You might also like

- ExportDocument25 pagesExportBala VinayagamNo ratings yet

- Assignment: Topic: - Summon in Civil SuitDocument12 pagesAssignment: Topic: - Summon in Civil SuitMOHAMAMD ZIYA ANSARINo ratings yet

- Concept of Appeal Under GSTDocument24 pagesConcept of Appeal Under GSTSUFIYAN SIDDIQUINo ratings yet

- Suits by An Indigent PersonDocument12 pagesSuits by An Indigent PersonAshmit Kumar AggarwalNo ratings yet

- India's Constitutional Framework for Taxation PowersDocument13 pagesIndia's Constitutional Framework for Taxation PowersDeepesh SinghNo ratings yet

- Oral and Documentary Evidence (Rajveer)Document17 pagesOral and Documentary Evidence (Rajveer)Abhimanyu SinghNo ratings yet

- Winding Up and Liquidation Under IBCDocument15 pagesWinding Up and Liquidation Under IBCTaruna Shandilya100% (1)

- Agrani EvidenceDocument8 pagesAgrani EvidenceVirupaksh SinghNo ratings yet

- Gurughasidas Central University, Bilaspur: "Power and Duties of Income-Tax Authorities"Document20 pagesGurughasidas Central University, Bilaspur: "Power and Duties of Income-Tax Authorities"Kishori PatelNo ratings yet

- Viability of Class Division While Accessing Tax - An Appraisal Dr. Ram Manohar Lohia National Law UniversityDocument16 pagesViability of Class Division While Accessing Tax - An Appraisal Dr. Ram Manohar Lohia National Law UniversityHimanshumalikNo ratings yet

- Taxation Law ProjectDocument15 pagesTaxation Law Projectraj vardhan agarwalNo ratings yet

- Evidence Law ProjectDocument17 pagesEvidence Law ProjectHrithik KaulNo ratings yet

- Anti Profiteering GSTDocument15 pagesAnti Profiteering GSTRishika JainNo ratings yet

- Registration Under GSTDocument19 pagesRegistration Under GSTHappyNo ratings yet

- Dr. Ram Manohar Lohiya National Law University, Lucknow: Cademic Ession RojectDocument15 pagesDr. Ram Manohar Lohiya National Law University, Lucknow: Cademic Ession RojectVarad Arun YadavNo ratings yet

- Rent Agreement SHOP NO.1, IN PROP NO - WZ-48-4D, KRISHNA PARK EXTN.Document4 pagesRent Agreement SHOP NO.1, IN PROP NO - WZ-48-4D, KRISHNA PARK EXTN.Jagparvesh SharmaNo ratings yet

- Procedure To Be Adopted in Warrant Cases Instituted On Police ReportDocument3 pagesProcedure To Be Adopted in Warrant Cases Instituted On Police ReportRachna YadavNo ratings yet

- GST - Concept and Constitutional FrameworkDocument9 pagesGST - Concept and Constitutional FrameworkarmsarivuNo ratings yet

- Capital GainsDocument8 pagesCapital GainsSarfaraz Singh LegaNo ratings yet

- Dr. Ram Manohar Lohiya National Law University, LucknowDocument14 pagesDr. Ram Manohar Lohiya National Law University, LucknowbhanwatiNo ratings yet

- Llmsy Lab 1 SarlaDocument25 pagesLlmsy Lab 1 SarlaHari KiranNo ratings yet

- Ms. Kuhu Tiwari: Hidayatullah National Law UniversityDocument20 pagesMs. Kuhu Tiwari: Hidayatullah National Law UniversityNaveen SihareNo ratings yet

- GST Refund Under Tax Laws: An Analysis: Hidayatullah National Law University Raipur (C.G.)Document20 pagesGST Refund Under Tax Laws: An Analysis: Hidayatullah National Law University Raipur (C.G.)Atul VermaNo ratings yet

- Assignment On Critical Analysis of Written StatementDocument25 pagesAssignment On Critical Analysis of Written Statementdivya srivastavaNo ratings yet

- Ational LAW University Odisha Cuttack: Topic: Law of MaintainanceDocument18 pagesAtional LAW University Odisha Cuttack: Topic: Law of Maintainancearsh singhNo ratings yet

- Determination of Mesne Profits Under CPCDocument17 pagesDetermination of Mesne Profits Under CPCDev DubeyNo ratings yet

- Protection of WomenDocument20 pagesProtection of Womenaamir raza khanNo ratings yet

- External AidsDocument5 pagesExternal AidsShashikantSauravBarnwalNo ratings yet

- Name of The Student Roll No. Semester: Name of The Program: 5 Year (B.A., LL.B. / LL.M.)Document25 pagesName of The Student Roll No. Semester: Name of The Program: 5 Year (B.A., LL.B. / LL.M.)Roshan ShakNo ratings yet

- Jamia Millia Islamia: Project TitleDocument19 pagesJamia Millia Islamia: Project TitlePranavNo ratings yet

- Section 91 CPC public nuisance suitsDocument2 pagesSection 91 CPC public nuisance suitsBilal akbarNo ratings yet

- Constitutional Framework of GST in IndiaDocument20 pagesConstitutional Framework of GST in IndiaABNo ratings yet

- A Detailed Study of Winding Up of A CompanyDocument7 pagesA Detailed Study of Winding Up of A CompanyIJRASETPublicationsNo ratings yet

- HPNLU ADR Project Analyzes Section 89Document12 pagesHPNLU ADR Project Analyzes Section 89vaishali panchNo ratings yet

- Dr. Ram Manohar Lohiya National Law University, Lucknow: Subject: Law of Taxation SessionDocument14 pagesDr. Ram Manohar Lohiya National Law University, Lucknow: Subject: Law of Taxation SessionShivam MishraNo ratings yet

- Summons Trials in Criminal CasesDocument18 pagesSummons Trials in Criminal CasesOnindya MitraNo ratings yet

- CPC 1908 PDFDocument35 pagesCPC 1908 PDFJyot JawanNo ratings yet

- Investigation of Affairs of A CompanyDocument18 pagesInvestigation of Affairs of A CompanyGufran KhanNo ratings yet

- University of Petroleum & Energy Studies College of Legal StudiesDocument16 pagesUniversity of Petroleum & Energy Studies College of Legal StudiesPrachie SinghNo ratings yet

- Corporate Law IIDocument19 pagesCorporate Law IIIMRAN ALAMNo ratings yet

- Lot FDDocument16 pagesLot FDShikhar TandonNo ratings yet

- IPR AssignmentDocument11 pagesIPR AssignmentNishin ShrikhandeNo ratings yet

- Nature of Avocate's Right To PractiseDocument16 pagesNature of Avocate's Right To PractiseSurbhi Sharma100% (1)

- Compulsory Licensing and its Development in India and InternationallyDocument6 pagesCompulsory Licensing and its Development in India and InternationallyRohan NandyNo ratings yet

- Labour Law AbstractDocument22 pagesLabour Law AbstractSaniaNo ratings yet

- Admission As Defined Under Sec 17Document8 pagesAdmission As Defined Under Sec 17Rajdeep DuttaNo ratings yet

- This Term Paper / Assignment / Project Has Been Submitted byDocument15 pagesThis Term Paper / Assignment / Project Has Been Submitted byApoorvnujsNo ratings yet

- Agriculture IncomeDocument10 pagesAgriculture IncomeSatish Penumarthi100% (1)

- Cpc-2 Mohammad Javed MalikDocument19 pagesCpc-2 Mohammad Javed MalikSahil Ahmed JameiNo ratings yet

- Dying in Harness Rule Study for UP Public Sector JobsDocument327 pagesDying in Harness Rule Study for UP Public Sector JobsStanzin LakeshatNo ratings yet

- Able of OntentsDocument22 pagesAble of OntentsAmita SinwarNo ratings yet

- Of Musical Works.: Alliance School of Law Alliance University, Banglore Date of Submission: 7 APRIL2019Document15 pagesOf Musical Works.: Alliance School of Law Alliance University, Banglore Date of Submission: 7 APRIL2019Chrisbel RanjithNo ratings yet

- Faculty of Law Jamia Millia IslamiaDocument14 pagesFaculty of Law Jamia Millia IslamiaJin KnoxvilleNo ratings yet

- Suits by and Against The Government: Jamia Millia IslamiaDocument17 pagesSuits by and Against The Government: Jamia Millia IslamiaIMRAN ALAMNo ratings yet

- Administrative LawDocument4 pagesAdministrative LawShivam YadavNo ratings yet

- Dr. Ram Manohar Lohiya Nationa Law University: Subject-Real State Laws Project Topic - Land Acquisition vs. Land PoolingDocument15 pagesDr. Ram Manohar Lohiya Nationa Law University: Subject-Real State Laws Project Topic - Land Acquisition vs. Land Poolingkaran rawatNo ratings yet

- CPC 4th SemDocument20 pagesCPC 4th SemAmit SinghNo ratings yet

- CRPCDocument6 pagesCRPCsiddhantNo ratings yet

- Doli Incapax - A Provision Impairing Justice To ChildrenDocument14 pagesDoli Incapax - A Provision Impairing Justice To Childrenshivam jainNo ratings yet

- Tabish CRPCDocument23 pagesTabish CRPCAhmed ShujaNo ratings yet

- CRPC Project: Constitution and Hierarchy of Criminal Courts in IndiaDocument16 pagesCRPC Project: Constitution and Hierarchy of Criminal Courts in IndiaAhmed ShujaNo ratings yet

- ADR DISSERTATION CompleteDocument137 pagesADR DISSERTATION CompleteAhmed ShujaNo ratings yet

- Written StatementDocument1 pageWritten StatementAhmed ShujaNo ratings yet

- In The City Civil Court, at Agra Civil Suit No. 100 of 2002Document3 pagesIn The City Civil Court, at Agra Civil Suit No. 100 of 2002Ahmed ShujaNo ratings yet

- Proforma Cover Page Assignment JMIDocument1 pageProforma Cover Page Assignment JMIAhmed ShujaNo ratings yet

- Alternative Dispute Resolution Methods Post-Independence in IndiaDocument11 pagesAlternative Dispute Resolution Methods Post-Independence in IndiaAhmed ShujaNo ratings yet

- Tax Invoice: Signature Not VerifiedDocument1 pageTax Invoice: Signature Not VerifiedAhmed ShujaNo ratings yet

- Adr DilwarDocument136 pagesAdr DilwarAhmed ShujaNo ratings yet

- City of Manila vs. Coca-ColaDocument3 pagesCity of Manila vs. Coca-ColaAngel Agustine O. Japitan IINo ratings yet

- Certificate of Creditable Tax Withheld at Source: Kawanihan NG Rentas InternasDocument2 pagesCertificate of Creditable Tax Withheld at Source: Kawanihan NG Rentas InternasWeng Tuiza EstebanNo ratings yet

- Concept of Supply: Name-Jash Jain Roll-126Document21 pagesConcept of Supply: Name-Jash Jain Roll-126Tanisha DoshiNo ratings yet

- GST RegistrationDocument4 pagesGST RegistrationUnique Trans SystemNo ratings yet

- Direct TaxesDocument7 pagesDirect Taxessebastian mlingwaNo ratings yet

- NOLCODocument8 pagesNOLCOChristopher SantosNo ratings yet

- LDNID, Supplier Registration Form Ver. 5.2 (2020) - SignDocument1 pageLDNID, Supplier Registration Form Ver. 5.2 (2020) - SigniraNo ratings yet

- VAT, estate tax and donor's tax rulesDocument24 pagesVAT, estate tax and donor's tax rulesValierry VelascoNo ratings yet

- 2010-2015 Bar Tax Q&aDocument104 pages2010-2015 Bar Tax Q&aMicah Ruth PascuaNo ratings yet

- Maceda VS Macaraig, GR No 88291, May 31, 1981Document43 pagesMaceda VS Macaraig, GR No 88291, May 31, 1981KidMonkey2299No ratings yet

- Sl. No Description Unit Price Qty Net Amount Tax Rate Tax Type Tax Amount Total AmountDocument1 pageSl. No Description Unit Price Qty Net Amount Tax Rate Tax Type Tax Amount Total AmountAnirudhNo ratings yet

- Order details for Rs. 182 and Rs. 163 booksDocument2 pagesOrder details for Rs. 182 and Rs. 163 bookspgpm20 SANCHIT GARGNo ratings yet

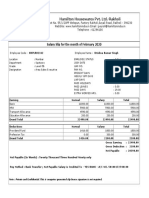

- Hamilton Housewares Pvt. Ltd.-Rakholi: Salary Slip For The Month of February 2020Document1 pageHamilton Housewares Pvt. Ltd.-Rakholi: Salary Slip For The Month of February 2020KRISHNA SINGHNo ratings yet

- Legal M e M o R A N D U MDocument3 pagesLegal M e M o R A N D U MmyrahjNo ratings yet

- Assessment of Vat Administration (A Case Study On Bishoftu Town)Document41 pagesAssessment of Vat Administration (A Case Study On Bishoftu Town)chalachew mekonnenNo ratings yet

- E-Commerce & Works Contracts, Right To Use, Restaurant-27.2.2017 (CA. Pritam Mahure)Document34 pagesE-Commerce & Works Contracts, Right To Use, Restaurant-27.2.2017 (CA. Pritam Mahure)PARESH KUVADIYANo ratings yet

- G.R. No. 147375 June 26, 2006 Commissioner of Internal Revenue, Petitioner, Bank of The Philippine Islands, RespondentDocument11 pagesG.R. No. 147375 June 26, 2006 Commissioner of Internal Revenue, Petitioner, Bank of The Philippine Islands, RespondentShie DiazNo ratings yet

- Manual Return 2023Document28 pagesManual Return 2023arsalanghuralgtNo ratings yet

- Indian Income Tax Return Acknowledgement 2021-22: Assessment YearDocument1 pageIndian Income Tax Return Acknowledgement 2021-22: Assessment YearneerajNo ratings yet

- 432HW5 KeyDocument6 pages432HW5 KeyJs ParkNo ratings yet

- HFC Digital TechnologiesDocument1 pageHFC Digital TechnologiesKarna Satish KumarNo ratings yet

- Netflix Vs Blockbuster Financials 10.30.22Document4 pagesNetflix Vs Blockbuster Financials 10.30.22Melissa ChanNo ratings yet

- Bengal Financial Statements AnalysisDocument1 pageBengal Financial Statements AnalysisTenghour LyNo ratings yet

- Cash BudgetDocument2 pagesCash BudgetSenthil Kumar0% (1)

- CIR v. Dash Engineering Phils., Inc., 712 SCRA 347 - THE LIFEBLOOD DOCTRINE - DigestDocument2 pagesCIR v. Dash Engineering Phils., Inc., 712 SCRA 347 - THE LIFEBLOOD DOCTRINE - DigestKate Garo100% (1)

- Tax Invoice: Edutech Mentor Mangrodih, Giridih 815302Document2 pagesTax Invoice: Edutech Mentor Mangrodih, Giridih 815302Sonu Kumar SinghNo ratings yet

- .Part - II - Sec.I - Direct TaxesDocument235 pages.Part - II - Sec.I - Direct TaxesJay Sangoi71% (7)

- AbideDocument1 pageAbideWisdom NyamhosvaNo ratings yet

- Service Tax Return 3in Excel Format-1Document8 pagesService Tax Return 3in Excel Format-1priyaradhiNo ratings yet

- BOI incentives for mass housing developersDocument20 pagesBOI incentives for mass housing developersRoseNo ratings yet