You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5814)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- ICAEW Professional Level Tax Compliance Question & Answer Bank March 2016 To March 2020 PDFDocument414 pagesICAEW Professional Level Tax Compliance Question & Answer Bank March 2016 To March 2020 PDFOptimal Management Solution100% (1)

- Revised Corporation CodeDocument172 pagesRevised Corporation CodeRic John Naquila Cabilan70% (10)

- How To Adjusted BalanceDocument4 pagesHow To Adjusted BalanceAnya Daniella80% (5)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Godrej One, Pirojshanagar, Eastern Express Highway, Vikhroli (East), Mumbai - 400079Document2 pagesGodrej One, Pirojshanagar, Eastern Express Highway, Vikhroli (East), Mumbai - 400079Shashikant Thakre100% (1)

- AFAR Quizzer 2 SolutionsDocument8 pagesAFAR Quizzer 2 SolutionsRic John Naquila Cabilan100% (1)

- Solved Jurisdiction Z Levies An Excise Tax On Retail Purchases ofDocument1 pageSolved Jurisdiction Z Levies An Excise Tax On Retail Purchases ofAnbu jaromiaNo ratings yet

- PERDEV 2nd Quarter ReviewerDocument3 pagesPERDEV 2nd Quarter ReviewerRic John Naquila Cabilan50% (2)

- Advanced Financial Accounting & Reporting February 9, 2020Document8 pagesAdvanced Financial Accounting & Reporting February 9, 2020Ric John Naquila CabilanNo ratings yet

- Advanced Financial Accounting & Reporting February 9, 2020Document8 pagesAdvanced Financial Accounting & Reporting February 9, 2020Ric John Naquila CabilanNo ratings yet

- List of Stocks and Availability Purchases Orders: Rey Skintouch Beauty ProductsDocument10 pagesList of Stocks and Availability Purchases Orders: Rey Skintouch Beauty ProductsRic John Naquila CabilanNo ratings yet

- Mail Merge Application LetterDocument25 pagesMail Merge Application LetterRic John Naquila CabilanNo ratings yet

- Reading and Writing IntertextDocument3 pagesReading and Writing IntertextRic John Naquila Cabilan100% (1)

- NAME: - SECTION: - Brain DominanceDocument3 pagesNAME: - SECTION: - Brain DominanceRic John Naquila CabilanNo ratings yet

- Philippine Deposit Insurance CorporationDocument23 pagesPhilippine Deposit Insurance CorporationRic John Naquila CabilanNo ratings yet

- 3rd Quizzer TAX 2nd Sem SY 2019 2020Document4 pages3rd Quizzer TAX 2nd Sem SY 2019 2020Ric John Naquila CabilanNo ratings yet

- Law On CooperativesDocument106 pagesLaw On CooperativesRic John Naquila CabilanNo ratings yet

- S02 Joint and by Product ABC Backflush and Service Department Cost AllocationDocument5 pagesS02 Joint and by Product ABC Backflush and Service Department Cost AllocationRic John Naquila CabilanNo ratings yet

- AFAR Quizzer 1 SolutionsDocument12 pagesAFAR Quizzer 1 SolutionsRic John Naquila CabilanNo ratings yet

- JhgfdsaDocument2 pagesJhgfdsaRic John Naquila CabilanNo ratings yet

- C33 - PFRS 5 Discontinued OperationDocument2 pagesC33 - PFRS 5 Discontinued OperationAllaine ElfaNo ratings yet

- Taxation SlideDocument26 pagesTaxation SlidePei Jia WahNo ratings yet

- BIR Application For Registration FORM (1901)Document2 pagesBIR Application For Registration FORM (1901)Francis Nico PeñaNo ratings yet

- 114 (1) (Return of Income For A Person Deriving Income Only From Salary and Other Sources Eligible To File Salary Return) - 2020Document4 pages114 (1) (Return of Income For A Person Deriving Income Only From Salary and Other Sources Eligible To File Salary Return) - 2020asiashah1975No ratings yet

- Company Registration IrelandDocument9 pagesCompany Registration IrelandParas MittalNo ratings yet

- Computation of Total Income Income From Salary (Chapter IV A) 1696258Document3 pagesComputation of Total Income Income From Salary (Chapter IV A) 1696258amit22505No ratings yet

- Bill ToDocument1 pageBill ToAmin KhanNo ratings yet

- Combined Accounts - Computations - Company Tax ReturnDocument37 pagesCombined Accounts - Computations - Company Tax Returnvictoria.gutu91No ratings yet

- Bir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of March, 2017Document7 pagesBir Form 1601E - Schedule I Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of March, 2017khellany guerzonNo ratings yet

- DonationS UNDE INCOME TAX ACTDocument2 pagesDonationS UNDE INCOME TAX ACTManjeet KaurNo ratings yet

- Problem 4 2aDocument12 pagesProblem 4 2aHCM Nguyen Do Huy HoangNo ratings yet

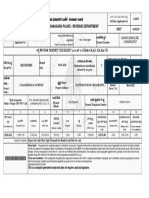

- Bruhat Bengaluru Mahanagara Palike - Revenue Department: Xjdœ LXD - /HZ Eud/ Eĺ Lbx¡E (6 E LDocument1 pageBruhat Bengaluru Mahanagara Palike - Revenue Department: Xjdœ LXD - /HZ Eud/ Eĺ Lbx¡E (6 E LManjunathNo ratings yet

- P 15-6 Apply Threshold Tests-Disclosure: RequiredDocument2 pagesP 15-6 Apply Threshold Tests-Disclosure: Requiredandrea de capellaNo ratings yet

- Sales Tax Return 16353854Document1 pageSales Tax Return 163538547799349No ratings yet

- Week 7Document3 pagesWeek 7yogeshgharpureNo ratings yet

- Group 6 Avanced Tax Assignment-1Document9 pagesGroup 6 Avanced Tax Assignment-1Jeremiah NcubeNo ratings yet

- TDS Late Fee (Or GST Late Fee) Is An Allowable ExpenditureDocument5 pagesTDS Late Fee (Or GST Late Fee) Is An Allowable ExpenditureDivyaNo ratings yet

- Airtel Bill For The Month of June'20Document2 pagesAirtel Bill For The Month of June'20Piyush MittalNo ratings yet

- Scan Split 8 FinalDocument39 pagesScan Split 8 FinalJefferson ClineNo ratings yet

- Declaration FormatsDocument4 pagesDeclaration FormatsG N Harish Kumar YadavNo ratings yet

- Rajesh Bora Itr PLBS 2022Document5 pagesRajesh Bora Itr PLBS 2022ABDUL KHALIKNo ratings yet

- Tax 2 SyllabusDocument9 pagesTax 2 SyllabusAlvin RufinoNo ratings yet

- Deductions From Gross Income Part 2 Illustrative ProblemsDocument2 pagesDeductions From Gross Income Part 2 Illustrative ProblemsJohn Rich GamasNo ratings yet

- HDFC Credit Card Limit Enhancement FormDocument1 pageHDFC Credit Card Limit Enhancement Formranju93No ratings yet

- Paper - 7: Direct Tax Laws: Items DebitedDocument26 pagesPaper - 7: Direct Tax Laws: Items DebitedANIL JARWALNo ratings yet

- Climate Action Incentive Payment Notice 2022 06 25 09 46 45 07823 PDFDocument3 pagesClimate Action Incentive Payment Notice 2022 06 25 09 46 45 07823 PDFalex mac dougallNo ratings yet