You might also like

- ASSIGNMENT 1 and 2Document20 pagesASSIGNMENT 1 and 2Na Lisa Lee100% (3)

- Jessie Flores v. People (New Case)Document2 pagesJessie Flores v. People (New Case)xxxaaxxxNo ratings yet

- Performance Evaluation of PNB and HDFC BankDocument58 pagesPerformance Evaluation of PNB and HDFC BankEkam Jot100% (1)

- David v. Rongcal, A.C. No. 12103, 23 June 2020Document3 pagesDavid v. Rongcal, A.C. No. 12103, 23 June 2020xxxaaxxxNo ratings yet

- Banco Filipino v. Monetary Board Liquidation Authority CaseDocument2 pagesBanco Filipino v. Monetary Board Liquidation Authority CasexxxaaxxxNo ratings yet

- Consolidated Bank & Trust Corporation vs. CA, GR No. 138569 PDFDocument2 pagesConsolidated Bank & Trust Corporation vs. CA, GR No. 138569 PDFxxxaaxxx100% (1)

- Consolidated Bank & Trust Corporation vs. CA, GR No. 138569 PDFDocument2 pagesConsolidated Bank & Trust Corporation vs. CA, GR No. 138569 PDFxxxaaxxx100% (1)

- Equitable PCI v. Arcelito Tan, G.R. No. 165339Document2 pagesEquitable PCI v. Arcelito Tan, G.R. No. 165339xxxaaxxxNo ratings yet

- Consolidated Bank & Trust Corporation vs. CA, GR No. 138569 PDFDocument2 pagesConsolidated Bank & Trust Corporation vs. CA, GR No. 138569 PDFxxxaaxxx100% (1)

- Cash - TeachersDocument12 pagesCash - TeachersJustin ManaogNo ratings yet

- Westmont Bank liable for negligence of officer in bank vs Dela Rosa caseDocument1 pageWestmont Bank liable for negligence of officer in bank vs Dela Rosa caseLouie Marrero DadatNo ratings yet

- Westmont Bank CaseDocument2 pagesWestmont Bank CaseDave Lumasag CanumhayNo ratings yet

- GDocument1 pageGSteph LopezNo ratings yet

- GBL SET Case Digest 28 Aug 2021Document14 pagesGBL SET Case Digest 28 Aug 2021GiOvhanii BuenNo ratings yet

- Citystate Bank liable for agent's actsDocument4 pagesCitystate Bank liable for agent's actsJon Konrad AriasNo ratings yet

- Westmont Bank VS Dela Rosa-RamosDocument2 pagesWestmont Bank VS Dela Rosa-RamosCandelaria QuezonNo ratings yet

- Citystate Savings Bank VDocument3 pagesCitystate Savings Bank VAnnievin HawkNo ratings yet

- 34 City State Savings Bank Vs Teresita Tobias 3 7 18 G.R. No. 227990Document4 pages34 City State Savings Bank Vs Teresita Tobias 3 7 18 G.R. No. 227990RubenNo ratings yet

- Bank liable for paying crossed checks to unauthorized personDocument8 pagesBank liable for paying crossed checks to unauthorized personnikkeesNo ratings yet

- Simex Intl. Inc. vs. CADocument3 pagesSimex Intl. Inc. vs. CAZen DanielNo ratings yet

- City Savings v. TobiasDocument38 pagesCity Savings v. TobiasssNo ratings yet

- Westmont Bank Vs Dela RosaDocument1 pageWestmont Bank Vs Dela RosaJohn Benedict TigsonNo ratings yet

- Supreme Court Rules Bank Liable for Payment of Crossed Checks to Unauthorized PersonDocument4 pagesSupreme Court Rules Bank Liable for Payment of Crossed Checks to Unauthorized PersonpreiquencyNo ratings yet

- G.R. No. 84281Document1 pageG.R. No. 84281Rocky LadignonNo ratings yet

- Bank of America NT and SA vs. Associated Citizens BankDocument2 pagesBank of America NT and SA vs. Associated Citizens BankClauds GadzzNo ratings yet

- 23.17 - Associated Bank Vs CA - 1Document2 pages23.17 - Associated Bank Vs CA - 1Elaine Atienza-IllescasNo ratings yet

- 2022 Banking Law Digest For Prelim - AMORIO, Vikki Mae J.Document21 pages2022 Banking Law Digest For Prelim - AMORIO, Vikki Mae J.Vikki AmorioNo ratings yet

- Banking DigestsDocument9 pagesBanking DigestsEm DavidNo ratings yet

- City State Savings Bank Vs TobiasDocument2 pagesCity State Savings Bank Vs Tobiaspauline445No ratings yet

- City Trust Banking Corp Vs CruzDocument1 pageCity Trust Banking Corp Vs CruzDannethGianLatNo ratings yet

- Citystate Bank Held Liable for Negligence in Employee Fraud CaseDocument3 pagesCitystate Bank Held Liable for Negligence in Employee Fraud CaseMichael Vincent BautistaNo ratings yet

- Banking Law, Central Bank Act, SRC, Foreign Investment, Letters of CreditDocument45 pagesBanking Law, Central Bank Act, SRC, Foreign Investment, Letters of Creditflordeluna ayingNo ratings yet

- Banks' fiduciary duty and obligation to depositorsDocument1 pageBanks' fiduciary duty and obligation to depositorsMicaela Dela PeñaNo ratings yet

- National Bank V. Manila Oil Refining 43 PHIL 444 FactsDocument3 pagesNational Bank V. Manila Oil Refining 43 PHIL 444 FactsPJANo ratings yet

- Forgery CasesDocument14 pagesForgery CasesKirby ReniaNo ratings yet

- Citystate Savings Bank V TobiasDocument2 pagesCitystate Savings Bank V TobiasSha Santos100% (1)

- 2022 Banking Law Digest For PrelimDocument15 pages2022 Banking Law Digest For PrelimJem PagantianNo ratings yet

- Rodriguez G.R. No. 170325: #16 PNB VsDocument2 pagesRodriguez G.R. No. 170325: #16 PNB VsAdrian HilarioNo ratings yet

- Banking Laws and Jurisprudence 2009 Party Duh NotesDocument62 pagesBanking Laws and Jurisprudence 2009 Party Duh NotesPhilipBrentMorales-MartirezCariagaNo ratings yet

- Associated Bank v. Court of Appeals G.R. No. 89802 07 May 1992 Case DigestDocument3 pagesAssociated Bank v. Court of Appeals G.R. No. 89802 07 May 1992 Case DigestPhi SalvadorNo ratings yet

- Bank negligence leads to bounced checksDocument2 pagesBank negligence leads to bounced checksxxxaaxxx67% (3)

- Philippine bank fiduciary duties and obligationsDocument3 pagesPhilippine bank fiduciary duties and obligationsJun JunNo ratings yet

- Banking Law Case DigestsDocument4 pagesBanking Law Case DigestsPatricia PinedaNo ratings yet

- Associated Bank vs. CADocument4 pagesAssociated Bank vs. CARio Jean QuindaraNo ratings yet

- 2022 Banking Law Digest For Prelim - AMORIO, Vikki Mae J.Document45 pages2022 Banking Law Digest For Prelim - AMORIO, Vikki Mae J.Vikki AmorioNo ratings yet

- BANK LIABILITY FOR FRAUDULENT CHECKSDocument34 pagesBANK LIABILITY FOR FRAUDULENT CHECKSJobelle VillanuevaNo ratings yet

- Philippine Commercial International Bank v. Court of Appeals, G.R. No. 121413 January 29, 2001Document23 pagesPhilippine Commercial International Bank v. Court of Appeals, G.R. No. 121413 January 29, 2001Krister VallenteNo ratings yet

- BPI V. COURT OF APPEALS DECISION ON BANK LIABILITYDocument4 pagesBPI V. COURT OF APPEALS DECISION ON BANK LIABILITYChristopher PhilipNo ratings yet

- Libertas (Jurisprudence On Nego)Document106 pagesLibertas (Jurisprudence On Nego)Vince AbucejoNo ratings yet

- PCIB v. CA: Banks Liable for Negligence in Handling ChecksDocument3 pagesPCIB v. CA: Banks Liable for Negligence in Handling ChecksCharm Divina LascotaNo ratings yet

- PCIB Vs CADocument2 pagesPCIB Vs CAMark Gabriel B. MarangaNo ratings yet

- Banking Law and PracticeDocument5 pagesBanking Law and PracticeiantseriweNo ratings yet

- Bank Errors Lead to DamagesDocument3 pagesBank Errors Lead to DamagesJherna TabulogNo ratings yet

- Nego - Check CasesDocument3 pagesNego - Check CasesRizel C. BarsabalNo ratings yet

- Banking Cases Week 1Document5 pagesBanking Cases Week 1Katrina PerezNo ratings yet

- Citystate Savings Bank vs. TobiasDocument1 pageCitystate Savings Bank vs. TobiasDianne YcoNo ratings yet

- METROPOLITAN BANK AND TRUST CO. V CABILZODocument2 pagesMETROPOLITAN BANK AND TRUST CO. V CABILZOshortsandcutsNo ratings yet

- Banking Case DoctrinesDocument9 pagesBanking Case DoctrinesDennice Erica DavidNo ratings yet

- Banking Law Case DigestsDocument4 pagesBanking Law Case DigestsZaira Gem Gonzales100% (1)

- Banking Law Practice Questions and Answers 2Document4 pagesBanking Law Practice Questions and Answers 2Phetho MachiliNo ratings yet

- Banks Liable for Negligence in Client DepositsDocument2 pagesBanks Liable for Negligence in Client DepositsLuke VerdaderoNo ratings yet

- Bank Liability for Acts of Branch ManagerDocument12 pagesBank Liability for Acts of Branch ManagerFranz Raymond Javier AquinoNo ratings yet

- Bank of America v. Phil Racing Club DigestDocument3 pagesBank of America v. Phil Racing Club DigestCelineNo ratings yet

- PNB LIABLE FOR DISHONORED CHECKS DUE TO INVALID DEPOSITSDocument14 pagesPNB LIABLE FOR DISHONORED CHECKS DUE TO INVALID DEPOSITSJustice PajarilloNo ratings yet

- Banking Law Case Digest: Citystate Savings Bank v. Teresita TobiasDocument7 pagesBanking Law Case Digest: Citystate Savings Bank v. Teresita TobiasAnastasia ZaitsevNo ratings yet

- 310 Supreme Court Reports AnnotatedDocument10 pages310 Supreme Court Reports AnnotatedNinaNo ratings yet

- Simex International v. CA, G.R. No. 88013. 89 Scra 360. March 19, 1990Document1 pageSimex International v. CA, G.R. No. 88013. 89 Scra 360. March 19, 1990Pamela Camille BarredoNo ratings yet

- Rural Bank of Buhi v. CA, G.R. No. L-61689Document2 pagesRural Bank of Buhi v. CA, G.R. No. L-61689xxxaaxxxNo ratings yet

- Lung Center of The Phil. vs. Quezon City, Et Al., G.R. No. 144104, June 29, 2004Document4 pagesLung Center of The Phil. vs. Quezon City, Et Al., G.R. No. 144104, June 29, 2004xxxaaxxx100% (1)

- Intercontinental Broadcasting Corp. vs. Noemi B. Amarilla, Et Al., G.R. No. 162775, October 27, 2006Document2 pagesIntercontinental Broadcasting Corp. vs. Noemi B. Amarilla, Et Al., G.R. No. 162775, October 27, 2006xxxaaxxxNo ratings yet

- CIR vs. Citytrust and Asianbank - 20% FWT Included in Computing 5% GRTDocument4 pagesCIR vs. Citytrust and Asianbank - 20% FWT Included in Computing 5% GRTxxxaaxxxNo ratings yet

- Villanueva v. CA, G.R. No. 114870Document2 pagesVillanueva v. CA, G.R. No. 114870xxxaaxxx100% (5)

- RBSM v. MB, G.R. No. 150886Document1 pageRBSM v. MB, G.R. No. 150886xxxaaxxxNo ratings yet

- Pacific Banking Corp. EE's Org. v. CA, G.R. No. 109373Document1 pagePacific Banking Corp. EE's Org. v. CA, G.R. No. 109373xxxaaxxx100% (1)

- Judge Dumlao v. Camacho, A.C. No. 10498, 4 September 2018Document5 pagesJudge Dumlao v. Camacho, A.C. No. 10498, 4 September 2018xxxaaxxxNo ratings yet

- Central Bank v. CA, G.R. No. 76118Document2 pagesCentral Bank v. CA, G.R. No. 76118xxxaaxxx100% (1)

- Koruga v. Arcenas, Et. Al, G.R. No. 168332Document2 pagesKoruga v. Arcenas, Et. Al, G.R. No. 168332xxxaaxxxNo ratings yet

- Abacus v. Manila Banking Corp., G.R. No. 162270Document2 pagesAbacus v. Manila Banking Corp., G.R. No. 162270xxxaaxxxNo ratings yet

- Republic v. Hon. Antonio M. Eugenio, G.R. No. 174629, February 14, 2008Document3 pagesRepublic v. Hon. Antonio M. Eugenio, G.R. No. 174629, February 14, 2008xxxaaxxx80% (5)

- Hon. Monetary Board v. PVB, G.R. No. 189571Document2 pagesHon. Monetary Board v. PVB, G.R. No. 189571xxxaaxxx0% (1)

- MCC Industrial Sales v. Ssanyong CorporationDocument1 pageMCC Industrial Sales v. Ssanyong CorporationxxxaaxxxNo ratings yet

- First Phil. Int'l Bank v. CA ruling on conservator powerDocument2 pagesFirst Phil. Int'l Bank v. CA ruling on conservator powerxxxaaxxx50% (4)

- Central Bank Circular No. 364 and Related Regulations on Foreign Exchange TransactionsDocument2 pagesCentral Bank Circular No. 364 and Related Regulations on Foreign Exchange TransactionsxxxaaxxxNo ratings yet

- Funa v. Manila Economic and Cultural OfficeDocument5 pagesFuna v. Manila Economic and Cultural OfficexxxaaxxxNo ratings yet

- Bank negligence leads to bounced checksDocument2 pagesBank negligence leads to bounced checksxxxaaxxx67% (3)

- Codilla Vs de Venecia (2002)Document4 pagesCodilla Vs de Venecia (2002)xxxaaxxxNo ratings yet

- Pana vs. Heirs of Juanite, Sr. (2012)Document2 pagesPana vs. Heirs of Juanite, Sr. (2012)xxxaaxxxNo ratings yet

- City of Manila v. Jacinto Del Rosario PDFDocument4 pagesCity of Manila v. Jacinto Del Rosario PDFxxxaaxxxNo ratings yet

- 064 - Arica v. NLRC - PascoDocument2 pages064 - Arica v. NLRC - Pascoxxxaaxxx100% (1)

- Banking Laws and Jurisprudence ReviewerDocument81 pagesBanking Laws and Jurisprudence ReviewerRonald ErigaNo ratings yet

- Audit MTP2 QP M24 @CAInterLegendsDocument17 pagesAudit MTP2 QP M24 @CAInterLegendssharmaansshumanNo ratings yet

- Bank ReconciliationDocument11 pagesBank ReconciliationKamrul Hasan100% (1)

- SOC Conv EnglishDocument25 pagesSOC Conv Englishwww.aslamarian541No ratings yet

- Estado Bancario ChaseDocument2 pagesEstado Bancario ChasePedro Ant. Núñez Ulloa100% (1)

- UK NEO-BANKS: COMPARING MONZO, STARLING AND REVOLUTDocument15 pagesUK NEO-BANKS: COMPARING MONZO, STARLING AND REVOLUTTurab DXBNo ratings yet

- Black BookDocument72 pagesBlack BookVikash Maurya0% (1)

- BMF FullDocument48 pagesBMF FullPunya KrishnaNo ratings yet

- Icici Bank Loans PDFDocument3 pagesIcici Bank Loans PDFRagothaman RNo ratings yet

- HTR 043235 PDFDocument4 pagesHTR 043235 PDFCjNo ratings yet

- CRM for Modern Retail Banking in Kotak Mahindra BankDocument71 pagesCRM for Modern Retail Banking in Kotak Mahindra BankHimali ChandwaniNo ratings yet

- Business COMMUNICATION + CHANGESDocument56 pagesBusiness COMMUNICATION + CHANGESDavinchi Davinchi DaniNo ratings yet

- Chapter 7 SolutionsDocument6 pagesChapter 7 SolutionsJay100% (1)

- Quick BooksDocument22 pagesQuick BooksENIDNo ratings yet

- General Banking of AIBLDocument30 pagesGeneral Banking of AIBLnabil ibrahimNo ratings yet

- Checking Account and Savings Account ChartDocument2 pagesChecking Account and Savings Account ChartMichelle StubbsNo ratings yet

- Ap CceDocument209 pagesAp CceTrisha RafalloNo ratings yet

- Evaluation of Loans and Advances: Chapter-1Document77 pagesEvaluation of Loans and Advances: Chapter-1VeereshNo ratings yet

- Exercise ISB548 January 2021Document4 pagesExercise ISB548 January 2021Atiqah AzmanNo ratings yet

- Bim NotesDocument12 pagesBim NotesBasudev SahooNo ratings yet

- FM 03 Financial IntermediationDocument8 pagesFM 03 Financial IntermediationIvy ObligadoNo ratings yet

- Chapter 6: Appropriation of Profits: Rohit AgarwalDocument4 pagesChapter 6: Appropriation of Profits: Rohit AgarwalbcomNo ratings yet

- Tariff Booklet: October 2021Document16 pagesTariff Booklet: October 2021Anonymous ameerNo ratings yet

- A Study On AtmDocument143 pagesA Study On AtmAbhishek PandeyNo ratings yet

- Banking Sector in India: Functions and DevelopmentDocument148 pagesBanking Sector in India: Functions and DevelopmentAkash JainNo ratings yet

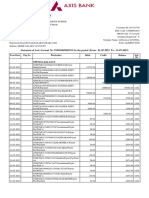

- Axis Bank Statement - 3monthsDocument4 pagesAxis Bank Statement - 3monthsnazeerhussain133No ratings yet

- 09-Angadanan2020 Part2-Findings and RecommDocument75 pages09-Angadanan2020 Part2-Findings and RecommAlicia NhsNo ratings yet