You might also like

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Cost-Volume Profit AnalysisDocument26 pagesCost-Volume Profit AnalysisClarizza20% (5)

- Chapter 4Document9 pagesChapter 4limenih100% (1)

- Bac 300 Lesson ThreeDocument15 pagesBac 300 Lesson ThreejjjjNo ratings yet

- CH - 1 CVP AnalysisDocument7 pagesCH - 1 CVP AnalysisMahlet AbrahaNo ratings yet

- MAS 2017 01 Management Accounting Concepts Techniques For Planning and ControlDocument5 pagesMAS 2017 01 Management Accounting Concepts Techniques For Planning and ControlMitch Delgado EmataNo ratings yet

- If There Is An Increase In.... Then Profit Tends To......Document5 pagesIf There Is An Increase In.... Then Profit Tends To......glcpaNo ratings yet

- Cost Behavior Patterns & CVP Analysis: Chapter SixDocument9 pagesCost Behavior Patterns & CVP Analysis: Chapter Sixabraha gebruNo ratings yet

- CMA II - Chapter 1, CVP RelationshipsDocument46 pagesCMA II - Chapter 1, CVP RelationshipsLakachew GetasewNo ratings yet

- Operating and Financial LeverageDocument36 pagesOperating and Financial LeverageKiena AnthiaNo ratings yet

- (At) 01 - Preface, Framework, EtcDocument8 pages(At) 01 - Preface, Framework, EtcCykee Hanna Quizo LumongsodNo ratings yet

- Chapter - One Cost-Volume-Profit AnalysisDocument13 pagesChapter - One Cost-Volume-Profit Analysisliyneh mebrahituNo ratings yet

- Cost Volume Profit Analysis: F. M. KapepisoDocument19 pagesCost Volume Profit Analysis: F. M. KapepisosimsonNo ratings yet

- CVP AnalysisDocument37 pagesCVP Analysis20B81A1235cvr.ac.in G RUSHI BHARGAVNo ratings yet

- Modified Internal Rate of Return and Accounting Rate of ReturnDocument51 pagesModified Internal Rate of Return and Accounting Rate of ReturnKarishma ChaudharyNo ratings yet

- Cost Volume Profit (CVP) Analysis-Final NoteDocument9 pagesCost Volume Profit (CVP) Analysis-Final NoteJuan Kerma100% (1)

- ACCTG 42 Module 3Document5 pagesACCTG 42 Module 3Hazel Grace PaguiaNo ratings yet

- Cost-Volume-Profit Relationships 2Document57 pagesCost-Volume-Profit Relationships 2Princess Jay NacorNo ratings yet

- H05. MAS03-CVPAnalysisDocument39 pagesH05. MAS03-CVPAnalysisShiela RengelNo ratings yet

- Break Even: IS4103 - Module 4Document22 pagesBreak Even: IS4103 - Module 4Aliah HadjirulNo ratings yet

- Cost Volume Profit (CVP) AnalysisDocument60 pagesCost Volume Profit (CVP) AnalysisEtsub SamuelNo ratings yet

- F5-CVP-1 AccaDocument10 pagesF5-CVP-1 AccaAmna HussainNo ratings yet

- MGMT Science Notes 03 CVP AnalysisDocument8 pagesMGMT Science Notes 03 CVP AnalysismichelleNo ratings yet

- Mas-02: Cost-Volume-Profit (CVP) Analysis: If There Is An Increase in Then Profit Tends ToDocument3 pagesMas-02: Cost-Volume-Profit (CVP) Analysis: If There Is An Increase in Then Profit Tends ToClint AbenojaNo ratings yet

- Session 12 CVP AnalysisDocument52 pagesSession 12 CVP Analysismuskan mittalNo ratings yet

- Chapter Three CVP AnalysisDocument65 pagesChapter Three CVP AnalysisBettyNo ratings yet

- Chapter - One Cost - Volume - Profit (CVP) Analysis: St. Mary's University, Faculty of Accounting and FinanceDocument8 pagesChapter - One Cost - Volume - Profit (CVP) Analysis: St. Mary's University, Faculty of Accounting and FinanceshimelisNo ratings yet

- Bingcang & Tamon (CVP, Module 5)Document67 pagesBingcang & Tamon (CVP, Module 5)FayehAmantilloBingcangNo ratings yet

- Chapter - One Cost-Volume-Profit AnalysisDocument10 pagesChapter - One Cost-Volume-Profit Analysisabateneh sintayehuNo ratings yet

- CVP StudentsDocument21 pagesCVP StudentsrbnbalachandranNo ratings yet

- Lecture 4b Cost Volume Profit EditedDocument24 pagesLecture 4b Cost Volume Profit EditedJinnie QuebrarNo ratings yet

- Topic 11 - Cost Volume Profit Analysis - LectureDocument23 pagesTopic 11 - Cost Volume Profit Analysis - LectureshamimahNo ratings yet

- CVP PDFDocument20 pagesCVP PDFChelsy SantosNo ratings yet

- Cost II Chap 1Document10 pagesCost II Chap 1abelNo ratings yet

- Cost II Chapter-OneDocument10 pagesCost II Chapter-OneSemiraNo ratings yet

- This Study Resource Was: San Sebastian College - RecoletosDocument4 pagesThis Study Resource Was: San Sebastian College - RecoletosNhel AlvaroNo ratings yet

- Agenda:: A Little More Vocabulary C-V-P Analysis Thursday's Class Group Problem SolvingDocument33 pagesAgenda:: A Little More Vocabulary C-V-P Analysis Thursday's Class Group Problem SolvingApoorvNo ratings yet

- Operating and Financial LeverageDocument43 pagesOperating and Financial LeverageMARIBEL SANTOSNo ratings yet

- Break Even: Engineering Economics - Session 9 Last SessionDocument23 pagesBreak Even: Engineering Economics - Session 9 Last Sessionmark floresNo ratings yet

- William Wenceslao - BA 202 Topic 6 Assignment - BY WILLDocument4 pagesWilliam Wenceslao - BA 202 Topic 6 Assignment - BY WILLWiLliamLoquiroWencesLaoNo ratings yet

- MODULE 2 CVP AnalysisDocument8 pagesMODULE 2 CVP Analysissharielles /No ratings yet

- Cac Chapter 4Document14 pagesCac Chapter 4DecimNo ratings yet

- Chapter 5Document40 pagesChapter 5endashaw debruNo ratings yet

- Cost Profit Volume AnalysisDocument28 pagesCost Profit Volume AnalysisClarice LangitNo ratings yet

- Operating and Financial LeverageDocument52 pagesOperating and Financial Leveragepangilinanac00No ratings yet

- Management Accounting: Breakeven AnalysisDocument27 pagesManagement Accounting: Breakeven Analysislakshmi aparna yelganamoniNo ratings yet

- CAC CHAPTER 4 - For MergeDocument23 pagesCAC CHAPTER 4 - For MergeDecimNo ratings yet

- CMA PlanDocument113 pagesCMA PlanYash Gandhi- 370No ratings yet

- HANDOUT CVP Methods of Acct TeachingDocument4 pagesHANDOUT CVP Methods of Acct TeachingMalesia AlmojuelaNo ratings yet

- Module 4 Cost Volume Profit AnalysisDocument6 pagesModule 4 Cost Volume Profit AnalysisJackielyn RavinaNo ratings yet

- BEP ExercisesDocument11 pagesBEP ExercisesBarack MikeNo ratings yet

- Cost Volume Profit AnalysisDocument7 pagesCost Volume Profit AnalysisMeng DanNo ratings yet

- Chapter 6 (Part I) Cost-Volume-Profit Analysis: A Simple Model For Planning & Decision-MakingDocument10 pagesChapter 6 (Part I) Cost-Volume-Profit Analysis: A Simple Model For Planning & Decision-MakingKhaled Abo YousefNo ratings yet

- Module 4Document42 pagesModule 4Eshael FathimaNo ratings yet

- Cost - Volume - Profit Analysis - CLASSDocument8 pagesCost - Volume - Profit Analysis - CLASSsaidkhatib368No ratings yet

- Day 3Document33 pagesDay 3Leo ApilanNo ratings yet

- Management Accounting NotesDocument8 pagesManagement Accounting NotesNafiz RahmanNo ratings yet

- 1 CVP RelationshipDocument22 pages1 CVP RelationshipmedrekNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- ARTA 111 - Elements and Principles of ArtDocument67 pagesARTA 111 - Elements and Principles of ArtJomari GavinoNo ratings yet

- ARTA 111 Assumptions and Nature of ArtDocument12 pagesARTA 111 Assumptions and Nature of ArtJomari GavinoNo ratings yet

- Session 4 - Saving, Investment & The Financial SystemDocument29 pagesSession 4 - Saving, Investment & The Financial SystemViviene Seth Alvarez LigonNo ratings yet

- ARTA 111 Introduction and Overview of ArtDocument19 pagesARTA 111 Introduction and Overview of ArtJomari Gavino100% (1)

- ARTA 111 - Functions of Art and PhilosophyDocument17 pagesARTA 111 - Functions of Art and PhilosophyViviene Seth Alvarez LigonNo ratings yet

- ARTA 111 Subject and ContentDocument15 pagesARTA 111 Subject and ContentJomari GavinoNo ratings yet

- Session 3 - Production and GrowthDocument27 pagesSession 3 - Production and GrowthViviene Seth Alvarez LigonNo ratings yet

- Session 5 - Basic Tools of FinanceDocument17 pagesSession 5 - Basic Tools of FinanceViviene Seth Alvarez LigonNo ratings yet

- Session 6 - Inflation & UnemploymentDocument29 pagesSession 6 - Inflation & UnemploymentViviene Seth Alvarez LigonNo ratings yet

- 11pert CPMDocument18 pages11pert CPMViviene Seth Alvarez LigonNo ratings yet

- Edev 311: Economic Development: Session 2: Measuring The National Income Accounts and Cost of LivingDocument34 pagesEdev 311: Economic Development: Session 2: Measuring The National Income Accounts and Cost of LivingCarlNo ratings yet

- Linear Equations and InequalitiesDocument10 pagesLinear Equations and InequalitiesViviene Seth Alvarez LigonNo ratings yet

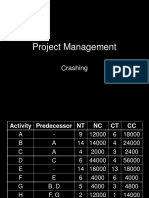

- CrashingDocument33 pagesCrashingViviene Seth Alvarez LigonNo ratings yet

- Pert CPMDocument33 pagesPert CPMViviene Seth Alvarez LigonNo ratings yet

- Linear Programming - Simplex MethodDocument22 pagesLinear Programming - Simplex MethodViviene Seth Alvarez LigonNo ratings yet

- Quantitative TechniquesDocument34 pagesQuantitative TechniquesViviene Seth Alvarez LigonNo ratings yet

- Msci111Document18 pagesMsci111Viviene Seth Alvarez LigonNo ratings yet

- Communication Aids and Strategies Using Tools of Technology 1Document29 pagesCommunication Aids and Strategies Using Tools of Technology 1Viviene Seth Alvarez Ligon80% (5)

- Cost-Volume-Profit Analysis - Sample ProblemsDocument1 pageCost-Volume-Profit Analysis - Sample ProblemsViviene Seth Alvarez LigonNo ratings yet

- Research ProposalDocument2 pagesResearch Proposalsmh9662No ratings yet

- BBC Learning English - 6 Minute English - Bitcoin - Digital Crypto-CurrencyDocument38 pagesBBC Learning English - 6 Minute English - Bitcoin - Digital Crypto-CurrencyMohamad GhafooryNo ratings yet

- S.NO. Students Name Contact Number CAP 10TH: Ideal Institute of Pharamacy, Wada SESSION-2020-21Document12 pagesS.NO. Students Name Contact Number CAP 10TH: Ideal Institute of Pharamacy, Wada SESSION-2020-21DAMBALENo ratings yet

- EPB2.4 + V3f20 Installation - Start-Up ProcDocument30 pagesEPB2.4 + V3f20 Installation - Start-Up ProcBeltran Héctor75% (4)

- ART Threaded Fastener Design and AnalysisDocument40 pagesART Threaded Fastener Design and AnalysisAarón Escorza MistránNo ratings yet

- Structural Analysis of English SyntaxDocument26 pagesStructural Analysis of English SyntaxremovableNo ratings yet

- RTI SpicesDocument226 pagesRTI SpicesvivebajajNo ratings yet

- 7-Drug Delivery Systems 3Document26 pages7-Drug Delivery Systems 3Ibrahim Al ShantiNo ratings yet

- Language - Introduction To The Integrated Language Arts CompetenciesDocument7 pagesLanguage - Introduction To The Integrated Language Arts CompetenciesHari Ng Sablay100% (1)

- Lecture - 1 - UNDERGROUND MINE DESIGNDocument59 pagesLecture - 1 - UNDERGROUND MINE DESIGNRahat fahimNo ratings yet

- But Flee Youthful Lusts - pdf2Document2 pagesBut Flee Youthful Lusts - pdf2emmaboakye2fNo ratings yet

- Asme B30.26 (2004)Document38 pagesAsme B30.26 (2004)Omar RamirezNo ratings yet

- The Trend Trader Nick Radge On Demand PDFDocument8 pagesThe Trend Trader Nick Radge On Demand PDFDedi Tri LaksonoNo ratings yet

- EKOFLUID PRODUCT SHEET FILOIL 6000 210x297 EN WEBDocument4 pagesEKOFLUID PRODUCT SHEET FILOIL 6000 210x297 EN WEBjunaidi.036No ratings yet

- Tata Steel LTD.: Elements Unit Min Max RemarksDocument2 pagesTata Steel LTD.: Elements Unit Min Max RemarksPavan KumarNo ratings yet

- HLSS 310 Critical Infrastructure ProtectionDocument12 pagesHLSS 310 Critical Infrastructure ProtectionMoffat HarounNo ratings yet

- Arid Agriculture University, RawalpindiDocument4 pagesArid Agriculture University, RawalpindiIsHa KhAnNo ratings yet

- Short Stories Planet Earth AnswersDocument2 pagesShort Stories Planet Earth AnswersLina Vasquez Vasquez100% (2)

- Management From RamayanaDocument14 pagesManagement From Ramayanasaaket batchuNo ratings yet

- Upfc PlacementDocument0 pagesUpfc PlacementVamsi KumarNo ratings yet

- How To Draw The Platform Business Model Map-David RogersDocument5 pagesHow To Draw The Platform Business Model Map-David RogersworkneshNo ratings yet

- Dunhill The Old WindmillDocument2 pagesDunhill The Old WindmillMaría Hernández MiraveteNo ratings yet

- Functional Plant Manager 2. Geographical Vice PresidentDocument5 pagesFunctional Plant Manager 2. Geographical Vice PresidentVic FranciscoNo ratings yet

- Plot Elements - DisneyDocument23 pagesPlot Elements - DisneyssssssNo ratings yet

- Generation Transmission and Distribution Notes.Document88 pagesGeneration Transmission and Distribution Notes.Abhishek NirmalkarNo ratings yet

- Scania DC12 Operator's ManualDocument65 pagesScania DC12 Operator's ManualAlex Renne Chambi100% (3)

- eLearnMarkets OptionsBuying HindiDocument17 pageseLearnMarkets OptionsBuying Hindisrinivas20% (1)

- Securing Your Organization From Modern Ransomware: Ransomware Attacks Are Now A Team EffortDocument11 pagesSecuring Your Organization From Modern Ransomware: Ransomware Attacks Are Now A Team EfforttiagouebemoraisNo ratings yet

- The DAMA Guide To The Data Management Body of Knowledge - First EditionDocument430 pagesThe DAMA Guide To The Data Management Body of Knowledge - First Editionkakarotodesu100% (10)

- Mum LatecityDocument14 pagesMum LatecityGkiniNo ratings yet