You might also like

- Introduction To Derivatives: Prof. Sudhakar ReddyDocument44 pagesIntroduction To Derivatives: Prof. Sudhakar ReddyHariSharanPanjwaniNo ratings yet

- Financial Risk Management with DerivativesDocument10 pagesFinancial Risk Management with DerivativesRoselle AlteriaNo ratings yet

- CH 4 Hedging and DerivativesDocument31 pagesCH 4 Hedging and DerivativesAbdii DhufeeraNo ratings yet

- Ch. 18 - Derivatives & Risk ManagementDocument58 pagesCh. 18 - Derivatives & Risk ManagementAngeline ManuelNo ratings yet

- MAF 675 Topic 1Document34 pagesMAF 675 Topic 1Abdul BatenNo ratings yet

- Derivatives - Cheat SheetDocument12 pagesDerivatives - Cheat SheetUchit MehtaNo ratings yet

- Future ContractsDocument25 pagesFuture ContractsvishalalluriNo ratings yet

- CH 2Document14 pagesCH 2SITI NABILAH OTHMANNo ratings yet

- Derivative Securities MarketDocument2 pagesDerivative Securities MarketClaudette BlanceNo ratings yet

- AFA 3e PPT Chap10Document79 pagesAFA 3e PPT Chap10Quỳnh NguyễnNo ratings yet

- Forward & Futures Forward & Futures Forward & FuturesDocument34 pagesForward & Futures Forward & Futures Forward & FuturesN ArunsankarNo ratings yet

- 3 - FD 2Document8 pages3 - FD 2Jaishree MBA2021MBNo ratings yet

- Alt To Invstment (Part II)Document9 pagesAlt To Invstment (Part II)महेंद्र सिंह राजपूतNo ratings yet

- Funds FinalsDocument5 pagesFunds FinalsSydney Miles MahinayNo ratings yet

- Basics of DerivativesDocument27 pagesBasics of DerivativesSweety PawarNo ratings yet

- Forward & Futures: Dr.N.Arunsankar Associate ProfessorDocument34 pagesForward & Futures: Dr.N.Arunsankar Associate ProfessorN ArunsankarNo ratings yet

- Unit - 2Document39 pagesUnit - 2DivyanshuNo ratings yet

- Currency Futures Trading GuideDocument18 pagesCurrency Futures Trading GuiderudraNo ratings yet

- Unit 2 FDDocument39 pagesUnit 2 FDraj kumarNo ratings yet

- File 1675671050219Document26 pagesFile 1675671050219Tamzid Ahmed AnikNo ratings yet

- AFA - 4e - PPT - Chap10 (For Students)Document56 pagesAFA - 4e - PPT - Chap10 (For Students)Cẩm Tú NguyễnNo ratings yet

- Managing Financial Risk with DerivativesDocument17 pagesManaging Financial Risk with DerivativesbaboabNo ratings yet

- Module 2 - Forwards & FuturesDocument84 pagesModule 2 - Forwards & FuturesSanjay PatilNo ratings yet

- 7 Equity Futures and Delta OneDocument65 pages7 Equity Futures and Delta OneBarry HeNo ratings yet

- Finance DocumentDocument2 pagesFinance DocumentLaukik 17No ratings yet

- Derivative 1Document39 pagesDerivative 1Heera JhaNo ratings yet

- Derivative MarketDocument15 pagesDerivative MarketKamran MehboobNo ratings yet

- Unit Vi: Financial Risk ManagementDocument23 pagesUnit Vi: Financial Risk Managementmtechvlsitd labNo ratings yet

- Chapter 1.2 FuturesDocument16 pagesChapter 1.2 FuturesAnkitaNo ratings yet

- IntroductionDocument50 pagesIntroductionCharityChanNo ratings yet

- Delivery PriceDocument29 pagesDelivery PricePremendra SahuNo ratings yet

- Financial Futures With Reference To NiftyDocument73 pagesFinancial Futures With Reference To Niftyjitendra jaushik75% (4)

- Introduction To DerivativesDocument14 pagesIntroduction To Derivativesking410No ratings yet

- 4 InterestRateFuturesDocument11 pages4 InterestRateFuturesSai KiranNo ratings yet

- Forwards & Futures: by Ajinkya Yadav (19020348002) MBA Ex - FinanceDocument25 pagesForwards & Futures: by Ajinkya Yadav (19020348002) MBA Ex - FinanceAjinkya YadavNo ratings yet

- Strategies in Stock MarketDocument30 pagesStrategies in Stock Marketaddi05No ratings yet

- FuturesDocument30 pagesFuturessoujee60No ratings yet

- Exchange Rates Foreign Investment International TradeDocument17 pagesExchange Rates Foreign Investment International TradeImtiaz HasanNo ratings yet

- Derivados 2Document26 pagesDerivados 2carlosNo ratings yet

- 4 InterestRateFuturesDocument11 pages4 InterestRateFuturesShivani Patnaik RajetiNo ratings yet

- CH 1Document16 pagesCH 1SITI NABILAH OTHMANNo ratings yet

- DerivadosDocument32 pagesDerivadoscarlosNo ratings yet

- Green Retro Markets and Finance Presentation - 20240213 - 085823 - 0000Document44 pagesGreen Retro Markets and Finance Presentation - 20240213 - 085823 - 0000Riza Mae AzulNo ratings yet

- Derivatives & AIDocument16 pagesDerivatives & AISneha GaggarNo ratings yet

- Lecture 3.3 - CMDocument59 pagesLecture 3.3 - CMOlga SlaninaNo ratings yet

- Guide to Financial DerivativesDocument13 pagesGuide to Financial DerivativesRakshita AngadiNo ratings yet

- Introduction To DerivativesDocument49 pagesIntroduction To DerivativesPhương TrinhNo ratings yet

- Legal Concepts Lecture (5) - DerivativesDocument77 pagesLegal Concepts Lecture (5) - DerivativesEusebio Olindo Lopez SamudioNo ratings yet

- Derivatives Market GuideDocument21 pagesDerivatives Market Guidesejalahir30_40759023No ratings yet

- Introduction to Derivatives MarketsDocument56 pagesIntroduction to Derivatives Marketsne002No ratings yet

- Role of Financial Futures With Reference To Nse NiftyDocument58 pagesRole of Financial Futures With Reference To Nse NiftyWebsoft Tech-HydNo ratings yet

- Forwards & FuturesDocument43 pagesForwards & FuturesasifanisNo ratings yet

- Updated LECTURE 2 - Risk Quantification (Basic Concepts)Document47 pagesUpdated LECTURE 2 - Risk Quantification (Basic Concepts)Ajid Ur Rehman100% (1)

- DerivativesDocument111 pagesDerivativesMuhammad Moazzam JavaidNo ratings yet

- Topic 4 - Accounting For Derivative Instruments - A211Document94 pagesTopic 4 - Accounting For Derivative Instruments - A211Xiao Xuan100% (1)

- 05 Derivatives Market ARZ PDFDocument45 pages05 Derivatives Market ARZ PDFDaviNo ratings yet

- Derivatives Analysis and Valuation: Learning OutcomesDocument64 pagesDerivatives Analysis and Valuation: Learning OutcomesPravesh PangeniNo ratings yet

- Forward and Futures Contracts: Key DifferencesDocument15 pagesForward and Futures Contracts: Key DifferencesrdtdtdrtdtrNo ratings yet

- 08 - Nurturing Green (C)Document14 pages08 - Nurturing Green (C)miku hrshNo ratings yet

- 07 - VC Financing Co Creation and ExpansionDocument13 pages07 - VC Financing Co Creation and Expansionmiku hrshNo ratings yet

- Chap 007Document38 pagesChap 007Khuong KhuongNo ratings yet

- Investments, 8 Edition: Portfolio Performance EvaluationDocument44 pagesInvestments, 8 Edition: Portfolio Performance Evaluationmiku hrshNo ratings yet

- 07 - VC Financing Co Creation and ExpansionDocument13 pages07 - VC Financing Co Creation and Expansionmiku hrshNo ratings yet

- 07 - VC Financing Co Creation and ExpansionDocument13 pages07 - VC Financing Co Creation and Expansionmiku hrshNo ratings yet

- Private Equity and Venture Capital: Atul KediaDocument11 pagesPrivate Equity and Venture Capital: Atul Kediamiku hrshNo ratings yet

- 14 - VC NegotiationDocument10 pages14 - VC Negotiationmiku hrshNo ratings yet

- Private Equity and Venture Capital: Atul KediaDocument15 pagesPrivate Equity and Venture Capital: Atul Kediamiku hrshNo ratings yet

- Private Equity and Venture Capital: Atul KediaDocument12 pagesPrivate Equity and Venture Capital: Atul Kediamiku hrshNo ratings yet

- 07 - VC Financing Co Creation and ExpansionDocument13 pages07 - VC Financing Co Creation and Expansionmiku hrshNo ratings yet

- 12 - Investment ProcessDocument11 pages12 - Investment Processmiku hrshNo ratings yet

- Volatility Smiles and EstimationDocument10 pagesVolatility Smiles and Estimationmiku hrshNo ratings yet

- S2. The Mechanics of The Futures MarketDocument13 pagesS2. The Mechanics of The Futures Marketmiku hrshNo ratings yet

- The Greek Letters: Option Portfolio Value and GreeksDocument16 pagesThe Greek Letters: Option Portfolio Value and Greeksmiku hrshNo ratings yet

- Swaptions: European Swap OptionsDocument4 pagesSwaptions: European Swap Optionsmiku hrshNo ratings yet

- Futures Options and Optiosn On Stocjk Indices and CurrenciesDocument9 pagesFutures Options and Optiosn On Stocjk Indices and Currenciesmiku hrshNo ratings yet

- Heston Model: Sankarshan Basu Professor of Finance Indian Institute of Management BangaloreDocument3 pagesHeston Model: Sankarshan Basu Professor of Finance Indian Institute of Management Bangaloremiku hrshNo ratings yet

- Investments, 8 Edition: Index ModelsDocument21 pagesInvestments, 8 Edition: Index Modelsmiku hrshNo ratings yet

- Investments, 8 Edition: Risk Aversion and Capital Allocation To Risky AssetsDocument33 pagesInvestments, 8 Edition: Risk Aversion and Capital Allocation To Risky Assetsmiku hrshNo ratings yet

- What Are Exotic Options?Document9 pagesWhat Are Exotic Options?miku hrshNo ratings yet

- Credit DerivativesDocument10 pagesCredit Derivativesmiku hrshNo ratings yet

- Chap 007Document38 pagesChap 007Khuong KhuongNo ratings yet

- Security Analysis and Portfolio Management: Session-1Document26 pagesSecurity Analysis and Portfolio Management: Session-1miku hrshNo ratings yet

- Binomial Option Pricing ModelDocument12 pagesBinomial Option Pricing Modelmiku hrshNo ratings yet

- Credit Derivatives - AdditionalDocument13 pagesCredit Derivatives - Additionalmiku hrshNo ratings yet

- Investments, 8 Edition: Portfolio Performance EvaluationDocument44 pagesInvestments, 8 Edition: Portfolio Performance Evaluationmiku hrshNo ratings yet

- Black Scholes ModelDocument10 pagesBlack Scholes Modelmiku hrshNo ratings yet

- Volatility Smiles and EstimationDocument10 pagesVolatility Smiles and Estimationmiku hrshNo ratings yet

- FinMan Module 2 Financial Markets & InstitutionsDocument13 pagesFinMan Module 2 Financial Markets & Institutionserickson hernanNo ratings yet

- Amortization Definition - InvestopediaDocument7 pagesAmortization Definition - InvestopediaBob KaneNo ratings yet

- Tegar Dwi Laksono AKDocument4 pagesTegar Dwi Laksono AKTegarNo ratings yet

- Sanjay Case Study 2017 QsDocument3 pagesSanjay Case Study 2017 QsIBBF FitnessNo ratings yet

- Modern Portfolio Theory and Investment Analysis 9th Edition Elton Test Bank CH 5Document4 pagesModern Portfolio Theory and Investment Analysis 9th Edition Elton Test Bank CH 5HarshNo ratings yet

- Abhay RPR First DrapDocument20 pagesAbhay RPR First DrapAbhay SrivastavaNo ratings yet

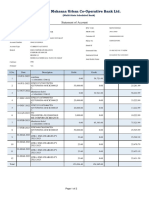

- Statement of AccountDocument2 pagesStatement of AccountReshma ModhiaNo ratings yet

- SECURED BUSINESS LOAN FUNDINGDocument11 pagesSECURED BUSINESS LOAN FUNDINGbhavneshsinghNo ratings yet

- NPCI Workshop Pre-Read MaterialDocument17 pagesNPCI Workshop Pre-Read MaterialRajesh ShuklaNo ratings yet

- Fundraising Methods and Trends in the Primary MarketDocument52 pagesFundraising Methods and Trends in the Primary Marketsejal100% (1)

- Macro LMS - Chapter 25&26Document14 pagesMacro LMS - Chapter 25&26Bảo Vy TrươngNo ratings yet

- Jcsgo Christian Academy: Senior High School DepartmentDocument4 pagesJcsgo Christian Academy: Senior High School DepartmentFredinel Malsi ArellanoNo ratings yet

- Cia ModelDocument4 pagesCia Modelyouzy rkNo ratings yet

- Savings statement overseas withdrawalsDocument2 pagesSavings statement overseas withdrawalsTimothy BlackNo ratings yet

- Indu Sind Pay FormDocument2 pagesIndu Sind Pay FormDesikanNo ratings yet

- Blockchain Unconfirmed Transaction Hack Script PDF FreeDocument2 pagesBlockchain Unconfirmed Transaction Hack Script PDF FreeHealing Relaxing Sleep Music100% (2)

- Credit ManagementDocument4 pagesCredit ManagementYuuna HoshinoNo ratings yet

- APAC Recruiting Deck v.FINALDocument30 pagesAPAC Recruiting Deck v.FINALPari SethNo ratings yet

- History Islami BankingDocument14 pagesHistory Islami BankingMilon SultanNo ratings yet

- Materi Kuliah MK StratejikDocument1 pageMateri Kuliah MK StratejikDiyo AhmadNo ratings yet

- US Financial Crisis of 2008-2009 ExplainedDocument11 pagesUS Financial Crisis of 2008-2009 ExplainedPhan Thị Thu ThảoNo ratings yet

- AkshatJain 0008 ACFDocument5 pagesAkshatJain 0008 ACFAkshat JainNo ratings yet

- ITP - Foreign Exchange RateDocument29 pagesITP - Foreign Exchange RateSuvamDharNo ratings yet

- International Finance A SR Jwhe3pDocument11 pagesInternational Finance A SR Jwhe3pRajni KumariNo ratings yet

- Treasury ManagementDocument9 pagesTreasury ManagementpareshgholapNo ratings yet

- Tugas KonsolidasiDocument10 pagesTugas KonsolidasiFajar Rahadi NugrohoNo ratings yet

- Long-Term Financial Planning: Fundamentals of Corporate FinanceDocument17 pagesLong-Term Financial Planning: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- FC TransactionDocument40 pagesFC TransactionShihab Hasan ChowdhuryNo ratings yet

- IFRS Financial Reporting and Asset ImpairmentDocument10 pagesIFRS Financial Reporting and Asset ImpairmentNitin ChoudharyNo ratings yet

- Shirkah and Its Variant SummaryDocument4 pagesShirkah and Its Variant SummaryOmayr QureshiNo ratings yet