You might also like

- 2015 AGCS Global Claims Review 2015Document40 pages2015 AGCS Global Claims Review 2015Maria TringaliNo ratings yet

- Covid-19 & 4IR and The Future of WorkDocument9 pagesCovid-19 & 4IR and The Future of WorkYahya HashmiNo ratings yet

- 2021 Report Thomson ReutersDocument20 pages2021 Report Thomson ReutersCiências CriminaisNo ratings yet

- Allianz Risk Barometer 2021Document26 pagesAllianz Risk Barometer 2021Alex DumiNo ratings yet

- PWC The Future of Financial ServicesDocument27 pagesPWC The Future of Financial ServicesPhương TrầnNo ratings yet

- European Management Journal: Joseph Amankwah-Amoah, Zaheer Khan, Geoffrey WoodDocument6 pagesEuropean Management Journal: Joseph Amankwah-Amoah, Zaheer Khan, Geoffrey WoodHamza TahirNo ratings yet

- In Conversation The Impact of Covid 19 On Capital MarketsDocument8 pagesIn Conversation The Impact of Covid 19 On Capital MarketsKato AkikoNo ratings yet

- Allianz Risk Barometer 2020Document24 pagesAllianz Risk Barometer 2020ivanhoNo ratings yet

- Journal of Banking & Finance: Roland Gillet, Georges Hübner, Séverine PlunusDocument12 pagesJournal of Banking & Finance: Roland Gillet, Georges Hübner, Séverine PlunuspmtunNo ratings yet

- Covid 19 Learnings Final v2Document15 pagesCovid 19 Learnings Final v2Xaidi axrinNo ratings yet

- Understanding The Sector Impact of COVID-19: Mining & MetalsDocument2 pagesUnderstanding The Sector Impact of COVID-19: Mining & MetalsRashi VajaniNo ratings yet

- The Impact of COVID 19 On Capital Markets One Year in PDFDocument8 pagesThe Impact of COVID 19 On Capital Markets One Year in PDFRhenyAANo ratings yet

- State of The Financial Services Industry Report 2015Document24 pagesState of The Financial Services Industry Report 2015Aditi KohliNo ratings yet

- Operational Risk Assessment - ConocoPhillipsDocument5 pagesOperational Risk Assessment - ConocoPhillipsHardik ThackerNo ratings yet

- Focus: Enterprise Risk Management (ERM)Document72 pagesFocus: Enterprise Risk Management (ERM)pressbureauNo ratings yet

- Dying IndustriesDocument6 pagesDying IndustriesBilgin YazarNo ratings yet

- Research Prop Covid-1Document7 pagesResearch Prop Covid-1VinayNo ratings yet

- The MiFID II Framework: How the New Standards Are Reshaping the Investment IndustryFrom EverandThe MiFID II Framework: How the New Standards Are Reshaping the Investment IndustryNo ratings yet

- Lecture Notes Unit 1 2014Document8 pagesLecture Notes Unit 1 2014Peter Jean-jacquesNo ratings yet

- Retail Market Conduct Task Force Report Initial Findings and Observations About The Impact of COVID-19 On Retail Market ConductDocument30 pagesRetail Market Conduct Task Force Report Initial Findings and Observations About The Impact of COVID-19 On Retail Market ConductTarbNo ratings yet

- COVID-19 Impact Towards Different IndustriesDocument48 pagesCOVID-19 Impact Towards Different IndustriesAnuruddha Rajasuriya100% (1)

- Anatomy and Impact of BriberyDocument13 pagesAnatomy and Impact of BriberyMarie SalukvadzeNo ratings yet

- PWC PWC Industry Spotlight An Oil and Gas Industry Focus On Covid 19 Accounting ConsiderationsDocument4 pagesPWC PWC Industry Spotlight An Oil and Gas Industry Focus On Covid 19 Accounting Considerationssyed2801No ratings yet

- Business EthicsDocument31 pagesBusiness EthicsFahim HossainNo ratings yet

- Shen-The Impact of The COVID - 19 Pandemic On Firm Performance. Emerging Markets Finance and TradeDocument19 pagesShen-The Impact of The COVID - 19 Pandemic On Firm Performance. Emerging Markets Finance and TradeIhsan FajrulNo ratings yet

- Accenture 10 Ways COVID 19 Impacting PaymentsDocument30 pagesAccenture 10 Ways COVID 19 Impacting PaymentsShweta TomarNo ratings yet

- ERM and ORMDocument11 pagesERM and ORMNarasimha Rao IthamsettyNo ratings yet

- Understanding The Sector Impact of COVID-19: Oil, Gas & ChemicalsDocument2 pagesUnderstanding The Sector Impact of COVID-19: Oil, Gas & ChemicalsperelapelNo ratings yet

- The Impactofthe COVID19 Pandemicon Firm PerformanceDocument20 pagesThe Impactofthe COVID19 Pandemicon Firm PerformanceやたなあはあやたNo ratings yet

- Cash Flow ManagementDocument10 pagesCash Flow Managementmamman64No ratings yet

- How Payments Can Adjust To The Coronavirus Pandemic and Help The World AdaptDocument10 pagesHow Payments Can Adjust To The Coronavirus Pandemic and Help The World AdaptMaría Victoria AlbanesiNo ratings yet

- The Top 10 Risks For Oil and GasDocument24 pagesThe Top 10 Risks For Oil and GasMsm MannNo ratings yet

- Assesment 2Document13 pagesAssesment 2Marian ValentinNo ratings yet

- Shaping The Battleground For GS100 SPDocument3 pagesShaping The Battleground For GS100 SPGlobalServicesNo ratings yet

- Impact of Finance & Accounting On The Energy IndustryDocument2 pagesImpact of Finance & Accounting On The Energy IndustryJubril_A_DaviesNo ratings yet

- Risk and ComplianceDocument10 pagesRisk and ComplianceCTRM CenterNo ratings yet

- Emerging DisruptorsDocument41 pagesEmerging DisruptorsDRIP HARDLYNo ratings yet

- Understanding Regtech For Digital Regulatory Compliance: Tom Butler and Leona O'BrienDocument18 pagesUnderstanding Regtech For Digital Regulatory Compliance: Tom Butler and Leona O'BrienjNo ratings yet

- Accenture Corporate Crisis ManagementDocument16 pagesAccenture Corporate Crisis Managementmukosino100% (1)

- JF Wicklow Sept04Document17 pagesJF Wicklow Sept04Prem KumarNo ratings yet

- Global Financial Crisis and COVID-19 Industrial ReactionsDocument32 pagesGlobal Financial Crisis and COVID-19 Industrial ReactionsLorena Galindo GuerreroNo ratings yet

- Forbes Insights Future of ManufacturingDocument18 pagesForbes Insights Future of Manufacturinggamil2No ratings yet

- Maharshi Dayanand University, Rohtak: Assignment OnDocument7 pagesMaharshi Dayanand University, Rohtak: Assignment Onashok kumarNo ratings yet

- Solution 3500.editedDocument18 pagesSolution 3500.editedRashika RoyNo ratings yet

- Chapter 12 - Macroeconomic and Industry AnalysisDocument8 pagesChapter 12 - Macroeconomic and Industry AnalysisMarwa HassanNo ratings yet

- Chapter 12 - Macroeconomic and Industry AnalysisDocument8 pagesChapter 12 - Macroeconomic and Industry AnalysisMarwa HassanNo ratings yet

- Chapter 12 - Macroeconomic and Industry AnalysisDocument8 pagesChapter 12 - Macroeconomic and Industry AnalysisMarwa HassanNo ratings yet

- Risk Report 2021Document18 pagesRisk Report 2021GDIAZNo ratings yet

- South Africa - Country Report 2023Document8 pagesSouth Africa - Country Report 2023Leon BurgerNo ratings yet

- The Economist (Intelligence Unit) - Trade and Investment Challenges and Opportunities in The Post-Pandemic World (2021Document24 pagesThe Economist (Intelligence Unit) - Trade and Investment Challenges and Opportunities in The Post-Pandemic World (2021tafakaraNo ratings yet

- The 2020 Wolters Kluwer Future Ready Lawyer: Performance DriversDocument26 pagesThe 2020 Wolters Kluwer Future Ready Lawyer: Performance DriversaegeanxNo ratings yet

- Notes3 1 7Document7 pagesNotes3 1 7ramNo ratings yet

- HMSP - Public Expose - 3Q2020Document19 pagesHMSP - Public Expose - 3Q2020Ershad SNo ratings yet

- COVID EditedDocument4 pagesCOVID EditedAron NgetichNo ratings yet

- ECON440 Project Group1Document14 pagesECON440 Project Group1hamzaNo ratings yet

- The European Insurance Industry: A PEST Analysis: Financial StudiesDocument20 pagesThe European Insurance Industry: A PEST Analysis: Financial StudiesAnonymous fRXyPY3No ratings yet

- Corporate RestructuringDocument41 pagesCorporate RestructuringAjmal KhanNo ratings yet

- 3017 Tutorial 9 SolutionsDocument4 pages3017 Tutorial 9 SolutionsNguyễn Hải100% (1)

- Letter of AcceptanceDocument2 pagesLetter of AcceptanceDisha DarjiNo ratings yet

- Lum Chang Technical BrochureDocument68 pagesLum Chang Technical BrochureBatu GajahNo ratings yet

- "E20" Surface Mount Productivity Improvement Project - Phase 1Document51 pages"E20" Surface Mount Productivity Improvement Project - Phase 1JAYANT SINGHNo ratings yet

- Assessment Task 1-2 Workbook-Bsbcrt512-Bsb50420-Cycle A-Edu Nomad-V1.0 2023Document17 pagesAssessment Task 1-2 Workbook-Bsbcrt512-Bsb50420-Cycle A-Edu Nomad-V1.0 2023Sujal KutalNo ratings yet

- Consumer Behaviour Swiggy ZomatoDocument11 pagesConsumer Behaviour Swiggy ZomatowhoreNo ratings yet

- LISTENING Countries in The WorldDocument6 pagesLISTENING Countries in The WorldVân KhánhNo ratings yet

- M3 - Run Checklist (MUDA, MURI, MURA) : M3 - Topic What Do You See? (Issue) How To Improve (Action)Document3 pagesM3 - Run Checklist (MUDA, MURI, MURA) : M3 - Topic What Do You See? (Issue) How To Improve (Action)abhasNo ratings yet

- A Case Study Analysis of The Montreal (CANADA) Chapter of The Hells Angels Outlaw Motorcycle Club (HAMC) (1995-2010) : Applying The Crime Business Analysis Matrix (CBAM)Document22 pagesA Case Study Analysis of The Montreal (CANADA) Chapter of The Hells Angels Outlaw Motorcycle Club (HAMC) (1995-2010) : Applying The Crime Business Analysis Matrix (CBAM)Ryan29No ratings yet

- Sample Barangay BudgetDocument17 pagesSample Barangay Budgetnilo bia100% (4)

- Hilton Hotels - Brand Differentiation Through Customer RelationshipDocument11 pagesHilton Hotels - Brand Differentiation Through Customer RelationshipYash Pratap SinghNo ratings yet

- Research On Fastrack WatchesDocument23 pagesResearch On Fastrack Watcheskk_kamal40% (5)

- Habtamu SerteDocument17 pagesHabtamu SerteAklilu GirmaNo ratings yet

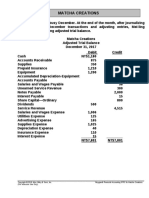

- MC4 Matcha Creations: (For Instructor Use Only)Document2 pagesMC4 Matcha Creations: (For Instructor Use Only)Reza eka PutraNo ratings yet

- 大萧条:历史与经验Document54 pages大萧条:历史与经验吴宙航No ratings yet

- Web NotificationDocument8 pagesWeb NotificationMaitri Auto Electrical East AfricaNo ratings yet

- 8 General Foods v. NACOCODocument3 pages8 General Foods v. NACOCOShaula FlorestaNo ratings yet

- Study Regarding Innovation and Entrepreneurship in Romanian SmesDocument6 pagesStudy Regarding Innovation and Entrepreneurship in Romanian SmesAlex ObrejanNo ratings yet

- MCom - Accounts ch-13 Topic3Document19 pagesMCom - Accounts ch-13 Topic3Sameer GoyalNo ratings yet

- Commercial Law Reviewer, MercantileDocument60 pagesCommercial Law Reviewer, MercantilecelestezerosevenNo ratings yet

- Vansh Course Prospectous 12 Feb 2021Document8 pagesVansh Course Prospectous 12 Feb 2021Komal S.No ratings yet

- AC415 Fixed Variable Costs BreakEven 1 - 11 - 2017Document35 pagesAC415 Fixed Variable Costs BreakEven 1 - 11 - 2017blablaNo ratings yet

- Attempt All QuestionsDocument5 pagesAttempt All QuestionsApurva SrivastavaNo ratings yet

- SM SX 52 SpecificatonDocument2 pagesSM SX 52 SpecificatonAli HussnainNo ratings yet

- Artikel MMT Lisa Nilhuda 17002060Document7 pagesArtikel MMT Lisa Nilhuda 17002060Erlianaeka SaputriNo ratings yet

- Assignment of Contract (Correct Version)Document2 pagesAssignment of Contract (Correct Version)Heru Atiba El - BeyNo ratings yet

- DIVYA VISHWAKARMA Construction IndustryDocument87 pagesDIVYA VISHWAKARMA Construction IndustryNITISH CHANDRA PANDEYNo ratings yet

- Confusion of GoodsDocument1 pageConfusion of GoodsJames AndrinNo ratings yet

- Case Study 3: Fountain Pens LimitedDocument3 pagesCase Study 3: Fountain Pens Limitedtanya singh100% (1)

- Coti GIW Rep 26x28LSA PDFDocument3 pagesCoti GIW Rep 26x28LSA PDFjohan diazNo ratings yet

- 5.tender Process N DocumentationDocument35 pages5.tender Process N DocumentationDilanka MJ Dassanayake100% (1)