You might also like

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5813)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Citizens United FOIA Production #1 (Veterans Affairs - Biden Voting EO)Document90 pagesCitizens United FOIA Production #1 (Veterans Affairs - Biden Voting EO)Citizens UnitedNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Stetson 2005 ExamDocument11 pagesStetson 2005 ExamKeenan SmithNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Teaching Augustine PDFDocument181 pagesTeaching Augustine PDFKeenan SmithNo ratings yet

- Suggested Answers To The 2016 Bar Examination in Labor LawDocument12 pagesSuggested Answers To The 2016 Bar Examination in Labor Lawaliagamps411No ratings yet

- Local Government SystemDocument65 pagesLocal Government Systemshakeel100% (1)

- The Roles and Powers of The LEGISLATIVE BRANCH of The Philippine GovernmentDocument24 pagesThe Roles and Powers of The LEGISLATIVE BRANCH of The Philippine GovernmentroperNo ratings yet

- Remedies 2002 Model AnswersDocument9 pagesRemedies 2002 Model AnswersKeenan SmithNo ratings yet

- Intellectual Property Rights LawDocument26 pagesIntellectual Property Rights LawEthereal DNo ratings yet

- Constitutions, Statutes, and Administrative RegulationsDocument30 pagesConstitutions, Statutes, and Administrative RegulationsKeenan SmithNo ratings yet

- Stetson-2002 AnswerDocument12 pagesStetson-2002 AnswerKeenan SmithNo ratings yet

- Income Tax OutlineDocument20 pagesIncome Tax OutlineKeenan SmithNo ratings yet

- Criminal LAW Bulletin: Volume 46, Number 2Document12 pagesCriminal LAW Bulletin: Volume 46, Number 2Keenan SmithNo ratings yet

- Fall 2006 ExamDocument10 pagesFall 2006 ExamKeenan SmithNo ratings yet

- Lesson 18 PowerpointDocument10 pagesLesson 18 PowerpointKeenan SmithNo ratings yet

- Syllabus Updates: OK To Skip QP, BA & FactsDocument19 pagesSyllabus Updates: OK To Skip QP, BA & FactsKeenan SmithNo ratings yet

- Lesson 20 PowerpointDocument14 pagesLesson 20 PowerpointKeenan SmithNo ratings yet

- Jones V Golden PDFDocument7 pagesJones V Golden PDFKeenan SmithNo ratings yet

- United States District Court Southern District of Ohio Western DivisionDocument27 pagesUnited States District Court Southern District of Ohio Western DivisionKeenan SmithNo ratings yet

- Question Presented & Brief Answer: Jackson - Legal Writing - Fall 2019Document1 pageQuestion Presented & Brief Answer: Jackson - Legal Writing - Fall 2019Keenan SmithNo ratings yet

- Absolute and Qualified ImmunityDocument6 pagesAbsolute and Qualified ImmunityKeenan SmithNo ratings yet

- Endo PR Fall 2020 SyllabusDocument8 pagesEndo PR Fall 2020 SyllabusKeenan SmithNo ratings yet

- Substance v. Procedure ProblemDocument2 pagesSubstance v. Procedure ProblemKeenan SmithNo ratings yet

- 9 - GR No.225442-SPARK V Quezon CityDocument1 page9 - GR No.225442-SPARK V Quezon CityPamela Jane I. TornoNo ratings yet

- Agapay v. Palang, GR 116668, July 28, 1997Document18 pagesAgapay v. Palang, GR 116668, July 28, 1997Anna NicerioNo ratings yet

- Eng 7136Document4 pagesEng 7136sfsdfsdfsdfNo ratings yet

- Notes For MechDocument3 pagesNotes For MechShranish KarNo ratings yet

- Lankabangla Securities LTD.: Trade Confirmation Note (Summary)Document1 pageLankabangla Securities LTD.: Trade Confirmation Note (Summary)Mahi ZabeenNo ratings yet

- გაიქეცი პატარავ გაიქეცი PDFDocument260 pagesგაიქეცი პატარავ გაიქეცი PDFNino BerdzenishviliNo ratings yet

- Work Terms and ConditionsDocument3 pagesWork Terms and ConditionsYubaraj AcharyaNo ratings yet

- Recruitment For The Post of AssistantDocument4 pagesRecruitment For The Post of AssistantPradeep KumarNo ratings yet

- Rosencor Dev. Corp. v. Inquing, G.R. No. 140479Document10 pagesRosencor Dev. Corp. v. Inquing, G.R. No. 140479Shaula FlorestaNo ratings yet

- Subject: Issuance of Equivalence Certificate of MBA (3.5) To MBA/MS/M. PhillDocument1 pageSubject: Issuance of Equivalence Certificate of MBA (3.5) To MBA/MS/M. PhillAbdulBasitKhanSadozaiNo ratings yet

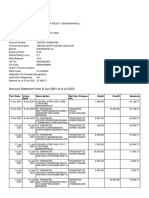

- Account Statement From 8 Jan 2021 To 8 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument16 pagesAccount Statement From 8 Jan 2021 To 8 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceMUTHYALA NEERAJANo ratings yet

- Starkville Dispatch Eedition 3-4-21Document12 pagesStarkville Dispatch Eedition 3-4-21The DispatchNo ratings yet

- 2018 Judgement 07-Mar-2019Document24 pages2018 Judgement 07-Mar-2019ajay kumarNo ratings yet

- Audit Plan: Note # 1Document6 pagesAudit Plan: Note # 1Audit Circle IV BhavnagarNo ratings yet

- Memo On Tree PlantingDocument6 pagesMemo On Tree Plantingjojo zamNo ratings yet

- Florentino v. Encarnacion G.R. No. L-27696, 30 September 1977 FactsDocument4 pagesFlorentino v. Encarnacion G.R. No. L-27696, 30 September 1977 FactsKNo ratings yet

- ADR Under Sec 89 of Civil Procedure Code, 1908: A Critical AnalysisDocument3 pagesADR Under Sec 89 of Civil Procedure Code, 1908: A Critical AnalysisSatyam SinghNo ratings yet

- OMBC Memoradum No. 2Document7 pagesOMBC Memoradum No. 2Shienna Divina GordoNo ratings yet

- Presentation JMCTIDocument42 pagesPresentation JMCTIyeyagoj460No ratings yet

- Pawar's Time of Reckoning - Outlook India MagazineDocument11 pagesPawar's Time of Reckoning - Outlook India MagazinelakshmankannaNo ratings yet

- Model-N-TR1EB SKD - 6090.199.009Document6 pagesModel-N-TR1EB SKD - 6090.199.009Wang Sze ShianNo ratings yet

- Law of CarriageDocument10 pagesLaw of CarriageSushree Swagatika BarikNo ratings yet

- NYPD Lieutenant Acquitted of Beating Girlfriend After OrgyDocument1 pageNYPD Lieutenant Acquitted of Beating Girlfriend After Orgyedwinbramosmac.comNo ratings yet

- Reyes vs. Enriquez Reyes vs. EnriquezDocument11 pagesReyes vs. Enriquez Reyes vs. EnriquezSamantha AdduruNo ratings yet

- Dont Ask Dont TellDocument4 pagesDont Ask Dont TellEmily CoxNo ratings yet