You might also like

- Shipments To Branch Above CostDocument4 pagesShipments To Branch Above CostJohnmichael Coroza0% (1)

- Home Office and Branch HandoutsDocument4 pagesHome Office and Branch HandoutsbangtansonyeondaNo ratings yet

- Advanced Accounting Home Office, Branch and Agency TransactionsDocument7 pagesAdvanced Accounting Home Office, Branch and Agency TransactionsMajoy Bantoc100% (1)

- Home Office and Branch AccountingDocument4 pagesHome Office and Branch AccountingMaurice AgbayaniNo ratings yet

- AGONCILLO LORIELYN HomeOfficeQuestionsDocument13 pagesAGONCILLO LORIELYN HomeOfficeQuestionsLara FloresNo ratings yet

- Home Office and Branch AccountingDocument3 pagesHome Office and Branch AccountingPrecious Ivy Fernandez100% (1)

- Acctg 10 - Final ExamDocument6 pagesAcctg 10 - Final ExamNANNo ratings yet

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument15 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionErwin Labayog MedinaNo ratings yet

- Midterm Exam No. 2Document1 pageMidterm Exam No. 2Anie MartinezNo ratings yet

- Installment Sales MethodDocument25 pagesInstallment Sales MethodAngerica BongalingNo ratings yet

- Consolidated Net IncomeDocument1 pageConsolidated Net IncomePJ PoliranNo ratings yet

- Activity Task Business CombinationDocument7 pagesActivity Task Business CombinationCasper John Nanas MuñozNo ratings yet

- Home Office IntegDocument9 pagesHome Office IntegReshielyn Vee Entrampas LopezNo ratings yet

- Advanced Accounting - Volume 1Document4 pagesAdvanced Accounting - Volume 1Erica CaliuagNo ratings yet

- TB ch01 9eDocument12 pagesTB ch01 9eRadizaJisiNo ratings yet

- Quiz 2 - Accounting ProcessDocument3 pagesQuiz 2 - Accounting ProcessPrincess NozalNo ratings yet

- Branches and Agencies - OdtDocument9 pagesBranches and Agencies - OdtEunice BernalNo ratings yet

- Chapter 13 - Multiple Choices Problem and Theries KeyDocument15 pagesChapter 13 - Multiple Choices Problem and Theries KeyKryscel ManansalaNo ratings yet

- Solution Chapter 8 Rev FinalDocument20 pagesSolution Chapter 8 Rev FinalJonalyn SaloNo ratings yet

- Audit of ReceivablesDocument29 pagesAudit of ReceivablesJoseph SalidoNo ratings yet

- Consolidated BS - Date of AcquisitionDocument2 pagesConsolidated BS - Date of AcquisitionKharen Valdez0% (1)

- Business Combination and Consolidated FS Part 1Document6 pagesBusiness Combination and Consolidated FS Part 1markNo ratings yet

- Home Office BranchDocument5 pagesHome Office BranchMikaella SarmientoNo ratings yet

- QuizDocument11 pagesQuizJuan Rafael FernandezNo ratings yet

- Activity 1 Home Office and Branch Accounting - General ProceduresDocument4 pagesActivity 1 Home Office and Branch Accounting - General ProceduresDaenielle EspinozaNo ratings yet

- Quiz Bee4thyrDocument5 pagesQuiz Bee4thyrlalala010899No ratings yet

- Activity Audit in InventoryDocument4 pagesActivity Audit in InventoryKizzea Bianca GadotNo ratings yet

- 04 CVP AnswerDocument36 pages04 CVP AnswerjoyjoyjoyNo ratings yet

- Home Office and Branch AccountingDocument2 pagesHome Office and Branch AccountingJack Herer100% (1)

- Auditing Theory - Internal Control ConsiderationDocument11 pagesAuditing Theory - Internal Control ConsiderationNeil BacaniNo ratings yet

- Exercise AC 518 2nd Sem 2016Document2 pagesExercise AC 518 2nd Sem 2016RALLISONNo ratings yet

- Advanced Accounting PDocument4 pagesAdvanced Accounting PMaurice Agbayani100% (1)

- M3 Assignment Internal Control Group 9 AUDIT SPECIAL INDUSTRYDocument5 pagesM3 Assignment Internal Control Group 9 AUDIT SPECIAL INDUSTRYReginald ValenciaNo ratings yet

- AFAR Business Combination 1Document12 pagesAFAR Business Combination 1Herwin Mae BoclarasNo ratings yet

- P2 - Installment Sales, O2018 AUFDocument5 pagesP2 - Installment Sales, O2018 AUFedsNo ratings yet

- Chapter 4Document17 pagesChapter 4Mary MarieNo ratings yet

- C Par First Pre Board 2008 ADocument17 pagesC Par First Pre Board 2008 AJaylord Pido100% (1)

- Von Sanchez ExpressDocument12 pagesVon Sanchez ExpressJoey WassigNo ratings yet

- BAFINAR Quiz 6 R FinalDocument4 pagesBAFINAR Quiz 6 R FinalJemNo ratings yet

- Mid PS3Document8 pagesMid PS3heyNo ratings yet

- StudyDocument10 pagesStudyirahQNo ratings yet

- Mga Dambieee!!!!: Complete Answer Pleaseee. Thank Youuu NO. Questions Answer 1 Answer 2 If Unsure Answer 1Document12 pagesMga Dambieee!!!!: Complete Answer Pleaseee. Thank Youuu NO. Questions Answer 1 Answer 2 If Unsure Answer 1Hannah Jane UmbayNo ratings yet

- Installment Sales - PretestDocument2 pagesInstallment Sales - PretestCattleyaNo ratings yet

- Chapter 16 - Bus Com Part 3 - Afar Part 2Document5 pagesChapter 16 - Bus Com Part 3 - Afar Part 2Emman ElagoNo ratings yet

- Cpa Review School of The Philippines: (P1,832,400-P598,400-P19,200-P180,000-P65,000-P73,000-P178,200)Document10 pagesCpa Review School of The Philippines: (P1,832,400-P598,400-P19,200-P180,000-P65,000-P73,000-P178,200)RIZA LUMAADNo ratings yet

- 09 X07 C Responsibility Accounting and TP Variable Costing & Segmented ReportingDocument8 pages09 X07 C Responsibility Accounting and TP Variable Costing & Segmented ReportingJonailyn YR PeraltaNo ratings yet

- Closing Entries - Branchbooks: (Branch Books) Home OfficeDocument2 pagesClosing Entries - Branchbooks: (Branch Books) Home OfficeUnknown 01No ratings yet

- Coursehero 12Document2 pagesCoursehero 12nhbNo ratings yet

- Palmones, Jayhan Grace M. QuizDocument6 pagesPalmones, Jayhan Grace M. QuizjayhandarwinNo ratings yet

- ACC16 - HO 2 Installment Sales 11172014Document7 pagesACC16 - HO 2 Installment Sales 11172014Marvin James Cho0% (2)

- Accounting 7an Business CombinationDocument8 pagesAccounting 7an Business CombinationLabLab ChattoNo ratings yet

- Home Office, Agency and Branch AccountingDocument17 pagesHome Office, Agency and Branch AccountingPaupauNo ratings yet

- Seatwork Income MaDocument3 pagesSeatwork Income MaJoyce Ann Agdippa Barcelona0% (1)

- Exercises Absorption and Variable CostingPAUL ANTHONY DE JESUSDocument4 pagesExercises Absorption and Variable CostingPAUL ANTHONY DE JESUSMeng DanNo ratings yet

- Finals Quiz 2 Buscom Version 2Document3 pagesFinals Quiz 2 Buscom Version 2Kristina Angelina ReyesNo ratings yet

- HOBA - SeatworkDocument2 pagesHOBA - Seatworkahyenn cabelloNo ratings yet

- HOBA - Finals QuizDocument13 pagesHOBA - Finals QuizRujean Salar AltejarNo ratings yet

- ExerciseDocument4 pagesExerciseMae RxNo ratings yet

- Lesson 2 Home and Branch Accounting - Special ProblemsDocument3 pagesLesson 2 Home and Branch Accounting - Special ProblemsAndy LaluNo ratings yet

- Home Office and Branch Accounting H2Document3 pagesHome Office and Branch Accounting H2Nye NyeNo ratings yet

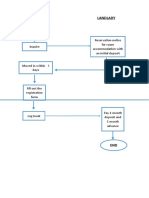

- FlowchartDocument1 pageFlowchartKathleeneNo ratings yet

- EditedDocument58 pagesEditedKathleeneNo ratings yet

- Vat Healthcare GCC Dec2016 PDFDocument2 pagesVat Healthcare GCC Dec2016 PDFJoe Marie Peter BaddongonNo ratings yet

- Financial Assumptions: RevenueDocument12 pagesFinancial Assumptions: RevenueKathleeneNo ratings yet

- 10 Reasons Why Studying Is HardDocument2 pages10 Reasons Why Studying Is HardKathleeneNo ratings yet

- HANDOUTS AUDITORs ResponsibilityDocument3 pagesHANDOUTS AUDITORs ResponsibilityKathleeneNo ratings yet

- RMYC Tax Case 2019 R3Document2 pagesRMYC Tax Case 2019 R3KathleeneNo ratings yet

- Simple Stress: Mechanics of Deformable BodiesDocument19 pagesSimple Stress: Mechanics of Deformable BodiesKathleeneNo ratings yet

- Shear Stress: Mechanics of Deformable BodiesDocument18 pagesShear Stress: Mechanics of Deformable BodiesKathleeneNo ratings yet

- Home Office and Branch Accounting (HOBA) With Sample Problems, Solutions and ExplanationsDocument16 pagesHome Office and Branch Accounting (HOBA) With Sample Problems, Solutions and ExplanationsKathleene50% (2)

- Tax Tarification LawDocument10 pagesTax Tarification LawKathleene100% (2)

- Accounting Ratios FormulasDocument3 pagesAccounting Ratios FormulasEshan BhattNo ratings yet

- SyllabusDocument5 pagesSyllabusBalbeer SinghNo ratings yet

- Fico TicketsDocument29 pagesFico TicketsVikas MNo ratings yet

- Managing Member - Tim Eriksen Eriksen Capital Management, LLC 567 Wildrose Cir., Lynden, WA 98264Document7 pagesManaging Member - Tim Eriksen Eriksen Capital Management, LLC 567 Wildrose Cir., Lynden, WA 98264Matt EbrahimiNo ratings yet

- Lae ReservingDocument5 pagesLae ReservingEsra Gunes YildizNo ratings yet

- Homework On Current Liabilities 1st Term Sy2018-2019Document4 pagesHomework On Current Liabilities 1st Term Sy2018-2019RedNo ratings yet

- Operations Management PS5Document5 pagesOperations Management PS5Vishal BhagiaNo ratings yet

- Book Building ProcessDocument3 pagesBook Building ProcessgiteshNo ratings yet

- AFA - Earnings Drivers EtcDocument24 pagesAFA - Earnings Drivers EtcHYUN JUNG KIMNo ratings yet

- In God We Trust - Multiple ChoiceDocument13 pagesIn God We Trust - Multiple ChoiceNevan NovaNo ratings yet

- Rate of ReturnDocument38 pagesRate of ReturnPraz AarashNo ratings yet

- WRAP Thesis Lamusse 1982Document457 pagesWRAP Thesis Lamusse 1982Vishal RamlallNo ratings yet

- Presentation On Elasticity of DemandDocument15 pagesPresentation On Elasticity of DemandsoftcoreNo ratings yet

- International Strategic Alliances: After Studying This Chapter, Students Should Be Able ToDocument19 pagesInternational Strategic Alliances: After Studying This Chapter, Students Should Be Able Toaidatabah100% (1)

- Problem 4Document3 pagesProblem 4Rua ConNo ratings yet

- Quiz 7 - BTX 113Document5 pagesQuiz 7 - BTX 113Rae Vincent Revilla100% (3)

- Assignment 2Document8 pagesAssignment 2Krithardh ChunchuNo ratings yet

- Hunger Banquet ScriptDocument10 pagesHunger Banquet ScriptThe Bean CounterNo ratings yet

- Explanatory Memorandum SSDocument23 pagesExplanatory Memorandum SSkalluvarmaNo ratings yet

- Littlefield Game 2 OverviewDocument3 pagesLittlefield Game 2 OverviewRichard Joshua SNo ratings yet

- ShortingDocument25 pagesShortingTony NguyenNo ratings yet

- Unit 3Document21 pagesUnit 3InduSaran AttadaNo ratings yet

- Touchpoints in CRM of LICDocument7 pagesTouchpoints in CRM of LICShahnwaz AlamNo ratings yet

- Friendley S Miniature Golf and Driving Range Inc Was Opened OnDocument1 pageFriendley S Miniature Golf and Driving Range Inc Was Opened Ontrilocksp SinghNo ratings yet

- Basic Option Pricing by BittmanDocument48 pagesBasic Option Pricing by BittmanJunedi dNo ratings yet

- David Wessels - Corporate Strategy and ValuationDocument26 pagesDavid Wessels - Corporate Strategy and Valuationesjacobsen100% (1)

- Pa Aaaaa SssDocument34 pagesPa Aaaaa Ssspeter NHNo ratings yet

- Functional Areas of KCMMFDocument11 pagesFunctional Areas of KCMMFChaithra ThampanNo ratings yet

- MyNotesOnCNBCSoFar 2016Document38 pagesMyNotesOnCNBCSoFar 2016Tony C.No ratings yet

- Hac 1001 NotesDocument56 pagesHac 1001 NotesMarlin MerikanNo ratings yet