You might also like

- Business Plan Checklist: Plan your way to business successFrom EverandBusiness Plan Checklist: Plan your way to business successRating: 5 out of 5 stars5/5 (1)

- Business Plan Management ConceptsDocument6 pagesBusiness Plan Management ConceptsPrashant KumarNo ratings yet

- Plan Your EnterpriseDocument9 pagesPlan Your EnterpriseJerwin SamsonNo ratings yet

- FinalDocument13 pagesFinalNishuNo ratings yet

- Sterling Institute of Management StudiesDocument29 pagesSterling Institute of Management StudiesPraNita AmbavaneNo ratings yet

- Business Plan Unit 9Document6 pagesBusiness Plan Unit 9Disha JainNo ratings yet

- Financial Planning and ForecastingDocument15 pagesFinancial Planning and Forecastingalkanm750100% (1)

- H9 Master Budget and ForecastingDocument17 pagesH9 Master Budget and ForecastingGodwin Jil CabotajeNo ratings yet

- Business Plan FormatDocument5 pagesBusiness Plan FormatNimmy MathewNo ratings yet

- Investment Appraisal in BusinessDocument13 pagesInvestment Appraisal in BusinessAsimali AsimaliNo ratings yet

- Module 2 Smart Task 2Document3 pagesModule 2 Smart Task 2YASHASVI SHARMANo ratings yet

- Build Business Plan SuccessDocument21 pagesBuild Business Plan SuccessFatimah Binte AtiqNo ratings yet

- Lecture 12 EntrepreneurshipDocument23 pagesLecture 12 EntrepreneurshipKomal RahimNo ratings yet

- Financial Planning and ForcastingDocument34 pagesFinancial Planning and ForcastingFarhan JagirdarNo ratings yet

- Chapter 8 IzmerDocument20 pagesChapter 8 IzmerMOHAMAD NAIM FAHMI BIN MOHAMAD YASIR STUDENTNo ratings yet

- Financial ManagementDocument26 pagesFinancial ManagementHILLARY SHINGIRAI MAPIRANo ratings yet

- Financial Projections and Key Metrics for MBLDocument6 pagesFinancial Projections and Key Metrics for MBLGohar AfshanNo ratings yet

- The Business PlanDocument42 pagesThe Business PlanSavant83% (12)

- Planning and Working Capital Management Part 1Document31 pagesPlanning and Working Capital Management Part 1Michelle RotairoNo ratings yet

- Management Accounting NotesDocument7 pagesManagement Accounting NotesMuhammad Akmal HossainNo ratings yet

- Cost Accounting: Chapter 8 Solutions, 4eDocument85 pagesCost Accounting: Chapter 8 Solutions, 4eaorlaan50% (2)

- The Financial Plan: Serjoe Orven Gutierrez - Mmed ReporterDocument41 pagesThe Financial Plan: Serjoe Orven Gutierrez - Mmed ReporterSerjoe GutierrezNo ratings yet

- Assignment 3 - 18 - ENG - 091Document7 pagesAssignment 3 - 18 - ENG - 091ravindu nayanajithNo ratings yet

- Chapter 3 Developing A Business Plan PDFDocument21 pagesChapter 3 Developing A Business Plan PDFAdrian Singson0% (2)

- Writing A Business Plan: How To Win Backing To Start Up or Grow Your Business (Bahasa Indonesia)Document79 pagesWriting A Business Plan: How To Win Backing To Start Up or Grow Your Business (Bahasa Indonesia)MiraNo ratings yet

- Financial Planning Tools and Concepts ExplainedDocument17 pagesFinancial Planning Tools and Concepts ExplainedLenard TaberdoNo ratings yet

- Lesson 1 EntrepreneurshipDocument28 pagesLesson 1 EntrepreneurshipMia Rose E. CasusulaNo ratings yet

- Business Finance: 1 Quarter Lesson 3: Financial Planning ProcessDocument6 pagesBusiness Finance: 1 Quarter Lesson 3: Financial Planning ProcessReshaNo ratings yet

- Financial AnalysisDocument17 pagesFinancial AnalysistonyNo ratings yet

- Financial Planning Guide for Small BusinessesDocument23 pagesFinancial Planning Guide for Small BusinessesHassan JulkipliNo ratings yet

- Met Mba 2011 - 2013: Preparation of A Budget For Mba Programme (Case Study On Mba Student at Met Iom)Document18 pagesMet Mba 2011 - 2013: Preparation of A Budget For Mba Programme (Case Study On Mba Student at Met Iom)shashankchhedaNo ratings yet

- Ed - 5Document30 pagesEd - 5CA Arena TumkurNo ratings yet

- Entrepreneurship CH 7Document21 pagesEntrepreneurship CH 7Wiz Nati XvNo ratings yet

- Financial Planning PresentationDocument27 pagesFinancial Planning PresentationSeidu AbdullahiNo ratings yet

- FP&A Interview Questions and AnswersDocument7 pagesFP&A Interview Questions and Answershrithikoswal1603No ratings yet

- Corporate Finance ProjectDocument31 pagesCorporate Finance ProjectKrishnendu SahaNo ratings yet

- Lecture 3 - Applying For FinanceDocument22 pagesLecture 3 - Applying For FinanceJad ZoghaibNo ratings yet

- Business Plan: International Philippine School in Jeddah Senior High School DepartmentDocument29 pagesBusiness Plan: International Philippine School in Jeddah Senior High School DepartmentDanikkaGayleBonoanNo ratings yet

- Financial Reporting Thesis PDFDocument6 pagesFinancial Reporting Thesis PDFUK100% (2)

- A Guide to Writing Effective Business PlansDocument6 pagesA Guide to Writing Effective Business Plansugochi ajaraonyeNo ratings yet

- FINANCIAL FORCASTING REPORTDocument9 pagesFINANCIAL FORCASTING REPORTHannah Lucenio BaringNo ratings yet

- PRATICAL NO 14 EDP HKKDocument5 pagesPRATICAL NO 14 EDP HKKHKK 169No ratings yet

- Parts of Feasibility StudyDocument5 pagesParts of Feasibility StudyMark LoraNo ratings yet

- Philippine Christian University MBA Program Income Statement ForecastDocument10 pagesPhilippine Christian University MBA Program Income Statement ForecastKatrizia FauniNo ratings yet

- Manage Finances Bsbfim 601 Chiradet Thepwong 14497: ASSESSMENT 3 (Online Assessment) - Research and QuestioningDocument11 pagesManage Finances Bsbfim 601 Chiradet Thepwong 14497: ASSESSMENT 3 (Online Assessment) - Research and Questioningnatty60% (5)

- Main Components of A Business PlanDocument8 pagesMain Components of A Business PlanReynhard DaleNo ratings yet

- Financial Planning ToolDocument125 pagesFinancial Planning ToolKareen Tapia PublicoNo ratings yet

- Small Business Owner S HandbookDocument18 pagesSmall Business Owner S HandbookAla'a AbdullaNo ratings yet

- CIMA Financial Information in Decision MakingDocument4 pagesCIMA Financial Information in Decision MakingAdil MahmudNo ratings yet

- School of Management Studies Business Plan GuideDocument19 pagesSchool of Management Studies Business Plan GuideStephen NNo ratings yet

- Business PlanningDocument23 pagesBusiness Planningramadhanamos620No ratings yet

- Chapter 8 COMM 320Document10 pagesChapter 8 COMM 320Erick GellisNo ratings yet

- Financial Forecasting 1Document44 pagesFinancial Forecasting 1ABOOBAKKERNo ratings yet

- Ecommerce: Business PlanDocument20 pagesEcommerce: Business PlanJoseph ContehNo ratings yet

- Final Exam Doc Cel SaberonDocument4 pagesFinal Exam Doc Cel SaberonAnonymous iScW9lNo ratings yet

- Understanding the Importance of Financial Planning for BusinessesDocument98 pagesUnderstanding the Importance of Financial Planning for Businessesrey mark hamacNo ratings yet

- Handout EntrepDocument6 pagesHandout EntrepNorsaifah AbduljalalNo ratings yet

- Financial Projections Guide Business SuccessDocument9 pagesFinancial Projections Guide Business SuccessIndra Kusuma AdiNo ratings yet

- Management Accounting - HCA16ge - Ch6Document76 pagesManagement Accounting - HCA16ge - Ch6Corliss Ko100% (3)

- Hca16ge Ch06 SMDocument76 pagesHca16ge Ch06 SMAmanda GuanNo ratings yet

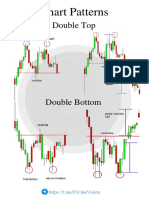

- Double Top: Chart PatternsDocument11 pagesDouble Top: Chart PatternsKrunal Jain100% (1)

- Level 2 Unit 08 Importance of Business PlansDocument3 pagesLevel 2 Unit 08 Importance of Business PlansAliceNo ratings yet

- Importance of Business Planning in An Environment Lacking Economic PredictabilityDocument6 pagesImportance of Business Planning in An Environment Lacking Economic PredictabilityAliceNo ratings yet

- Level 2 Unit 08 Importance of Business PlansDocument3 pagesLevel 2 Unit 08 Importance of Business PlansAliceNo ratings yet

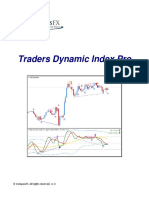

- TDI Pro User ManualDocument36 pagesTDI Pro User ManualMichael Mario80% (5)

- TDI Indicator For Mobile PDFDocument2 pagesTDI Indicator For Mobile PDFAbrudean Paul100% (1)

- Analitical Exsp 121Document7 pagesAnalitical Exsp 121Seya ArfNo ratings yet

- CRED: India's Leading FinTech Rewarding Credit Card Bill PaymentsDocument3 pagesCRED: India's Leading FinTech Rewarding Credit Card Bill PaymentsyogeshNo ratings yet

- Book My ShowDocument18 pagesBook My ShowakhilmidhaNo ratings yet

- I190378914 1Document6 pagesI190378914 1Appie KoekangeNo ratings yet

- AFR Stockland Exits Retirement Living With $987m Sale To EQT, Profit RisesDocument4 pagesAFR Stockland Exits Retirement Living With $987m Sale To EQT, Profit Risesroshan24No ratings yet

- F 09420010120134019 PP T 06Document21 pagesF 09420010120134019 PP T 06Morita MichieNo ratings yet

- List of Project Topics Capital Markets and Securities LawDocument4 pagesList of Project Topics Capital Markets and Securities Lawsonu peterNo ratings yet

- Introduction To Options Trading de Weert PDF and Free Nifty Option Tips TodayDocument1 pageIntroduction To Options Trading de Weert PDF and Free Nifty Option Tips TodayAnonymous wUtTgUNo ratings yet

- Business Finance Module 5Document3 pagesBusiness Finance Module 5acegutierrezNo ratings yet

- Top Ten Advanced Indicators With Tom Long TomLongDocument43 pagesTop Ten Advanced Indicators With Tom Long TomLongSenthil Kumaran100% (1)

- Jawaban UTS Manajemen KeuanganDocument16 pagesJawaban UTS Manajemen KeuanganMikhail BarenovNo ratings yet

- Jollibee Foods CorporationDocument7 pagesJollibee Foods Corporationgiadcunha88% (8)

- (MR Paul A Taylor) Consolidated Financial Reportin PDFDocument385 pages(MR Paul A Taylor) Consolidated Financial Reportin PDFMarcel Coșcodan100% (1)

- Exam Passing Strategy ACHSDocument16 pagesExam Passing Strategy ACHSnv_FrancisNo ratings yet

- A MiDocument608 pagesA Mimasmid100% (2)

- Insurance Pricing: Ajitav AcharyaDocument13 pagesInsurance Pricing: Ajitav AcharyaAJITAV SILUNo ratings yet

- Fast Graph Howtoknowpart1Document9 pagesFast Graph Howtoknowpart1Sww WisdomNo ratings yet

- BA 5301 - IBM - Theory Assistance - 5 UnitsDocument20 pagesBA 5301 - IBM - Theory Assistance - 5 UnitsSelvaraj VijayNo ratings yet

- Nutresa Nov 3Document13 pagesNutresa Nov 3SemanaNo ratings yet

- Eeco Chapter 2Document3 pagesEeco Chapter 2Erika Herrera0% (2)

- Retail Strategies: Ahold vs Walmart & CarrefourDocument7 pagesRetail Strategies: Ahold vs Walmart & CarrefourrajdeeplahaNo ratings yet

- Peer Mentoring PostTestDocument7 pagesPeer Mentoring PostTestronnelNo ratings yet

- Inside Job - Movie Review (The Story of Global Recession 2008) PDFDocument21 pagesInside Job - Movie Review (The Story of Global Recession 2008) PDFVALLIAPPAN.P100% (2)

- Ledger 3Document138 pagesLedger 3AWNo ratings yet

- TYBBI Security Anal 7.xlxsDocument4 pagesTYBBI Security Anal 7.xlxsEsha JaiswalNo ratings yet

- VEP - A.T. Kearney 2003Document48 pagesVEP - A.T. Kearney 2003punit_sonikaNo ratings yet

- Provisional 2014 15Document29 pagesProvisional 2014 15maheshfbNo ratings yet

- BPC 10.0 Planning ScenariosDocument16 pagesBPC 10.0 Planning ScenariosDinakaran KailasamNo ratings yet

- Kepler Nova RETDocument2 pagesKepler Nova RETKepler NovaNo ratings yet

- Growel Guide To Dairy Farm Business Management AnalysisDocument32 pagesGrowel Guide To Dairy Farm Business Management AnalysisGrowel Agrovet Private Limited.No ratings yet