To IndiaAnushka Jaiswal100% (1)