You might also like

- Harry Markowitz's Modern Portfolio Theory: The Efficient FrontierDocument7 pagesHarry Markowitz's Modern Portfolio Theory: The Efficient Frontiermahbobullah rahmaniNo ratings yet

- Chapter-2 Portfolio Analysis and SelectionDocument14 pagesChapter-2 Portfolio Analysis and Selection8008 Aman GuptaNo ratings yet

- Unit 4Document17 pagesUnit 4vivek badhanNo ratings yet

- Portofolio OptimalDocument6 pagesPortofolio Optimalmamih baekNo ratings yet

- Capital Asset Pricing Model: Make smart investment decisions to build a strong portfolioFrom EverandCapital Asset Pricing Model: Make smart investment decisions to build a strong portfolioRating: 4.5 out of 5 stars4.5/5 (3)

- Portfolio TheoryDocument3 pagesPortfolio TheoryZain MughalNo ratings yet

- Introduction to Index Funds and ETF's - Passive Investing for BeginnersFrom EverandIntroduction to Index Funds and ETF's - Passive Investing for BeginnersRating: 4.5 out of 5 stars4.5/5 (7)

- Retail Banking Assignment Yashkumar Patel 17020942046: Ans. Modern Portfolio TheoryDocument5 pagesRetail Banking Assignment Yashkumar Patel 17020942046: Ans. Modern Portfolio TheoryYashkumar PatelNo ratings yet

- Definition of Portfolio AnalysisDocument15 pagesDefinition of Portfolio Analysissimrenchoudhary057No ratings yet

- Unit4 SAPMDocument11 pagesUnit4 SAPMBhaskaran BalamuraliNo ratings yet

- Security Analysis and Portfolio ManagementDocument6 pagesSecurity Analysis and Portfolio ManagementPrabakaran SanthanamNo ratings yet

- Portfolio Evaluation and RevisionDocument53 pagesPortfolio Evaluation and Revisionjibumon k gNo ratings yet

- Investment ManagementDocument12 pagesInvestment ManagementBe YourselfNo ratings yet

- Portfolio Management - Meaning and Important ConceptsDocument6 pagesPortfolio Management - Meaning and Important ConceptsManjulaNo ratings yet

- Portfolio Management - Meaning and Important ConceptsDocument6 pagesPortfolio Management - Meaning and Important ConceptsManjula50% (2)

- Finman3 Report DiscussionDocument5 pagesFinman3 Report DiscussionFlorence CuansoNo ratings yet

- Powerpoint Concept Smjhne Security-Analysis-and-Portfolo-Management-Unit-4-Dr-Asma-KhanDocument66 pagesPowerpoint Concept Smjhne Security-Analysis-and-Portfolo-Management-Unit-4-Dr-Asma-KhanShailjaNo ratings yet

- Modern Portfolio TheoryDocument6 pagesModern Portfolio TheoryRahul PillaiNo ratings yet

- Topic: Markowitz Theory (With Assumptions) IntroductionDocument3 pagesTopic: Markowitz Theory (With Assumptions) Introductiondeepti sharmaNo ratings yet

- Understanding The Efficient FrontierDocument4 pagesUnderstanding The Efficient FrontierThanh Tu NguyenNo ratings yet

- Portfolio Construction and EvaluationDocument5 pagesPortfolio Construction and Evaluations_s_swapnaNo ratings yet

- Port Folio ManagementDocument90 pagesPort Folio Managementnaga0017100% (1)

- Markowitz ModelDocument25 pagesMarkowitz ModelVignesh PrabhuNo ratings yet

- Investement Analysis and Portfolio Management Chapter 6Document12 pagesInvestement Analysis and Portfolio Management Chapter 6Oumer ShaffiNo ratings yet

- Portfolio Management - Module 2Document16 pagesPortfolio Management - Module 2satyamchoudhary2004No ratings yet

- Rangkuman Bab 8 Portfolio Selection and Asset AllocationDocument3 pagesRangkuman Bab 8 Portfolio Selection and Asset Allocationindah oliviaNo ratings yet

- Portfolio Theory - Ses2Document82 pagesPortfolio Theory - Ses2Vaidyanathan Ravichandran100% (1)

- Investment Portfolio Management. Objectives and ConstraintsDocument5 pagesInvestment Portfolio Management. Objectives and ConstraintsShirinSuterNo ratings yet

- Modern Portfolio Theory: Session IV & VDocument30 pagesModern Portfolio Theory: Session IV & VAmit Singh RanaNo ratings yet

- Porfolio ManagementDocument89 pagesPorfolio ManagementTeddy DavisNo ratings yet

- ChapterDocument90 pagesChapterRavi SharmaNo ratings yet

- What Is Modern Portfolio Theory (MPT) ?Document6 pagesWhat Is Modern Portfolio Theory (MPT) ?nidamahNo ratings yet

- FM - Modern Portfolio Theory 1Document7 pagesFM - Modern Portfolio Theory 1Lipika haldarNo ratings yet

- Objective of Study Concepts Investment Options Data Collection Analysis Recommendation Limitations ReferencesDocument26 pagesObjective of Study Concepts Investment Options Data Collection Analysis Recommendation Limitations Referenceshtikyani_1No ratings yet

- What Is A Portfolio?: Key TakeawaysDocument7 pagesWhat Is A Portfolio?: Key TakeawaysSabarni ChatterjeeNo ratings yet

- Investment Management FAQDocument3 pagesInvestment Management FAQRockyBalboaaNo ratings yet

- Portfolio Management - Module 1Document15 pagesPortfolio Management - Module 1satyamchoudhary2004No ratings yet

- Modern Portfolio TheoryDocument12 pagesModern Portfolio TheoryruiyizNo ratings yet

- Market Portfolio Efficient FrontierDocument33 pagesMarket Portfolio Efficient FrontierVaidyanathan RavichandranNo ratings yet

- BBA Unit 5Document4 pagesBBA Unit 5gorang GehaniNo ratings yet

- Unit 5 SAPMDocument26 pagesUnit 5 SAPMMathangi VNo ratings yet

- A Study in Portfolio Management: 2.1 Indierence Curves and Risk AversionDocument15 pagesA Study in Portfolio Management: 2.1 Indierence Curves and Risk AversionAseem MiglaniNo ratings yet

- Unit-2 Portfolio Analysis &selectionDocument64 pagesUnit-2 Portfolio Analysis &selectiontanishq8807No ratings yet

- Corporate Portfolio Analysis TechniquesDocument24 pagesCorporate Portfolio Analysis TechniquesSanjay DhageNo ratings yet

- Modern Portfolio TheoryDocument17 pagesModern Portfolio Theorymahbobullah rahmaniNo ratings yet

- Portfolio TheoryDocument6 pagesPortfolio TheorykrgitNo ratings yet

- Risk & Return Analysis - Prime BookDocument25 pagesRisk & Return Analysis - Prime Bookßïshñü PhüyãlNo ratings yet

- Basics of FinanceDocument46 pagesBasics of FinanceELgün F. QurbanovNo ratings yet

- Risk:: The Two Major Types of Risks AreDocument16 pagesRisk:: The Two Major Types of Risks AreAbhishek TyagiNo ratings yet

- 1.1 Introduction To The StudyDocument68 pages1.1 Introduction To The Studyrajesh bathulaNo ratings yet

- Basics of FinanceDocument46 pagesBasics of Financeisrael_zamora6389No ratings yet

- Modern Portfolio Theory, Capital Market Theory, and Asset Pricing ModelsDocument33 pagesModern Portfolio Theory, Capital Market Theory, and Asset Pricing ModelsvamshidharNo ratings yet

- Modern Portfolio Theory: Jump To: Navigation, SearchDocument14 pagesModern Portfolio Theory: Jump To: Navigation, SearchKunal PanjaNo ratings yet

- Modern Portfolio Theory, Capital Market Theory, and Asset Pricing ModelsDocument33 pagesModern Portfolio Theory, Capital Market Theory, and Asset Pricing ModelsV. G. LagnerNo ratings yet

- Chapter 3 Portfolio Selection PDFDocument6 pagesChapter 3 Portfolio Selection PDFMariya BhavesNo ratings yet

- Portfolio Advice For A Multifactor WorldDocument20 pagesPortfolio Advice For A Multifactor Worldasilvestre19807No ratings yet

- The 6 Market Model Britannia: 18020448091 Rajrishi Daharwal 18020448125 Dulal Nandy 18020448062 Ravi PandhareDocument12 pagesThe 6 Market Model Britannia: 18020448091 Rajrishi Daharwal 18020448125 Dulal Nandy 18020448062 Ravi PandhareRajarshi DaharwalNo ratings yet

- Stock Analysis 2Document62 pagesStock Analysis 2Rajarshi DaharwalNo ratings yet

- FcpaDocument4 pagesFcpaRajarshi DaharwalNo ratings yet

- FM Assignment-2Document8 pagesFM Assignment-2Rajarshi DaharwalNo ratings yet

- SAPMDocument4 pagesSAPMRajarshi DaharwalNo ratings yet

- FM Questions RevisedDocument15 pagesFM Questions RevisedRajarshi DaharwalNo ratings yet

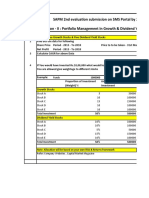

- If You Would Have Invested Rs.10,00,000 What Would Have Been Weightage To Both The Categories?Document4 pagesIf You Would Have Invested Rs.10,00,000 What Would Have Been Weightage To Both The Categories?Rajarshi DaharwalNo ratings yet

- 2 Way AnnovaDocument1 page2 Way AnnovaRajarshi DaharwalNo ratings yet

- Q1 Liabilities Amount Assests Amount Balance Sheet: CA 225000 CL CA-135000 90000Document2 pagesQ1 Liabilities Amount Assests Amount Balance Sheet: CA 225000 CL CA-135000 90000Rajarshi DaharwalNo ratings yet

- Statistics Assignment 3 Q1Document1 pageStatistics Assignment 3 Q1Rajarshi DaharwalNo ratings yet

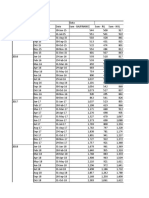

- Efficient Frontier: Month HDFC TCS % Return TCS % Return HDFC HDFC TCS RP S.D Portfolio Mix (W)Document1 pageEfficient Frontier: Month HDFC TCS % Return TCS % Return HDFC HDFC TCS RP S.D Portfolio Mix (W)Rajarshi DaharwalNo ratings yet

- AB Limited Provides You The Following DataDocument2 pagesAB Limited Provides You The Following DataRajarshi DaharwalNo ratings yet

- CTC Structure: 7% Component A Component B Component C Component D Component E Component FDocument1 pageCTC Structure: 7% Component A Component B Component C Component D Component E Component FRajarshi DaharwalNo ratings yet

- How To Trade A News BreakoutDocument4 pagesHow To Trade A News BreakoutJason2Kool100% (2)

- INfyDocument14 pagesINfyswaroop shettyNo ratings yet

- Can I Trust My Financial AdvisorDocument5 pagesCan I Trust My Financial Advisoryous douseNo ratings yet

- Business Value From ITDocument29 pagesBusiness Value From ITabhik0001No ratings yet

- Assignment 5 (Price Discrimination)Document2 pagesAssignment 5 (Price Discrimination)Baideshik JobNo ratings yet

- P1 Syllabus IcmabDocument19 pagesP1 Syllabus Icmabzia4000100% (1)

- An Empirical Analysis of Economic Policies, Institutions, and Investment Nexus in PakistanDocument20 pagesAn Empirical Analysis of Economic Policies, Institutions, and Investment Nexus in PakistanNaveed SandhuNo ratings yet

- Stocks VNODocument9 pagesStocks VNOBis LactaNo ratings yet

- Risk and Retrun TheoryDocument40 pagesRisk and Retrun TheorySonakshi TayalNo ratings yet

- Instruments of Credit Control in Central BankDocument8 pagesInstruments of Credit Control in Central BankAnya SinghNo ratings yet

- Hill Country Snack Foods Case AnalysisDocument5 pagesHill Country Snack Foods Case Analysisdivakar62No ratings yet

- Lesson 3Document17 pagesLesson 3Angelica MagdaraogNo ratings yet

- Development Trends of The InternatiDocument10 pagesDevelopment Trends of The InternatiJakeNo ratings yet

- Activation of Additional SegmentsDocument1 pageActivation of Additional SegmentsArun KumarNo ratings yet

- Actual Test 3 Test BankDocument50 pagesActual Test 3 Test BankWihl Mathew ZalatarNo ratings yet

- Komparasi Capital Asset Pricing Model Versus Arbitrage Pricing Theory Model Atas Volatilitas Return SahamDocument19 pagesKomparasi Capital Asset Pricing Model Versus Arbitrage Pricing Theory Model Atas Volatilitas Return SahamIDFL IDFLNo ratings yet

- Pre Imbalance BibleDocument67 pagesPre Imbalance BibleVarun 99100% (1)

- Practice Question - 2 Portfolio ManagementDocument5 pagesPractice Question - 2 Portfolio Managementzoyaatique72No ratings yet

- Portfolio Revision TechniquesDocument28 pagesPortfolio Revision Techniquesspssimran60% (5)

- Solution Manual For Corporate Finance 12th Edition Stephen Ross Randolph Westerfield Jeffrey Jaffe Bradford JordanDocument31 pagesSolution Manual For Corporate Finance 12th Edition Stephen Ross Randolph Westerfield Jeffrey Jaffe Bradford JordanOliviaHarrisonobijq99% (86)

- Shareholders-Agreement TemplateDocument45 pagesShareholders-Agreement Templateklarita ferji100% (1)

- Forex Virtuoso PDFDocument19 pagesForex Virtuoso PDFHARISH_IJTNo ratings yet

- Chapter 2Document13 pagesChapter 2eswariNo ratings yet

- Problem SolutionsDocument4 pagesProblem SolutionsParas JangirNo ratings yet

- Cap Budegt ProbsDocument4 pagesCap Budegt ProbsAR Ananth Rohith BhatNo ratings yet

- Ch02 TB Loftus 3e - Textbook Solution Ch02 TB Loftus 3e - Textbook SolutionDocument12 pagesCh02 TB Loftus 3e - Textbook Solution Ch02 TB Loftus 3e - Textbook SolutionTrinh LêNo ratings yet

- DMS-IIT Delhi Compendium 2019-21Document55 pagesDMS-IIT Delhi Compendium 2019-21Sounak Chatterjee100% (1)

- Finance Report of Sharekhan LTDDocument85 pagesFinance Report of Sharekhan LTDjsmith84No ratings yet

- Nasdaq Dubai Ipo GuideDocument104 pagesNasdaq Dubai Ipo GuidetamersalahNo ratings yet

- Sahodaya Pre-Board Examination Term II Subject - Entrepreneurship - 066 Answer Key - Set ADocument11 pagesSahodaya Pre-Board Examination Term II Subject - Entrepreneurship - 066 Answer Key - Set AAravind SNo ratings yet

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 3.5 out of 5 stars3.5/5 (8)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successFrom EverandReady, Set, Growth hack:: A beginners guide to growth hacking successRating: 4.5 out of 5 stars4.5/5 (93)

- An easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyFrom EverandAn easy approach to trading with bollinger bands: How to learn how to use Bollinger bands to trade online successfullyRating: 3 out of 5 stars3/5 (1)

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamFrom EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamNo ratings yet

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthFrom EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthRating: 4 out of 5 stars4/5 (20)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialNo ratings yet

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Built, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursFrom EverandBuilt, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursRating: 5 out of 5 stars5/5 (13)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialFrom EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialRating: 4.5 out of 5 stars4.5/5 (32)

- Creating Shareholder Value: A Guide For Managers And InvestorsFrom EverandCreating Shareholder Value: A Guide For Managers And InvestorsRating: 4.5 out of 5 stars4.5/5 (8)

- The Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsFrom EverandThe Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsNo ratings yet

- Product-Led Growth: How to Build a Product That Sells ItselfFrom EverandProduct-Led Growth: How to Build a Product That Sells ItselfRating: 5 out of 5 stars5/5 (1)

- Mastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsFrom EverandMastering the VC Game: A Venture Capital Insider Reveals How to Get from Start-up to IPO on Your TermsRating: 4.5 out of 5 stars4.5/5 (21)

- Value: The Four Cornerstones of Corporate FinanceFrom EverandValue: The Four Cornerstones of Corporate FinanceRating: 4.5 out of 5 stars4.5/5 (18)

- Valley Girls: Lessons From Female Founders in the Silicon Valley and BeyondFrom EverandValley Girls: Lessons From Female Founders in the Silicon Valley and BeyondNo ratings yet

- Mind over Money: The Psychology of Money and How to Use It BetterFrom EverandMind over Money: The Psychology of Money and How to Use It BetterRating: 4 out of 5 stars4/5 (24)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (8)

- Finance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)From EverandFinance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)Rating: 4 out of 5 stars4/5 (5)

- Buffett's 2-Step Stock Market Strategy: Know When To Buy A Stock, Become A Millionaire, Get The Highest ReturnsFrom EverandBuffett's 2-Step Stock Market Strategy: Know When To Buy A Stock, Become A Millionaire, Get The Highest ReturnsRating: 5 out of 5 stars5/5 (1)

- The Value of a Whale: On the Illusions of Green CapitalismFrom EverandThe Value of a Whale: On the Illusions of Green CapitalismRating: 5 out of 5 stars5/5 (2)