You might also like

- CD 2U ManualDocument140 pagesCD 2U ManualottieNo ratings yet

- Akai MPC-Software ManualDocument219 pagesAkai MPC-Software ManualottieNo ratings yet

- Korg M50 - TRDocument136 pagesKorg M50 - TRRuben Puma TapiaNo ratings yet

- User Guide: Safety and Operation Precautions Must Be Read Before Using This UnitDocument53 pagesUser Guide: Safety and Operation Precautions Must Be Read Before Using This UnitKalygulyNo ratings yet

- Operation Manual: Operation Manual Can Be Downloaded From The ZOOM Official Website. (WWW - Zoom.jp/docs/r16)Document100 pagesOperation Manual: Operation Manual Can Be Downloaded From The ZOOM Official Website. (WWW - Zoom.jp/docs/r16)Jussi JänttiNo ratings yet

- Ableton Live Tutorial: 25 Pro-Tips: MusictechDocument9 pagesAbleton Live Tutorial: 25 Pro-Tips: MusictechottieNo ratings yet

- Ias 16 Property Plant and Equipment Summary PDFDocument8 pagesIas 16 Property Plant and Equipment Summary PDFPuneeth DhondaleNo ratings yet

- JUNO-DS 88 76 61 Eng01 WDocument22 pagesJUNO-DS 88 76 61 Eng01 WottieNo ratings yet

- BR-1180 Om PDFDocument192 pagesBR-1180 Om PDFAndre Tomazini0% (1)

- Yamaha PSR-1500 PSR 3000 Operating ManualDocument220 pagesYamaha PSR-1500 PSR 3000 Operating ManualJonathan Harrington100% (2)

- Pa800 201UM ENGDocument344 pagesPa800 201UM ENGTakis MatthaiouNo ratings yet

- Guideline: Subject: IFRS 9 Financial Instruments and Disclosures Category: AccountingDocument64 pagesGuideline: Subject: IFRS 9 Financial Instruments and Disclosures Category: AccountingottieNo ratings yet

- First Grade Dolch Sight Word Flash CardsDocument6 pagesFirst Grade Dolch Sight Word Flash CardsottieNo ratings yet

- Ias 8 Accounting Policies Changes in Accounting Estimates and Errors SummaryDocument5 pagesIas 8 Accounting Policies Changes in Accounting Estimates and Errors SummaryWilmar AbriolNo ratings yet

- In Depth: A Look at Current Financial Reporting IssuesDocument15 pagesIn Depth: A Look at Current Financial Reporting IssuesottieNo ratings yet

- IFRS 15 Summary PDFDocument8 pagesIFRS 15 Summary PDFAshraf ValappilNo ratings yet

- Snapshot - IFRS 9 - Financial Instruments - Hedge AccountingDocument1 pageSnapshot - IFRS 9 - Financial Instruments - Hedge AccountingottieNo ratings yet

- Complete List of MS Excel Shortcut Key: Mohammed Ameerudheen M. A +919995614399Document3 pagesComplete List of MS Excel Shortcut Key: Mohammed Ameerudheen M. A +919995614399ottieNo ratings yet

- Fina Analysis m3Document22 pagesFina Analysis m3ottieNo ratings yet

- Pub Deposit Insurance Reform Cost Bank SupDocument16 pagesPub Deposit Insurance Reform Cost Bank SupottieNo ratings yet

- Strategy: Demystifying Asset-Backed Commercial PaperDocument12 pagesStrategy: Demystifying Asset-Backed Commercial PaperottieNo ratings yet

- Covered BondDocument3 pagesCovered BondottieNo ratings yet

- A Step by Step Guide To Learning SASDocument49 pagesA Step by Step Guide To Learning SASDRx Sonali TareiNo ratings yet

- Ifrs 15 Revenue From Contracts With Customers SnapshotDocument1 pageIfrs 15 Revenue From Contracts With Customers SnapshotottieNo ratings yet

- The Abcs of Abs: Accounting For Asset-Backed SecuritiesDocument11 pagesThe Abcs of Abs: Accounting For Asset-Backed SecuritiesottieNo ratings yet

- Icaap DtiDocument12 pagesIcaap DtiottieNo ratings yet

- GuidelineDocument17 pagesGuidelineottieNo ratings yet

- F9 JUNE 17 Mock QuestionsDocument23 pagesF9 JUNE 17 Mock QuestionsottieNo ratings yet

- F9 T Revision Study Planner June 2017Document1 pageF9 T Revision Study Planner June 2017ottieNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Project On AtmDocument51 pagesProject On Atmashwin_nakman77% (53)

- Gonder IndictmentDocument9 pagesGonder IndictmentChris GothnerNo ratings yet

- Plastic MoneyDocument48 pagesPlastic Moneyvanishachhabra5008No ratings yet

- Amna INTERNSHIP REPORTDocument35 pagesAmna INTERNSHIP REPORTMadiha ToOrNo ratings yet

- Philippine Banking SystemDocument2 pagesPhilippine Banking SystemXytusNo ratings yet

- Chapter 7.5 AccountDocument1 pageChapter 7.5 Accountmarianne raelNo ratings yet

- Caraga Regional Science High School: Subject: FABMDocument3 pagesCaraga Regional Science High School: Subject: FABMJezelle Grace EaNo ratings yet

- Htpadu bs2022Document2 pagesHtpadu bs2022shuhada shuhaimiNo ratings yet

- Axix Bank ProjectDocument67 pagesAxix Bank ProjectSâñjây BîñdNo ratings yet

- Metro Bank PLC ArticleDocument2 pagesMetro Bank PLC ArticleDave LiNo ratings yet

- Penyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)Document2 pagesPenyata Akaun: Tarikh Date Keterangan Description Terminal ID ID Terminal Amaun (RM) Amount (RM) Baki (RM) Balance (RM)Vitus JTinusNo ratings yet

- Compound InterestDocument29 pagesCompound InterestNicole Roxanne RubioNo ratings yet

- Reporter No. 4 - Pdic LawDocument47 pagesReporter No. 4 - Pdic LawJi YuNo ratings yet

- Herstatt Risk and Collapse of Herstatt BankDocument21 pagesHerstatt Risk and Collapse of Herstatt BankChirdeep PareekNo ratings yet

- Banking System: Rashid SirDocument3 pagesBanking System: Rashid Sirparassh knowledgeNo ratings yet

- NEw IC 38 Question Bank 366Document58 pagesNEw IC 38 Question Bank 366Kit Cat83% (6)

- Case 28 AutozoneDocument39 pagesCase 28 AutozonePatcharanan SattayapongNo ratings yet

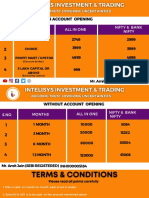

- Intelisys Pricing PlanDocument5 pagesIntelisys Pricing PlanregsNo ratings yet

- Accounting and Auditing MCQs Part-1 by Alisha Mahajan PDFDocument58 pagesAccounting and Auditing MCQs Part-1 by Alisha Mahajan PDFJamodvipulNo ratings yet

- The Impact of Key Audit Matters Disclosure On Communicative ValueDocument19 pagesThe Impact of Key Audit Matters Disclosure On Communicative ValueDzulfaqor Tanzil ArifinNo ratings yet

- Int. Acc 1 Chap 2Document7 pagesInt. Acc 1 Chap 2Nicole Anne Santiago SibuloNo ratings yet

- Emerging Areas For Articleship ExperienceDocument17 pagesEmerging Areas For Articleship ExperienceAmit JainNo ratings yet

- Burger KingDocument6 pagesBurger KingAditya SapraNo ratings yet

- Banking System in IndiaDocument62 pagesBanking System in IndiaRashi JoshiNo ratings yet

- Financial Statement Analysis: K R Subramanyam John J WildDocument34 pagesFinancial Statement Analysis: K R Subramanyam John J WildAgus Tina100% (1)

- Tanggal Uraian Transaksi Nominal Transaksi SaldoDocument4 pagesTanggal Uraian Transaksi Nominal Transaksi SaldoPipit NurfitrohNo ratings yet

- FN107-1342 - Footnotes Levin-Coburn Report.Document1,037 pagesFN107-1342 - Footnotes Levin-Coburn Report.Rick ThomaNo ratings yet

- Chapter 02 Final AccountsDocument69 pagesChapter 02 Final AccountsAuthor Jyoti Prakash rathNo ratings yet

- 30 Transactions With Their Journal EntriesDocument9 pages30 Transactions With Their Journal EntriesPrashant BhardwajNo ratings yet

- Test Ii: Misplaced Check (AR)Document10 pagesTest Ii: Misplaced Check (AR)Hannaniah PabicoNo ratings yet