You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Amended Articles of Incorporation ofDocument17 pagesAmended Articles of Incorporation ofxenoyewNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Accounting Procedures and ConceptsDocument36 pagesAccounting Procedures and ConceptsIlwynFreiresGascal0% (1)

- Self Journal V5 Instructions FLATDocument19 pagesSelf Journal V5 Instructions FLATBun100% (8)

- Strange Times, Or, Perhaps I Just Don T Get It (04.10.08)Document8 pagesStrange Times, Or, Perhaps I Just Don T Get It (04.10.08)BunNo ratings yet

- 7) Fusion Accounting Hub For Insurance Premium - External SourceDocument18 pages7) Fusion Accounting Hub For Insurance Premium - External Sourcekeerthi_fcmaNo ratings yet

- Accounting Entries in OracleDocument31 pagesAccounting Entries in OracleConrad RodricksNo ratings yet

- BCG Real-Case MotorDocument17 pagesBCG Real-Case MotorBunNo ratings yet

- Report of Collections and DepositsDocument3 pagesReport of Collections and DepositsReign Hernandez100% (1)

- Technical Indicator ExplanationDocument4 pagesTechnical Indicator ExplanationfranraizerNo ratings yet

- The Dash To Trash and The Grab For Growth (01.15.08)Document16 pagesThe Dash To Trash and The Grab For Growth (01.15.08)BunNo ratings yet

- Financial InstitutionsDocument2 pagesFinancial InstitutionsWilsonNo ratings yet

- Statement 20240101 20240116Document3 pagesStatement 20240101 20240116sophaneatungNo ratings yet

- Bake N Flake Company Final 4Document31 pagesBake N Flake Company Final 4sarojNo ratings yet

- Prospectus Syll-2016 Revised 20-11-2019Document68 pagesProspectus Syll-2016 Revised 20-11-2019Vaishnavi swamiNo ratings yet

- Sybbi FM Working Capital SumsDocument2 pagesSybbi FM Working Capital Sumssameer_kiniNo ratings yet

- Deposist AccountDocument6 pagesDeposist AccountwaheedarifNo ratings yet

- FHA HUD Preforeclosure Short Sale 2013 GuidelinesDocument48 pagesFHA HUD Preforeclosure Short Sale 2013 GuidelinesWendy RulnickNo ratings yet

- Mt103 - Pko Bank Polski Sa (Pko) Formatting Requirements: Status M/O/ C Field Field Name Content CommentsDocument3 pagesMt103 - Pko Bank Polski Sa (Pko) Formatting Requirements: Status M/O/ C Field Field Name Content CommentsSiau HuiNo ratings yet

- Chapter 2 (Section 2) Study Guide IDocument3 pagesChapter 2 (Section 2) Study Guide ILeinard AgcaoiliNo ratings yet

- PDFDocument1 pagePDFmd_muNo ratings yet

- Property Tax: OwnerDocument2 pagesProperty Tax: OwnerAnkit A DesaiNo ratings yet

- ESENECO 2 Interest Money Time Relationship Rev1Document49 pagesESENECO 2 Interest Money Time Relationship Rev1Irah BonifacioNo ratings yet

- 12006.departmental AccountsDocument10 pages12006.departmental Accountsyuvraj216No ratings yet

- E-Banking: Presented by:-PARDEEP KUMAR MBA (Hons.) 2.1 ROLL NO. - 3045Document20 pagesE-Banking: Presented by:-PARDEEP KUMAR MBA (Hons.) 2.1 ROLL NO. - 3045pardeepkayatNo ratings yet

- FINA01052383 - Tutorial 3 Problem SetDocument5 pagesFINA01052383 - Tutorial 3 Problem SetJunaid Arshad50% (2)

- Case Study Key Highlights:: Balance Sheet Sources of FundsDocument2 pagesCase Study Key Highlights:: Balance Sheet Sources of FundsVenkat ThiagarajanNo ratings yet

- NPP 2020 Final Web PDFDocument216 pagesNPP 2020 Final Web PDFMawuli AhorlumegahNo ratings yet

- Rasna Kashyap Startup Business PlanDocument29 pagesRasna Kashyap Startup Business PlanMayank jain100% (1)

- Instructions For Form 3520-A: Annual Information Return of Foreign Trust With A U.S. OwnerDocument4 pagesInstructions For Form 3520-A: Annual Information Return of Foreign Trust With A U.S. OwnerIRSNo ratings yet

- The Big Mac TheoryDocument4 pagesThe Big Mac TheoryGemini_0804No ratings yet

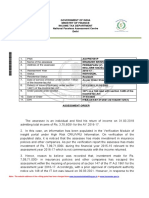

- Assessmnt Order Us 144 & 147 - Dhanush - AY 2016-17Document3 pagesAssessmnt Order Us 144 & 147 - Dhanush - AY 2016-17client itNo ratings yet

- Public E-Carbon Efficient FundDocument1 pagePublic E-Carbon Efficient FundEileen LauNo ratings yet

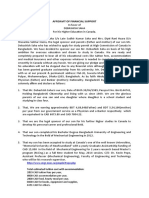

- AFFIDAVIT OF FINANCIAL SUPPORT - Parents - DebashishDocument6 pagesAFFIDAVIT OF FINANCIAL SUPPORT - Parents - DebashishImdad KhanNo ratings yet

- Group 07 - MFS - Vaswani IPO ScamDocument8 pagesGroup 07 - MFS - Vaswani IPO ScamSonu YadavNo ratings yet