You might also like

- White Lies - Core RulebookDocument136 pagesWhite Lies - Core RulebookThiago AlmeidaNo ratings yet

- Injectomat Agilia IS - Spare PartsDocument18 pagesInjectomat Agilia IS - Spare PartsNguyễn Phúc NhưNo ratings yet

- BARACARBDocument2 pagesBARACARBYudha Satria50% (2)

- Bronchiolitis A Practical Approach For The General RadiologistDocument42 pagesBronchiolitis A Practical Approach For The General RadiologistTara NareswariNo ratings yet

- Beneficiation of Cassiterite From Primary Tin OresDocument11 pagesBeneficiation of Cassiterite From Primary Tin OresSULMAGNo ratings yet

- 3rd Periodic Test in English4Document7 pages3rd Periodic Test in English4Santa Dela Cruz Naluz100% (1)

- Water Spray Nozzle: Fire Fighting Equipment Data SheetDocument7 pagesWater Spray Nozzle: Fire Fighting Equipment Data SheetJosef MadronaNo ratings yet

- Solvent Extraction: Please Submit Question 4 For MarkingDocument3 pagesSolvent Extraction: Please Submit Question 4 For MarkingThembi Matebula100% (1)

- ISO 14000 - WikipediaDocument5 pagesISO 14000 - WikipediaalexokorieNo ratings yet

- JD Edwards World Forecasting Guide Forecast Calculation ExamplesDocument26 pagesJD Edwards World Forecasting Guide Forecast Calculation ExamplesNitaNo ratings yet

- Forecasting Excel FormulaDocument2 pagesForecasting Excel FormulaCarlo Niño GedoriaNo ratings yet

- Monthly Irradiation Data: PVGIS-5 Geo-Temporal Irradiation DatabaseDocument1 pageMonthly Irradiation Data: PVGIS-5 Geo-Temporal Irradiation DatabaseneymarronNo ratings yet

- Marv HarnishfegerDocument5 pagesMarv Harnishfegerdember alexis palacios abarcaNo ratings yet

- Case Study Test CA 2 No AnswearDocument3 pagesCase Study Test CA 2 No Answear722h0159No ratings yet

- FuelpricesHistory Sept 2021Document15 pagesFuelpricesHistory Sept 2021Paul LynchNo ratings yet

- 2022-2023 Overall Approval Rate for EB1ADocument1 page2022-2023 Overall Approval Rate for EB1AmixarimNo ratings yet

- Three Period Moving Average ForecastingDocument6 pagesThree Period Moving Average ForecastingnomanNo ratings yet

- Gazette No. 2 of 2002Document2 pagesGazette No. 2 of 2002cybertech34 HDNo ratings yet

- Mariano Marcos State University Case StudyDocument13 pagesMariano Marcos State University Case Studypeachsanchez BarrugaNo ratings yet

- Sales Performance Report: The Salesman JanuaryDocument21 pagesSales Performance Report: The Salesman JanuarymaheswaranNo ratings yet

- TB and HIV Target Achievement Trends Jan-Nov 2022Document9 pagesTB and HIV Target Achievement Trends Jan-Nov 2022Yulia Arum SekariniNo ratings yet

- Rural Men Employed in Tertary SectorDocument9 pagesRural Men Employed in Tertary SectorrazekumaNo ratings yet

- Roll 220225101010130 28 12 2022 P2 02 Hindi PDFDocument1 pageRoll 220225101010130 28 12 2022 P2 02 Hindi PDFAnkush KumarNo ratings yet

- Roll 220229202090219 18 01 2023 P1 02 Hindi PDFDocument1 pageRoll 220229202090219 18 01 2023 P1 02 Hindi PDFPankaj JanmejayNo ratings yet

- Blood Pressure Effects of DrugsDocument6 pagesBlood Pressure Effects of DrugsValerie IvanenkovaNo ratings yet

- Compute P40, P50 and P95 for the first documentDocument4 pagesCompute P40, P50 and P95 for the first documentMark TronNo ratings yet

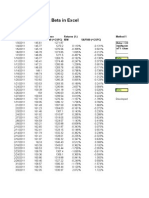

- Stock Beta ExcelDocument8 pagesStock Beta ExcelChi FongNo ratings yet

- Labour Cost 2016Document8 pagesLabour Cost 2016syahrulNo ratings yet

- Fill-Up Size Components Reference Sheet PDFDocument12 pagesFill-Up Size Components Reference Sheet PDFsubodhasinghNo ratings yet

- Table A: Producer's Price Index by Three Digit Level of ISIC : January 2014, December 2019 (Base Period: 2013 Q4 100)Document1 pageTable A: Producer's Price Index by Three Digit Level of ISIC : January 2014, December 2019 (Base Period: 2013 Q4 100)Muhazzam MaazNo ratings yet

- TOM Sesi 3 - Forecasting WorksheetDocument17 pagesTOM Sesi 3 - Forecasting WorksheetbadzwowNo ratings yet

- Economic Outlook For Southeast Asia, China and India 2022 - © OECD 2022 Disclaimer: Http://oe - Cd/disclaimerDocument3 pagesEconomic Outlook For Southeast Asia, China and India 2022 - © OECD 2022 Disclaimer: Http://oe - Cd/disclaimerKinjal ShethiaNo ratings yet

- Auto Co-Relation Co-EffDocument3 pagesAuto Co-Relation Co-Effsubham mishraNo ratings yet

- Table 1.3 USA Canada Japan France Germany Italy UKDocument1 pageTable 1.3 USA Canada Japan France Germany Italy UKHermann Habrahamsohn OrtizNo ratings yet

- Table 1.3 USA Canada Japan France Germany Italy UKDocument1 pageTable 1.3 USA Canada Japan France Germany Italy UKCecia Batista VergaraNo ratings yet

- Roll 220229202090219 18 01 2023 P1 16 Sanskrit PDFDocument1 pageRoll 220229202090219 18 01 2023 P1 16 Sanskrit PDFPankaj JanmejayNo ratings yet

- (A) MeanDocument2 pages(A) MeanNasif HassanNo ratings yet

- Book 1Document3 pagesBook 1MARIO JR. MODESTONo ratings yet

- Ashok Laylend stock performance over 2 yearsDocument4 pagesAshok Laylend stock performance over 2 yearsAli NadafNo ratings yet

- StatisticsDocument8 pagesStatisticsMarinel Mae ChicaNo ratings yet

- Index of Eight Core Industries (Base: 2004-05 100) March, 2016Document7 pagesIndex of Eight Core Industries (Base: 2004-05 100) March, 2016Santhosh KumarNo ratings yet

- Where We Left Off : - in GAA, I Pursued A Sector-Specific Long-Short StrategyDocument16 pagesWhere We Left Off : - in GAA, I Pursued A Sector-Specific Long-Short StrategySriniNo ratings yet

- Daily Sales Over TimeDocument5 pagesDaily Sales Over TimeMoidin AfsanNo ratings yet

- Raw DataDocument3 pagesRaw DataThessa Neca SagarioNo ratings yet

- Final NITs Branchwise Cut Off Marks & PercentileDocument59 pagesFinal NITs Branchwise Cut Off Marks & PercentileKorean kocchaNo ratings yet

- Labour Jan 08 To Jun08Document1 pageLabour Jan 08 To Jun08Mukesh Prasad GuptaNo ratings yet

- AP and MP Curves for Production StagesDocument1 pageAP and MP Curves for Production StagesStar OlsonNo ratings yet

- Vue eclatée - EACV-P1500YBLDocument11 pagesVue eclatée - EACV-P1500YBLissam.raqibi2021No ratings yet

- GRAFIKDocument4 pagesGRAFIKiqbal fahamzahNo ratings yet

- Hours Sorted Data (Ascending Order) Part (A)Document4 pagesHours Sorted Data (Ascending Order) Part (A)faisal58650No ratings yet

- 09 Self Educting Foam Nozzles CENDocument2 pages09 Self Educting Foam Nozzles CENneymarronNo ratings yet

- Psych Math B - AssignmentDocument1 pagePsych Math B - AssignmentSteph ClairNo ratings yet

- State Grid Loss AccountDocument7 pagesState Grid Loss AccountAkd DeshmukhNo ratings yet

- Water Consumption in The New York City - NYC Open Data1 PDFDocument1 pageWater Consumption in The New York City - NYC Open Data1 PDFVikesh RavichandrenNo ratings yet

- Instructions for 70-minute online examDocument1 pageInstructions for 70-minute online examAsif Faiyed (191011115)No ratings yet

- Regression Models to Predict Sales, Profits from AdsDocument2 pagesRegression Models to Predict Sales, Profits from AdsAINDRILA BERANo ratings yet

- Production Report by Field and by Operator, From January 2015 To September 2016Document32 pagesProduction Report by Field and by Operator, From January 2015 To September 2016balienniyazi2008No ratings yet

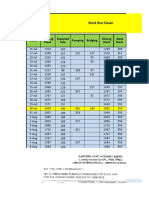

- Date Pumping Bridging Opening Stock Expected Sale Closing Stock Dead StockDocument5 pagesDate Pumping Bridging Opening Stock Expected Sale Closing Stock Dead StockAreeba MushtaqNo ratings yet

- Gasoline Price GraphDocument4 pagesGasoline Price GraphLuis AvilaNo ratings yet

- UntitledDocument5 pagesUntitledPalak SharmaNo ratings yet

- Chevrolet Malibu Workshop Manual v6 3 6l 2010 2Document1 pageChevrolet Malibu Workshop Manual v6 3 6l 2010 2stevenNo ratings yet

- Assign FC Bias - Assign 2Document5 pagesAssign FC Bias - Assign 2MUHAMMAD SOHAIB KHANNo ratings yet

- B 15 Harga Prices Sabah Sarawak 1 2023Document4 pagesB 15 Harga Prices Sabah Sarawak 1 2023Anonymous 60fJWeqdTNo ratings yet

- LJ Chart Electrolytes Dec 2022 - NewDocument49 pagesLJ Chart Electrolytes Dec 2022 - NewKoton RoyNo ratings yet

- Lab 1 (BTS3014)Document2 pagesLab 1 (BTS3014)NIVEDHA A P VADIVELUNo ratings yet

- CIM Final AssignmentDocument28 pagesCIM Final AssignmentFarhan AhmedNo ratings yet

- TQM Chapter 1Document23 pagesTQM Chapter 1Sir JuliusNo ratings yet

- TQM Chapter 1Document36 pagesTQM Chapter 1Sir JuliusNo ratings yet

- Ways Enjoy WorkDocument11 pagesWays Enjoy WorkGirlie Villar BulanonNo ratings yet

- ADVISORY No. 78 URGENT SUBMISSION OF THE PROPOSED PRIORITY POSITIONS FOR CREATION USING EQUAL 3-TRANCHE FUNDING SCHEME PDFDocument1 pageADVISORY No. 78 URGENT SUBMISSION OF THE PROPOSED PRIORITY POSITIONS FOR CREATION USING EQUAL 3-TRANCHE FUNDING SCHEME PDFSir JuliusNo ratings yet

- Accepted Papers PDFDocument7 pagesAccepted Papers PDFSir JuliusNo ratings yet

- SUC - NF - 2013 FORM-E2 ZCSPC Extension Program at Vitali Technical Vocational SchoolDocument18 pagesSUC - NF - 2013 FORM-E2 ZCSPC Extension Program at Vitali Technical Vocational SchoolKatz EscañoNo ratings yet

- Enhancing Capabilities For Delivery of Trainings FINALDocument60 pagesEnhancing Capabilities For Delivery of Trainings FINALSir JuliusNo ratings yet

- Pangasinan State University Research Proposal DevelopmentDocument1 pagePangasinan State University Research Proposal DevelopmentSir JuliusNo ratings yet

- Mvf404 Mhn-Seh2000w 956 b4 SiDocument2 pagesMvf404 Mhn-Seh2000w 956 b4 SiluisneiralopezNo ratings yet

- Oxford SuprEsser ManualDocument34 pagesOxford SuprEsser ManualaaaNo ratings yet

- Edema Paru Kardiogenik Akut Kak TiaraDocument8 pagesEdema Paru Kardiogenik Akut Kak TiaraTyara LarisaNo ratings yet

- Definisi, Karakteristik dan Contoh Aplikasi SIGDocument28 pagesDefinisi, Karakteristik dan Contoh Aplikasi SIGtoyota taaNo ratings yet

- Rotating Sharp Shooting Multi Target Mechanism Improves Military AimDocument13 pagesRotating Sharp Shooting Multi Target Mechanism Improves Military AimVishal GNo ratings yet

- Blackmer Pump Parts ListDocument2 pagesBlackmer Pump Parts ListFelipe Ignacio PaillavilNo ratings yet

- A Study On Renewable Energy Resources in IndiaDocument39 pagesA Study On Renewable Energy Resources in IndiaDevendra SharmaNo ratings yet

- HSB Julian Reyes 4ab 1Document3 pagesHSB Julian Reyes 4ab 1Kéññy RèqüēñåNo ratings yet

- management of burns readingDocument28 pagesmanagement of burns readinghimanshugupta811997No ratings yet

- 2024 Drik Panchang Telugu Calendar v1.0.1Document25 pages2024 Drik Panchang Telugu Calendar v1.0.1Sreekara GsNo ratings yet

- Audit Keselamatan Jalan Pada Jalan Yogyakarta-Purworejo KM 35-40, Kulon Progo, YogyakartaDocument10 pagesAudit Keselamatan Jalan Pada Jalan Yogyakarta-Purworejo KM 35-40, Kulon Progo, YogyakartaSawaluddin SawalNo ratings yet

- 2011 02 Huijben Spie Why Every Urea Plant Needs A Continuous NC Meter PDFDocument9 pages2011 02 Huijben Spie Why Every Urea Plant Needs A Continuous NC Meter PDFfawadintNo ratings yet

- Growth, Stagnation or Decline? Agfficulturalproductm'Iy in British IndiaDocument290 pagesGrowth, Stagnation or Decline? Agfficulturalproductm'Iy in British IndiaHarshadeep BiswasNo ratings yet

- Problem Set 3_Cross-Text ConnectionDocument31 pagesProblem Set 3_Cross-Text Connectiontrinhdat11012010No ratings yet

- Sample Only Do Not Reproduce: Trench Rescue Incident Organizational BoardDocument1 pageSample Only Do Not Reproduce: Trench Rescue Incident Organizational BoardLuis Diaz CerdanNo ratings yet

- Line Pack Presentation - Dec 2018Document7 pagesLine Pack Presentation - Dec 2018Goran JakupovićNo ratings yet

- DesignDocument2 pagesDesignAmr AbdalhNo ratings yet

- Separation and Purification TechnologyDocument10 pagesSeparation and Purification TechnologyPedro Henrique MagachoNo ratings yet

- Rites of Acceptance For Altar Servers PDFDocument3 pagesRites of Acceptance For Altar Servers PDFJohn Carl Aparicio100% (1)

- Systems Design: Job-Order Costing and Process Costing: MANAGEMENT ACCOUNTING - Solutions ManualDocument16 pagesSystems Design: Job-Order Costing and Process Costing: MANAGEMENT ACCOUNTING - Solutions ManualBianca LizardoNo ratings yet

- Estimating Hb Levels with Sahli's MethodDocument13 pagesEstimating Hb Levels with Sahli's MethodSANANo ratings yet

- Fundamental Calculations To Convert Intensities Into Concentrations in Optical Emission Spectrochemical AnalysisDocument14 pagesFundamental Calculations To Convert Intensities Into Concentrations in Optical Emission Spectrochemical AnalysisPYDNo ratings yet