You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5796)

- Asifma Aplma Icma Isda Ibor Transition Guide For AsiaDocument15 pagesAsifma Aplma Icma Isda Ibor Transition Guide For AsiaRohit GajareNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- From LIBOR To SONIA and What You Need To KnowDocument3 pagesFrom LIBOR To SONIA and What You Need To KnowRohit GajareNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- An Economic Perspective On Payments Migration: Staff Working Paper/Document de Travail Du Personnel - 2020-24Document58 pagesAn Economic Perspective On Payments Migration: Staff Working Paper/Document de Travail Du Personnel - 2020-24Rohit GajareNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Outlook On Artificial Intelligence in The EnterpriseDocument12 pagesOutlook On Artificial Intelligence in The EnterpriseRohit GajareNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Sample Credco Report PDFDocument9 pagesSample Credco Report PDFKeith GoeringerNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Problems Ledger Account 1 5 UnsolvedDocument11 pagesProblems Ledger Account 1 5 UnsolvedNeeraj Gugle0% (1)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Indeks Bisnis-27 Menghijau: Data SahamDocument6 pagesIndeks Bisnis-27 Menghijau: Data SahamIndri ParwataNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument3 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceSridhar RamanNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- FinanceDocument5 pagesFinanceYixuan PENGNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- FARAP-4501 (Cash and Cash Equivalents)Document10 pagesFARAP-4501 (Cash and Cash Equivalents)Marya NvlzNo ratings yet

- Account Statement From 1 Apr 2021 To 31 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument14 pagesAccount Statement From 1 Apr 2021 To 31 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRishav AnandNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Chapter 7 - International Arbitrage and IRPDocument30 pagesChapter 7 - International Arbitrage and IRPPháp NguyễnNo ratings yet

- Fixed Deposit SampleDocument21 pagesFixed Deposit SampleSuriyachakArchwichaiNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

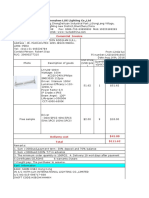

- Shenzhen LUX Lighting Co.,Ltd: Comercial InvoiceDocument2 pagesShenzhen LUX Lighting Co.,Ltd: Comercial InvoiceStefanie Joselyn Llosa RodriguezNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- NRB RemitDocument56 pagesNRB Remitনীল রহমানNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Tutorial Week 9: Chapter 11: International Debt Financing Chapter 12: International Equity FinancingDocument15 pagesTutorial Week 9: Chapter 11: International Debt Financing Chapter 12: International Equity FinancingSmartunblurrNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- EMV SDA Vs DDADocument6 pagesEMV SDA Vs DDAimvijayNo ratings yet

- What Are NBFCsDocument12 pagesWhat Are NBFCsRohan ShirdhankarNo ratings yet

- Here's Your February 2021 Bank Statement.: Axleis Pardias 6725 Brittmoore RD Apt 3308 Houston TX 77041-3818Document5 pagesHere's Your February 2021 Bank Statement.: Axleis Pardias 6725 Brittmoore RD Apt 3308 Houston TX 77041-3818axleisNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- ATM Refilling ModelDocument6 pagesATM Refilling ModelPrashant KumarNo ratings yet

- Handout Mathematics of Investment PDFDocument36 pagesHandout Mathematics of Investment PDFJhon Carlo Delmonte100% (7)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Invoice - 000000004097-001Document3 pagesInvoice - 000000004097-001Alejandro Pedroza CéspedesNo ratings yet

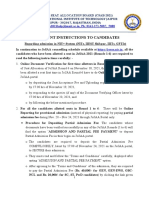

- Imp. Instructions For JoSAA R6Document2 pagesImp. Instructions For JoSAA R6Anurag MandloiNo ratings yet

- c1033 EftsDocument16 pagesc1033 EftsmayoNo ratings yet

- PSE213 Weida Su Final DraftDocument5 pagesPSE213 Weida Su Final Draft苏瑞迪No ratings yet

- Indian Banking System by Swapnil Chavan in Banking and Insurance Category On ManagementParadise - 13Document66 pagesIndian Banking System by Swapnil Chavan in Banking and Insurance Category On ManagementParadise - 13Sonu SharmaNo ratings yet

- Bond Equivalent Yield Financial MarketsDocument5 pagesBond Equivalent Yield Financial MarketsLianne PadillaNo ratings yet

- Northern Rock Provisional Restructuring Plan March 31 2008Document12 pagesNorthern Rock Provisional Restructuring Plan March 31 2008mckenzie0415No ratings yet

- Mutasi Transaksi - PermataME6574 - 81202124819Document4 pagesMutasi Transaksi - PermataME6574 - 81202124819jainulNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Ifrs 9 Ecl Template General ApproachDocument2 pagesIfrs 9 Ecl Template General ApproachTousief NaqviNo ratings yet

- Account Ledger Inquiry: Menu Show Memo Pad Background Menu CCY ConverterDocument2 pagesAccount Ledger Inquiry: Menu Show Memo Pad Background Menu CCY Convertersarwan kumarNo ratings yet

- Chapter23 Audit of Cash BalancesDocument37 pagesChapter23 Audit of Cash BalancesJesssel Marian AbrahamNo ratings yet

- Boe 13Document62 pagesBoe 13Dhananjay SinghNo ratings yet

- TNC Family BankingDocument5 pagesTNC Family BankingarshadNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)