You might also like

- Intangible Non Current AssetsDocument4 pagesIntangible Non Current AssetssadikiNo ratings yet

- Chapter 5 Audit Planning and Documentation: Learning ObjectivesDocument17 pagesChapter 5 Audit Planning and Documentation: Learning ObjectivesImamul MorsalinNo ratings yet

- IAS#38Document43 pagesIAS#38Shah KamalNo ratings yet

- Chapter 13 Audit of Non-Current Assets: Learning ObkectivesDocument15 pagesChapter 13 Audit of Non-Current Assets: Learning ObkectivesHoà TrầnNo ratings yet

- Chapter 5 Audit Planning and Documentation: Learning ObjectivesDocument17 pagesChapter 5 Audit Planning and Documentation: Learning Objectivessathish_inboxNo ratings yet

- Chapter 9 Intangible AssetsDocument36 pagesChapter 9 Intangible AssetsLEE WEI LONGNo ratings yet

- Audit Risks and MaterialityDocument11 pagesAudit Risks and MaterialityMohsin BasheerNo ratings yet

- Kaplan Ias 38 FinalDocument27 pagesKaplan Ias 38 FinalMahlet AbrahaNo ratings yet

- Intangible AssetsDocument16 pagesIntangible Assets566973801967% (3)

- L6 Intangible AssetsDocument43 pagesL6 Intangible AssetsЛинкольн ХaйдаровNo ratings yet

- Ias 38 Intangible AssetsDocument5 pagesIas 38 Intangible AssetsArogundade kamaldeenNo ratings yet

- Ind AS-38: Intangible Assets: 1. ScopeDocument21 pagesInd AS-38: Intangible Assets: 1. ScopeRochak ShresthaNo ratings yet

- PAS 38 Test BankDocument9 pagesPAS 38 Test BankJake ScotNo ratings yet

- Recent Studies/Tax Credit Benefits ObtainedDocument7 pagesRecent Studies/Tax Credit Benefits ObtainedResearch and Development Tax Credit Magazine; David Greenberg PhD, MSA, EA, CPA; TGI; 646-705-2910No ratings yet

- Summary Notes in Intangible Assets PDFDocument5 pagesSummary Notes in Intangible Assets PDFJohn Kenneth100% (1)

- Intangible AssetsmarykellyDocument7 pagesIntangible AssetsmarykellyAshura ShaibNo ratings yet

- Isa 38Document7 pagesIsa 38shahidgondal17No ratings yet

- Finacc 3Document6 pagesFinacc 3Tong WilsonNo ratings yet

- C35 - MFRS 138 IntangiblesDocument28 pagesC35 - MFRS 138 IntangibleskkNo ratings yet

- Intangible Assets NotesDocument6 pagesIntangible Assets NotesRaizel RamirezNo ratings yet

- Solution Manual For Applying International Financial Reporting Standards Picker Leo Loftus Wise Clark Alfredson 3rd EditionDocument22 pagesSolution Manual For Applying International Financial Reporting Standards Picker Leo Loftus Wise Clark Alfredson 3rd EditionDouglasWhiteheadxkwi100% (42)

- IndAS38 2019Document37 pagesIndAS38 2019WHY KODALINo ratings yet

- Acc TheoryDocument16 pagesAcc TheoryZHI QI chanNo ratings yet

- Intangible AssetsDocument4 pagesIntangible Assetsbrooke100% (1)

- Financial Accounting: Theory & Practice Intangible AssetsDocument81 pagesFinancial Accounting: Theory & Practice Intangible AssetsXNo ratings yet

- Intangible AssetsDocument24 pagesIntangible AssetsUnsolved MistryNo ratings yet

- Intangible AssetsDocument9 pagesIntangible AssetsDaniellaNo ratings yet

- Intangible Asset (Part 3)Document21 pagesIntangible Asset (Part 3)samundeswaryNo ratings yet

- Telstra CoDocument5 pagesTelstra Coharoon nasirNo ratings yet

- Intangible AssetsDocument8 pagesIntangible AssetsHoàng HạnhNo ratings yet

- 04 Ias 38Document4 pages04 Ias 38Irtiza AbbasNo ratings yet

- Week 5 C35 - MFRS 138 IntangiblesDocument26 pagesWeek 5 C35 - MFRS 138 IntangiblesYong Arifin0% (1)

- Bakercorpform10 QDocument55 pagesBakercorpform10 QTalha MalikNo ratings yet

- Using Financial Modeling Techniques To Value Structure M AsDocument19 pagesUsing Financial Modeling Techniques To Value Structure M Astommysyah100% (1)

- Images PDF DR - Haider Intangible-AssetsDocument30 pagesImages PDF DR - Haider Intangible-AssetsMahlet AbrahaNo ratings yet

- Accounting Standard 26Document16 pagesAccounting Standard 26Melissa ArnoldNo ratings yet

- QBDocument43 pagesQBSaurav DhyaniNo ratings yet

- Chapter 14 Fill-In NotesDocument5 pagesChapter 14 Fill-In Noteslowell MooreNo ratings yet

- Akuntansi Pajak Bab 11 Intangible Asset AccountingDocument20 pagesAkuntansi Pajak Bab 11 Intangible Asset AccountingGregorius ReghiNo ratings yet

- Ias 38 - TSVHDocument37 pagesIas 38 - TSVHHồ Đan ThụcNo ratings yet

- IFRS Development Costs Recognition PDFDocument3 pagesIFRS Development Costs Recognition PDFmizarkoNo ratings yet

- Module 14 PAS 38Document5 pagesModule 14 PAS 38Jan JanNo ratings yet

- 10.11 AS 26 Intangible AssetsDocument5 pages10.11 AS 26 Intangible AssetsAnakin SkywalkerNo ratings yet

- Module 7 IntangiblesDocument14 pagesModule 7 Intangiblestite ko'y malakeNo ratings yet

- B215 AC11 Can You See It 6th Presentation 27may2009Document36 pagesB215 AC11 Can You See It 6th Presentation 27may2009tohqinzhiNo ratings yet

- CA Inter Paper 6 Compiler 8-8-22Document316 pagesCA Inter Paper 6 Compiler 8-8-22KaviyaNo ratings yet

- Chapter 12 Intangible Assets ReviewerDocument4 pagesChapter 12 Intangible Assets ReviewerKaname KuranNo ratings yet

- IAS 38 Intangible Assets ExplainedDocument10 pagesIAS 38 Intangible Assets ExplainedBhuvaneswari karuturiNo ratings yet

- INTANGIBLESDocument40 pagesINTANGIBLESPhoebe Dayrit CunananNo ratings yet

- Intangible AssetDocument38 pagesIntangible AssetRimissha Udenia 2No ratings yet

- Tab Le of C OntentDocument15 pagesTab Le of C OntentSheikh Muhammad ShabbirNo ratings yet

- Accountancy Extra PointsDocument14 pagesAccountancy Extra PointsRishav KuriNo ratings yet

- Intangible Assets IjazDocument2 pagesIntangible Assets IjazIjaz MalikNo ratings yet

- Do You Want to Be a Digital Entrepreneur? What You Need to Know to Start and Protect Your Knowledge-Based Digital BusinessFrom EverandDo You Want to Be a Digital Entrepreneur? What You Need to Know to Start and Protect Your Knowledge-Based Digital BusinessNo ratings yet

- Module 7 IntangiblesDocument14 pagesModule 7 IntangiblesEarl ENo ratings yet

- CH 7 Ias 38 Intangible Assets+ Ifrs 3 GoodwillDocument2 pagesCH 7 Ias 38 Intangible Assets+ Ifrs 3 Goodwillmohamed.shaban2533No ratings yet

- Contoh JournalDocument5 pagesContoh Journalsophia1388No ratings yet

- Black Book ProjectDocument63 pagesBlack Book ProjectAkash Pawaskar75% (4)

- Pas 38 - Intangible AssetsDocument21 pagesPas 38 - Intangible AssetsMa. Franceska Loiz T. RiveraNo ratings yet

- Valuations of Early-Stage Companies and Disruptive Technologies: How to Value Life Science, Cybersecurity and ICT Start-ups, and their TechnologiesFrom EverandValuations of Early-Stage Companies and Disruptive Technologies: How to Value Life Science, Cybersecurity and ICT Start-ups, and their TechnologiesNo ratings yet

- Ifrs5 SN PDFDocument5 pagesIfrs5 SN PDFAmrita TamangNo ratings yet

- Ifrs5 SN PDFDocument5 pagesIfrs5 SN PDFAmrita TamangNo ratings yet

- Nas23 PDFDocument25 pagesNas23 PDFAmrita TamangNo ratings yet

- Assignment 1 j14 Solutions Final PDFDocument14 pagesAssignment 1 j14 Solutions Final PDFAmrita TamangNo ratings yet

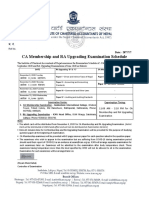

- CA Membership and RA Upgrading Examination Schedule: Date: - 2077/7/7Document1 pageCA Membership and RA Upgrading Examination Schedule: Date: - 2077/7/7Amrita TamangNo ratings yet

- 44 Ind AS 102 Share Based Payment 1201Document87 pages44 Ind AS 102 Share Based Payment 1201Ahmed MadhaNo ratings yet

- Share-Based Payment: A Practical Guide To Applying IFRS 2Document57 pagesShare-Based Payment: A Practical Guide To Applying IFRS 2georgepNo ratings yet

- Accounting Policies, Changes in Accounting Estimates and ErrorsDocument32 pagesAccounting Policies, Changes in Accounting Estimates and ErrorsAmrita TamangNo ratings yet

- Question 63: Advanced ConsolidationDocument8 pagesQuestion 63: Advanced ConsolidationAmrita TamangNo ratings yet

- FIFO, LIFO inventory accounting methods impactDocument2 pagesFIFO, LIFO inventory accounting methods impactKanika Bothra 1820441No ratings yet

- QR Code (Partnership)Document10 pagesQR Code (Partnership)saumya sainiNo ratings yet

- Accounting For EngineersDocument38 pagesAccounting For EngineersMunir KadernaniNo ratings yet

- P1 - Corporate Reporting April 11Document20 pagesP1 - Corporate Reporting April 11Abdurrazaq PanhwarNo ratings yet

- Business CombinationDocument3 pagesBusiness CombinationJia CruzNo ratings yet

- Diagnostic ExaminationDocument9 pagesDiagnostic ExaminationPatOcampoNo ratings yet

- IFRS Edition-2nd: Conceptual Framework For Financial ReportingDocument30 pagesIFRS Edition-2nd: Conceptual Framework For Financial ReportingAhmed SroorNo ratings yet

- Untitled DocumentDocument3 pagesUntitled DocumentchesNo ratings yet

- End Term Paper FACD 2020Document8 pagesEnd Term Paper FACD 2020Saksham SinhaNo ratings yet

- Oracle General Ledger statutory requirements assessmentDocument3 pagesOracle General Ledger statutory requirements assessmentSandip GhoshNo ratings yet

- Control and Significant InfluenceDocument11 pagesControl and Significant InfluencePatrick ArazoNo ratings yet

- Indian Accounting Standard 101Document19 pagesIndian Accounting Standard 101RITZ BROWNNo ratings yet

- Baskoro Riyanto - 023001800063 - Latihan Soal AKL IIDocument4 pagesBaskoro Riyanto - 023001800063 - Latihan Soal AKL IIBaskoro RiyantoNo ratings yet

- MCQs On Issue of DebenturesDocument7 pagesMCQs On Issue of DebenturesRamNo ratings yet

- Admission of A PartnerDocument5 pagesAdmission of A PartnerHigreeve SrudhiNo ratings yet

- Business CombinationDocument4 pagesBusiness CombinationNicole AutrizNo ratings yet

- Chapter 3 IFRS 10 Consolidated Financial Statements Part 2Document122 pagesChapter 3 IFRS 10 Consolidated Financial Statements Part 2Nanya BisnestNo ratings yet

- f1 Answers Nov14Document14 pagesf1 Answers Nov14Atif Rehman100% (1)

- Equity Investments 2019 RecapDocument10 pagesEquity Investments 2019 RecapAlmirah's iCPA ReviewNo ratings yet

- Project report on mergers, amalgamations and takeoversDocument18 pagesProject report on mergers, amalgamations and takeoversSunita YadavNo ratings yet

- Entrep Q2 M15 17Document16 pagesEntrep Q2 M15 17Joanna Mae PlacidoNo ratings yet

- Chapter 03 Consolidations-Subsequent To The Date of AcquisitionDocument111 pagesChapter 03 Consolidations-Subsequent To The Date of AcquisitionDenise Jane RoqueNo ratings yet

- Purchase ConsiderationDocument5 pagesPurchase ConsiderationAR Ananth Rohith BhatNo ratings yet

- Accounts 2Document41 pagesAccounts 2SubodhSaxenaNo ratings yet

- Chapter 17 - Partnership FormationDocument3 pagesChapter 17 - Partnership FormationKaori MiyazonoNo ratings yet

- Consolidated Financial StatementsDocument35 pagesConsolidated Financial Statementsnaseer ahmedNo ratings yet

- Order Against M/s Sai Praksah Properties Development Ltd. and Its Directors/promotersDocument22 pagesOrder Against M/s Sai Praksah Properties Development Ltd. and Its Directors/promotersShyam SunderNo ratings yet

- ACCA Strategic Business Reporting (SBR) Achievement Ladder Step 8 Questions & AnswersDocument22 pagesACCA Strategic Business Reporting (SBR) Achievement Ladder Step 8 Questions & AnswersAdam MNo ratings yet

- The Main New Irish Gaap Standard: Implications For The Hotel SectorDocument20 pagesThe Main New Irish Gaap Standard: Implications For The Hotel Sectorwattersed1711No ratings yet