You might also like

- Republic of The Philippines Supreme Court Manila Rule On Adoption A. Domestic AdoptionDocument10 pagesRepublic of The Philippines Supreme Court Manila Rule On Adoption A. Domestic AdoptionSteph SantiagoNo ratings yet

- National Flood Insurance Act of 1968 and The Flood Disaster Protection Act of 1973Document101 pagesNational Flood Insurance Act of 1968 and The Flood Disaster Protection Act of 1973Steph SantiagoNo ratings yet

- Public Law 109-417 109th Congress An ActDocument51 pagesPublic Law 109-417 109th Congress An ActSteph SantiagoNo ratings yet

- Petitioners Vs Vs Respondents: Second DivisionDocument12 pagesPetitioners Vs Vs Respondents: Second DivisionSteph SantiagoNo ratings yet

- 169217-2014-Grande v. Antonio PDFDocument9 pages169217-2014-Grande v. Antonio PDFSteph SantiagoNo ratings yet

- Petitioner Vs Vs Respondents: First DivisionDocument7 pagesPetitioner Vs Vs Respondents: First DivisionSteph SantiagoNo ratings yet

- RA 9262 Battered Wife SyndromeDocument10 pagesRA 9262 Battered Wife SyndromeSteph SantiagoNo ratings yet

- 2010 Navarro - v. - Ermita20180920 5466 Ta5meu PDFDocument17 pages2010 Navarro - v. - Ermita20180920 5466 Ta5meu PDFSteph SantiagoNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument7 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledSteph SantiagoNo ratings yet

- Ra 9255Document7 pagesRa 9255Steph SantiagoNo ratings yet

- 2017 Ara - v. - Pizarro20170711 911 48cu5o PDFDocument17 pages2017 Ara - v. - Pizarro20170711 911 48cu5o PDFSteph SantiagoNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Cambridge International AS & A Level: Economics 9708/32Document12 pagesCambridge International AS & A Level: Economics 9708/32PRIYANK RAWATNo ratings yet

- A Rothschild Plan For World GovernmentDocument31 pagesA Rothschild Plan For World GovernmentZsi GaNo ratings yet

- List of Importables ExcelDocument4 pagesList of Importables ExcelRACNo ratings yet

- Acc 423 Advanced TaxationDocument50 pagesAcc 423 Advanced Taxationkajojo joyNo ratings yet

- Centre State RelationsDocument9 pagesCentre State RelationsBuNo ratings yet

- Pramerica Life Rakshak SmartDocument10 pagesPramerica Life Rakshak SmartTraditional SamayalNo ratings yet

- Agarwal Shubh@gmailDocument2 pagesAgarwal Shubh@gmailapi-380051267% (3)

- Torcuator Vs Bernabe - G.R. No. 134219 - 20210705 - 223257Document9 pagesTorcuator Vs Bernabe - G.R. No. 134219 - 20210705 - 223257Maria Fiona Duran MerquitaNo ratings yet

- Guide+to+Importing+and+Exporting +Breaking+Down+the+BarriersDocument77 pagesGuide+to+Importing+and+Exporting +Breaking+Down+the+BarriersGrand-Master-FlashNo ratings yet

- XXII. CIR vs. Procter & GambleDocument12 pagesXXII. CIR vs. Procter & GambleStef OcsalevNo ratings yet

- Application For Registration: Taxpayer Identification Number (TIN)Document4 pagesApplication For Registration: Taxpayer Identification Number (TIN)Bernadette LeaNo ratings yet

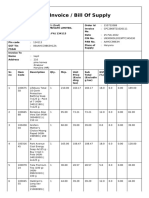

- Tax Invoice / Bill of SupplyDocument2 pagesTax Invoice / Bill of SupplyKapil SinglaNo ratings yet

- 2281 Economics: MARK SCHEME For The October/November 2006 Question PaperDocument3 pages2281 Economics: MARK SCHEME For The October/November 2006 Question Papermstudy123456100% (1)

- Microeconomics Principles and Policy 13th Edition Baumol Solutions ManualDocument5 pagesMicroeconomics Principles and Policy 13th Edition Baumol Solutions Manualphedrajoshuan28yjy100% (25)

- Data Analytics For Accounting, 2nd Edition Vernon Richardson PDFDocument1,026 pagesData Analytics For Accounting, 2nd Edition Vernon Richardson PDFjie100% (1)

- Brake Valve, Relay Valve 27.12.19 PDFDocument1 pageBrake Valve, Relay Valve 27.12.19 PDFnithinNo ratings yet

- Consolidated 2018 Forms 1099 and Details: Robinhood (650) 940-2700Document8 pagesConsolidated 2018 Forms 1099 and Details: Robinhood (650) 940-2700Renjie XuNo ratings yet

- The Fall of Ravi RestaurantDocument11 pagesThe Fall of Ravi RestaurantialimughalNo ratings yet

- Doctrine:: Commissioner of Internal Revenue vs. The Estate of Benigno TodaDocument2 pagesDoctrine:: Commissioner of Internal Revenue vs. The Estate of Benigno TodaElla CanuelNo ratings yet

- Individual Finance PDFDocument575 pagesIndividual Finance PDFshivam vajpai100% (1)

- Invoice IFBDocument1 pageInvoice IFBarindam kumarNo ratings yet

- 2014 Yara Fertilizer Industry HandbookDocument46 pages2014 Yara Fertilizer Industry HandbookMarcusWerteck100% (1)

- Ready ReckonerDocument72 pagesReady ReckonerSRINIVAS SEESALANo ratings yet

- Digests 2Document17 pagesDigests 2Henry LNo ratings yet

- Set 2 Social Science MajorsDocument4 pagesSet 2 Social Science MajorsPeter ReidNo ratings yet

- Final ProjectDocument5 pagesFinal ProjectAkshayNo ratings yet

- E-Commerce Taxation: Issues in Search of AnswersDocument23 pagesE-Commerce Taxation: Issues in Search of AnswersShiko TharwatNo ratings yet

- Merak Fiscal Model Library: Chad R/T (1999)Document2 pagesMerak Fiscal Model Library: Chad R/T (1999)Libya TripoliNo ratings yet

- LiabilitiesDocument2 pagesLiabilitiesFrederick AbellaNo ratings yet

- Full Employment BudgetDocument5 pagesFull Employment BudgetDhanikaNo ratings yet