You might also like

- Principles of Insurance Law with Case StudiesFrom EverandPrinciples of Insurance Law with Case StudiesRating: 5 out of 5 stars5/5 (1)

- Indemnity in International Oil and Gas ContractsDocument23 pagesIndemnity in International Oil and Gas ContractsLakshayNo ratings yet

- 14 Reinsurance PDFDocument28 pages14 Reinsurance PDFHalfani MoshiNo ratings yet

- A Practicle Guide To Construction Insurance CostDocument14 pagesA Practicle Guide To Construction Insurance CostvihangimaduNo ratings yet

- Re-Insurance Related LawsDocument13 pagesRe-Insurance Related LawsradhakrishnaNo ratings yet

- Vehicle InsuranceDocument31 pagesVehicle Insurancedhanaraj82No ratings yet

- 14 Reinsurance PDFDocument28 pages14 Reinsurance PDFHaider AliNo ratings yet

- 07 - Woolf1Document20 pages07 - Woolf1Yashveer Singh YadavNo ratings yet

- The Doctrine of Concealment - A Remnant in The Law of InsuranceDocument24 pagesThe Doctrine of Concealment - A Remnant in The Law of InsuranceVanesa SyNo ratings yet

- BMS AssignmentDocument3 pagesBMS AssignmentdreamsontherunwayNo ratings yet

- Chapter 2Document54 pagesChapter 2Anonymous WO7vzkjvNNo ratings yet

- Reinsurance: January 1998Document28 pagesReinsurance: January 1998Sudhakar GuntukaNo ratings yet

- Insurance Concepts: January 1998Document18 pagesInsurance Concepts: January 1998sunny rockyNo ratings yet

- The Design of Private Reinsurance Contracts: Financial Institutions CenterDocument26 pagesThe Design of Private Reinsurance Contracts: Financial Institutions CenterAbdoul Quang CuongNo ratings yet

- Re-Insurance Related Laws: Private International LawDocument5 pagesRe-Insurance Related Laws: Private International LawDevvrat garhwalNo ratings yet

- Re-Insurance: Private International LawDocument5 pagesRe-Insurance: Private International LawradhakrishnaNo ratings yet

- Insurance FeaturesDocument6 pagesInsurance FeaturesMayur ZambareNo ratings yet

- What Is InsuranceDocument2 pagesWhat Is InsuranceJamie RossNo ratings yet

- Rateable Proportion ClauseDocument2 pagesRateable Proportion ClausePrerana ChhapiaNo ratings yet

- Insurance PPDocument50 pagesInsurance PPmiadjafar463No ratings yet

- Re InsuranceDocument51 pagesRe Insuranceameydalvi91No ratings yet

- Reinsurance NotesDocument142 pagesReinsurance Notestendaihove264No ratings yet

- Nature and Scope of Liability Insurance in IndiaDocument7 pagesNature and Scope of Liability Insurance in IndiaAakaash Grover33% (3)

- ReinsuranceDocument142 pagesReinsuranceabhishek pathakNo ratings yet

- Assgmt 1 ReinsuranceDocument44 pagesAssgmt 1 ReinsuranceThevantharen MuniandyNo ratings yet

- Effects of Liability ClausesDocument2 pagesEffects of Liability ClausescngatiNo ratings yet

- Summary Insurance 91012Document5 pagesSummary Insurance 91012luna_puspitaNo ratings yet

- Consequences of Non-Disclosure in The Contract of InsuranceDocument8 pagesConsequences of Non-Disclosure in The Contract of InsuranceIOSRjournalNo ratings yet

- 6c IAA RB Ch6 ReinsuranceDocument22 pages6c IAA RB Ch6 ReinsuranceBison-Fûté LebesguesNo ratings yet

- 2 Insurance MidDocument5 pages2 Insurance MidacNo ratings yet

- Insurancelaw 2Document89 pagesInsurancelaw 2Rahul SinghNo ratings yet

- Law of Contracts 2 FinalDocument21 pagesLaw of Contracts 2 FinalDeepesh KumarNo ratings yet

- Notes On The Origin and Development of ReinsuranceDocument70 pagesNotes On The Origin and Development of Reinsuranceapi-261460293No ratings yet

- TOPIC 4. VALIDATION OF A CLAIM 1 and 2Document27 pagesTOPIC 4. VALIDATION OF A CLAIM 1 and 2Mujo TiNo ratings yet

- Insurance Law in India Question and AnswerDocument15 pagesInsurance Law in India Question and AnswerMaitrayee NandyNo ratings yet

- Insurance LawDocument3 pagesInsurance LawSonu MehthaNo ratings yet

- Dissertation ReinsuranceDocument4 pagesDissertation ReinsuranceWriteMyPaperSingapore100% (1)

- Insurance NotesDocument13 pagesInsurance NotesIrish Claire FornesteNo ratings yet

- The Merger or Insolvency Alternative in The Insurance IndustryDocument26 pagesThe Merger or Insolvency Alternative in The Insurance IndustrySrujan JNo ratings yet

- Introduction To Insurance and Reinsurance: January 2002Document15 pagesIntroduction To Insurance and Reinsurance: January 2002mooseman1980No ratings yet

- Insurance RegulationDocument6 pagesInsurance RegulationThanh N.No ratings yet

- Insurance Law (English) 2021Document47 pagesInsurance Law (English) 2021kairadigitalservicesNo ratings yet

- Lecture 8 InsuranceDocument8 pagesLecture 8 InsuranceAnna BrasoveanNo ratings yet

- Risk Which Can Be Insured by Private Companies Typically Share Seven Common CharacteristicsDocument10 pagesRisk Which Can Be Insured by Private Companies Typically Share Seven Common Characteristicsمنیب فراز درانیNo ratings yet

- Insurance PolicyDocument7 pagesInsurance PolicyCei mendozaNo ratings yet

- Public Liability Insurance 1Document10 pagesPublic Liability Insurance 1Ayanda MabuthoNo ratings yet

- How Insurance Works PDFDocument24 pagesHow Insurance Works PDFAviNo ratings yet

- Original 1489564315 Chapter 8 Property Per Risk XOL TreatyDocument12 pagesOriginal 1489564315 Chapter 8 Property Per Risk XOL TreatymakeshwaranNo ratings yet

- Law200 Final Body ReportDocument13 pagesLaw200 Final Body ReportAsad Uz JamanNo ratings yet

- Indemnity Provisions in Energy AgreementsDocument30 pagesIndemnity Provisions in Energy AgreementsJoySarkerNo ratings yet

- Reinsurance Basic GuideDocument80 pagesReinsurance Basic GuideNur AliaNo ratings yet

- Liability Insur WikipediaDocument14 pagesLiability Insur WikipediaDarshiniNo ratings yet

- Insurance Law - Part IDocument10 pagesInsurance Law - Part IBulelwa HarrisNo ratings yet

- Joint Pursuit of Recovery With An Insured: Issues For The Subrogating Carrier To ConsiderDocument11 pagesJoint Pursuit of Recovery With An Insured: Issues For The Subrogating Carrier To ConsiderAnton Ric Delos ReyesNo ratings yet

- Youngblood Flocos PracticalLawyerDocument17 pagesYoungblood Flocos PracticalLawyerKnowledge Guru100% (1)

- InsuranceDocument3 pagesInsuranceAzizi Mtumwa IddiNo ratings yet

- Risk Management: How to Use Different Insurance to Your BenefitFrom EverandRisk Management: How to Use Different Insurance to Your BenefitNo ratings yet

- Life, Accident and Health Insurance in the United StatesFrom EverandLife, Accident and Health Insurance in the United StatesRating: 5 out of 5 stars5/5 (1)

- ASDocument16 pagesASpradeep punuruNo ratings yet

- Bellum and Ius in Bello International Law. Some Questions May Be Solved Interpreting ExistingDocument5 pagesBellum and Ius in Bello International Law. Some Questions May Be Solved Interpreting Existingpradeep punuruNo ratings yet

- Later Vedic AgeDocument30 pagesLater Vedic Agepradeep punuruNo ratings yet

- Juris 2016084 SYNOPSISDocument4 pagesJuris 2016084 SYNOPSISpradeep punuruNo ratings yet

- Illegitimacy and Succession Under Private International Law 2Document22 pagesIllegitimacy and Succession Under Private International Law 2pradeep punuruNo ratings yet

- UGC RecommendationsDocument1 pageUGC Recommendationspradeep punuruNo ratings yet

- Skylit Terms and ConditionsDocument2 pagesSkylit Terms and Conditionspradeep punuruNo ratings yet

- Case Name: in Re Annesley: Davidson V. Annesley Case Citation: Facts of The CaseDocument2 pagesCase Name: in Re Annesley: Davidson V. Annesley Case Citation: Facts of The Casepradeep punuruNo ratings yet

- Tax II ProjectDocument23 pagesTax II Projectpradeep punuruNo ratings yet

- Itl Mid Sem NotesDocument8 pagesItl Mid Sem Notespradeep punuruNo ratings yet

- Damodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaDocument29 pagesDamodaram Sanjivayya National Law University Visakhapatnam, A.P., Indiapradeep punuru100% (1)

- Pbs IosDocument48 pagesPbs Iospradeep punuruNo ratings yet

- Case Analysis of Pradip TandonDocument2 pagesCase Analysis of Pradip Tandonpradeep punuruNo ratings yet

- 7) Who Wrote Globalisation and Its Discontents'Document3 pages7) Who Wrote Globalisation and Its Discontents'pradeep punuruNo ratings yet

- CRPC PradeepDocument24 pagesCRPC Pradeeppradeep punuruNo ratings yet

- E6sm ExcerptDocument2 pagesE6sm ExcerptEsra Gunes YildizNo ratings yet

- Communication v. SensingDocument6 pagesCommunication v. SensingLester BalagotNo ratings yet

- Bharti Axa Life InsuranceDocument94 pagesBharti Axa Life InsuranceVishal SoodanNo ratings yet

- Government Accounting and Non Profit OrgDocument4 pagesGovernment Accounting and Non Profit OrgPaupauNo ratings yet

- Fundamentals of Risk and Insurance 11Th Edition Vaughan Solutions Manual Full Chapter PDFDocument67 pagesFundamentals of Risk and Insurance 11Th Edition Vaughan Solutions Manual Full Chapter PDFjohnquyzwo9qa100% (13)

- Gard Rules 2011Document105 pagesGard Rules 2011Astrid AtehortúaNo ratings yet

- LifeInsRetirementValuation M05 LifeValuation 181205Document83 pagesLifeInsRetirementValuation M05 LifeValuation 181205Jeff JonesNo ratings yet

- Terms of Business Agreement BookletDocument12 pagesTerms of Business Agreement BookletAbraham MachadoNo ratings yet

- Pricing Insurance Risk Theory and Practice Stephen J Mildenhall All ChapterDocument67 pagesPricing Insurance Risk Theory and Practice Stephen J Mildenhall All Chaptergilbert.christner488100% (5)

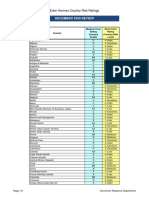

- December 2020 Review: Euler Hermes Country Risk RatingsDocument5 pagesDecember 2020 Review: Euler Hermes Country Risk RatingsLFNo ratings yet

- Al Madina - en PDFDocument236 pagesAl Madina - en PDFAkmal MazlanNo ratings yet

- Reinsurance List 2017Document10 pagesReinsurance List 2017Abdelrahman El-shafaeeNo ratings yet

- Unit 1 Study Material LOPDocument21 pagesUnit 1 Study Material LOPmeenasarathaNo ratings yet

- 18 Ifrs 17Document14 pages18 Ifrs 17DM BuenconsejoNo ratings yet

- Swiss Re: Global Share Participation Plan 2018 ProspectusDocument383 pagesSwiss Re: Global Share Participation Plan 2018 ProspectusMartin KalmanNo ratings yet

- Claims: Grounds For Denying LiabilityDocument11 pagesClaims: Grounds For Denying LiabilityDean RodriguezNo ratings yet

- Form LIB - FINALDocument22 pagesForm LIB - FINALibNo ratings yet

- Insurance Sector in IndiaDocument72 pagesInsurance Sector in IndiaTannya BrahmeNo ratings yet

- IBMDocument51 pagesIBMGayatri Swaminathan100% (1)

- Philam Vs Auditor GeneralDocument1 pagePhilam Vs Auditor GeneralRenz Aimeriza AlonzoNo ratings yet

- 165585Document14 pages165585The Supreme Court Public Information OfficeNo ratings yet

- Burglary, Robbery and Theft InsuranceDocument108 pagesBurglary, Robbery and Theft InsuranceShubham PhophaliaNo ratings yet

- Framework: General Concepts Life Insurance Non-Life InsuranceDocument92 pagesFramework: General Concepts Life Insurance Non-Life InsuranceDevilleres Eliza DenNo ratings yet

- Introduction To Reinsurance: Presentation by Holborn Corporation November 11, 2004Document24 pagesIntroduction To Reinsurance: Presentation by Holborn Corporation November 11, 2004Suresh100% (1)

- Afisco Insurance Corp V CADocument2 pagesAfisco Insurance Corp V CADon TiansayNo ratings yet

- Fieldmen's v. AsianDocument2 pagesFieldmen's v. Asiand2015memberNo ratings yet

- Chola MsDocument98 pagesChola MsDhaval224No ratings yet

- C3a - THE INSURANCE MECHANISM PDFDocument21 pagesC3a - THE INSURANCE MECHANISM PDFTzer Harn TanNo ratings yet

- RARBGDocument9 pagesRARBGAndrea IvanneNo ratings yet

- Ra 10607Document15 pagesRa 10607mblopez1100% (1)