You might also like

- 44 Bed Detox and Residential Substance Abuse Treatment Facility Proforma - Chapman TustinDocument4 pages44 Bed Detox and Residential Substance Abuse Treatment Facility Proforma - Chapman TustinDaniel L. Case, Sr.100% (2)

- International Financial Management: 7 EditionDocument47 pagesInternational Financial Management: 7 Editionbiradardnyaneshwar90No ratings yet

- Income Taxes For CorporationsDocument35 pagesIncome Taxes For CorporationsKurt SoriaoNo ratings yet

- Surviving the Aftermath of Covid-19:How Business Can Survive in the New EraFrom EverandSurviving the Aftermath of Covid-19:How Business Can Survive in the New EraNo ratings yet

- Elements of Financial StatementsDocument6 pagesElements of Financial StatementsAngelAnneDeJesus86% (7)

- What Is Gross Income (Or Taxable Gross Income) ?Document24 pagesWhat Is Gross Income (Or Taxable Gross Income) ?Joe P PokaranNo ratings yet

- Chapter 14-Regular Income Taxation: IndividualsDocument28 pagesChapter 14-Regular Income Taxation: Individualsarjay matanguihan100% (2)

- FAC1601 Assignment 5Document73 pagesFAC1601 Assignment 5Kgomotso RamodikeNo ratings yet

- Mistake: English Law: To Their Original Positions As If The Contract Has Been PerformedDocument38 pagesMistake: English Law: To Their Original Positions As If The Contract Has Been Performed承艳100% (1)

- M7 - P1 Individual Income Taxation - Students'Document66 pagesM7 - P1 Individual Income Taxation - Students'micaella pasionNo ratings yet

- Train LawDocument35 pagesTrain LawRAIZA GRACE OAMILNo ratings yet

- Basic Accounting Chapter 1-5 QuizzesDocument6 pagesBasic Accounting Chapter 1-5 QuizzesLuna Shi100% (1)

- Module 07 - Introduction To Regular Income TaxDocument25 pagesModule 07 - Introduction To Regular Income TaxJANELLE NUEZNo ratings yet

- Module 07 Introduction To Regular Income Tax 3 2Document21 pagesModule 07 Introduction To Regular Income Tax 3 2Joshua BazarNo ratings yet

- Taxation 8-Preferential Taxation: Pre-TestDocument4 pagesTaxation 8-Preferential Taxation: Pre-TestCharles Decripito Flores100% (1)

- Tax Reform For Acceleration and Inclusion LawDocument28 pagesTax Reform For Acceleration and Inclusion LawGloriosa SzeNo ratings yet

- Regular Income Taxation: Individuals: Chapter Overview and ObjectivesDocument27 pagesRegular Income Taxation: Individuals: Chapter Overview and ObjectivesJane HandumonNo ratings yet

- Tax 605Document5 pagesTax 605NhajNo ratings yet

- PEZA NotesDocument25 pagesPEZA NotesJane BiancaNo ratings yet

- Written Report Week 8 Income TaxDocument16 pagesWritten Report Week 8 Income Taxdevy mar topiaNo ratings yet

- Module 07 - Overview of Regular Income TaxationDocument32 pagesModule 07 - Overview of Regular Income TaxationTrixie OnglaoNo ratings yet

- Full Length of Module 1 Income Taxation On Individuals PDFDocument35 pagesFull Length of Module 1 Income Taxation On Individuals PDFHermosura ChristineNo ratings yet

- Income Taxation: Gross Revenue PXXXXX Deductions XXXXXDocument8 pagesIncome Taxation: Gross Revenue PXXXXX Deductions XXXXXPSHNo ratings yet

- Module 07 Introduction To Regular Income TaxDocument21 pagesModule 07 Introduction To Regular Income TaxJeon KookieNo ratings yet

- Copy Individual Income TaxDocument10 pagesCopy Individual Income TaxMari Louis Noriell MejiaNo ratings yet

- Abm Income TaxationDocument8 pagesAbm Income TaxationNardsdel RiveraNo ratings yet

- Covid-19 Effect On Tax CollectionDocument7 pagesCovid-19 Effect On Tax Collectionannemorano126No ratings yet

- Income Taxation For Domestic CorporationDocument6 pagesIncome Taxation For Domestic CorporationPaul Anthony AspuriaNo ratings yet

- Week 7: Taxation of Individuals (Non Residents and Aliens) and General Professional PartnershipsDocument6 pagesWeek 7: Taxation of Individuals (Non Residents and Aliens) and General Professional PartnershipsEddie Mar JagunapNo ratings yet

- Transfer Tax Train Law 2Document6 pagesTransfer Tax Train Law 2Mark DasiganNo ratings yet

- BLT 134 Chapter 4Document4 pagesBLT 134 Chapter 4MJNo ratings yet

- Stratax Online DiscussionDocument8 pagesStratax Online DiscussionRawr rawrNo ratings yet

- CorporationDocument83 pagesCorporationAlson Keith L CastroNo ratings yet

- Tax XXXXDocument60 pagesTax XXXXGerald Bowe ResuelloNo ratings yet

- Institute Progressive Tax Reform and More Effective Tax Collection, Indexing Taxes To Inflation. A Tax Reform Package Will Be Submitted To Congress by September 2016Document28 pagesInstitute Progressive Tax Reform and More Effective Tax Collection, Indexing Taxes To Inflation. A Tax Reform Package Will Be Submitted To Congress by September 2016RAIZA GRACE OAMILNo ratings yet

- A Guide To Taxation in The PhilippinesDocument5 pagesA Guide To Taxation in The PhilippinesNathaniel MartinezNo ratings yet

- Lesson 3 MGT207 Escape From Taxation Prepared by SKM (Additional)Document25 pagesLesson 3 MGT207 Escape From Taxation Prepared by SKM (Additional)Alkhair SangcopanNo ratings yet

- 3.2 Business Profit TaxDocument49 pages3.2 Business Profit TaxBizu AtnafuNo ratings yet

- Ass&Sa Claro Bac07-18Document28 pagesAss&Sa Claro Bac07-18Steffi Anne D. ClaroNo ratings yet

- Income Tax of IndividualsDocument27 pagesIncome Tax of IndividualsChristmaNo ratings yet

- IFBPDocument11 pagesIFBPmohanraokp2279No ratings yet

- Intro RIT - Exclusion in GIDocument23 pagesIntro RIT - Exclusion in GIdelacruzrojohn600No ratings yet

- Orca Share Media1613096356709 6765816501330676436Document9 pagesOrca Share Media1613096356709 6765816501330676436Mara Gianina QuejadaNo ratings yet

- DTB Orientation (PIT & CIT) FINALDocument37 pagesDTB Orientation (PIT & CIT) FINALCourt NanquilNo ratings yet

- Ryan RemsDocument56 pagesRyan Remsmimi supasNo ratings yet

- Clwtaxn - Lecture Week4Document17 pagesClwtaxn - Lecture Week4Maria Angelika ArcillaNo ratings yet

- Chapter 7: Introduction To Regular Income TaxDocument5 pagesChapter 7: Introduction To Regular Income TaxArna Kaira Kjell DiestraNo ratings yet

- Train LawDocument41 pagesTrain LawJoana Lyn GalisimNo ratings yet

- Tax Credit For Tax Paid To A Foreign CountryDocument3 pagesTax Credit For Tax Paid To A Foreign CountryCaile Peñora CajuraoNo ratings yet

- Osd CorrectionDocument2 pagesOsd CorrectionSai BomNo ratings yet

- 3 Tax Deductible Expenses With Limitations in PhilippinesDocument2 pages3 Tax Deductible Expenses With Limitations in PhilippinesChristine Bobis100% (1)

- Pro Pyme GeneralDocument11 pagesPro Pyme GeneralSofia OgaldeNo ratings yet

- Regular Income TaxationDocument2 pagesRegular Income TaxationAlyza CaculitanNo ratings yet

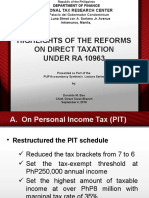

- Highlights of The Reforms On Direct Taxation UNDER RA 10963: National Tax Research CenterDocument33 pagesHighlights of The Reforms On Direct Taxation UNDER RA 10963: National Tax Research CenterCourt NanquilNo ratings yet

- Tax.103 2 Corporate Income Taxation StudentsDocument23 pagesTax.103 2 Corporate Income Taxation StudentsJames R JunioNo ratings yet

- Company Tax (Cameroon) - Chapter 1Document5 pagesCompany Tax (Cameroon) - Chapter 1Tagem AlainNo ratings yet

- M6 - Deductions P2 Students'Document53 pagesM6 - Deductions P2 Students'micaella pasionNo ratings yet

- Taxation Interest Income and Its Effect On SavingsDocument25 pagesTaxation Interest Income and Its Effect On SavingsTimothy AngeloNo ratings yet

- Morales Taxation Topic 2 Tax On IndividualsDocument23 pagesMorales Taxation Topic 2 Tax On IndividualsMary Joice Delos santosNo ratings yet

- Tax RateDocument10 pagesTax Rateusha chimariyaNo ratings yet

- Oclarit TAX PEZA Report PPT 1Document31 pagesOclarit TAX PEZA Report PPT 1charissetosloladoNo ratings yet

- Department of Accountancy Income Taxation - Quizzer Answer Key Case 1Document11 pagesDepartment of Accountancy Income Taxation - Quizzer Answer Key Case 1Dominic BulaclacNo ratings yet

- INCOME AND BUSINESS TAXATION FinalsDocument21 pagesINCOME AND BUSINESS TAXATION FinalsAbegail BlancoNo ratings yet

- Lecture 1 - Introduction To Income TaxDocument27 pagesLecture 1 - Introduction To Income TaxMimi kupiNo ratings yet

- TAXATION Finals-ReviewerDocument4 pagesTAXATION Finals-ReviewerABM1205 Lancanan Ma. SheilaNo ratings yet

- 450 499 PDFDocument44 pages450 499 PDFSamuelNo ratings yet

- Invoice Letter 11 Nov 2021Document8 pagesInvoice Letter 11 Nov 2021Suvi AzkaNo ratings yet

- Discuss How Any Company Can Become A Multinational Company What Are Some TheDocument2 pagesDiscuss How Any Company Can Become A Multinational Company What Are Some TheAmara jrrNo ratings yet

- PFRS 9Document7 pagesPFRS 9Carissa CestinaNo ratings yet

- Using Familiar Words SL - AnswerDocument5 pagesUsing Familiar Words SL - Answerashek mahmoodNo ratings yet

- TQM - TPMDocument11 pagesTQM - TPMPandi ANo ratings yet

- Report - Comparative Baseline Study On Establishing The Startup Policy in TanzaniaDocument101 pagesReport - Comparative Baseline Study On Establishing The Startup Policy in TanzaniaBongani SaidiNo ratings yet

- Bgcse Coursework CommerceDocument8 pagesBgcse Coursework Commercepkhdyfdjd100% (2)

- 12 Accountancy Keynotes Ch09 Redemption of DebenturesDocument4 pages12 Accountancy Keynotes Ch09 Redemption of DebenturesiisjafferNo ratings yet

- ObligationDocument2 pagesObligationJustine Airra OndoyNo ratings yet

- Refer To E4 9 A Cardon S Winterized Cleaned and Covered PDFDocument1 pageRefer To E4 9 A Cardon S Winterized Cleaned and Covered PDFTaimour HassanNo ratings yet

- Net Infotech System NIS/G/21-22/0340 31-Jul-21: Tax InvoiceDocument1 pageNet Infotech System NIS/G/21-22/0340 31-Jul-21: Tax InvoicehhNo ratings yet

- Ank ResumeDocument2 pagesAnk ResumeGouresh ChauhanNo ratings yet

- Case StudyDocument16 pagesCase StudyRocket SinghNo ratings yet

- Transportation and Economic Development Challenges - (4 Distance in The Existence of Political Pathologies Rationalized Tran... )Document13 pagesTransportation and Economic Development Challenges - (4 Distance in The Existence of Political Pathologies Rationalized Tran... )monazaNo ratings yet

- CA. Nitin Goel: CanitinDocument4 pagesCA. Nitin Goel: CanitinSri AssociatesNo ratings yet

- Department of Labor: Cedapr01Document28 pagesDepartment of Labor: Cedapr01USA_DepartmentOfLaborNo ratings yet

- SEAI EXEED Grant GuidelinesDocument46 pagesSEAI EXEED Grant GuidelinesHarsha RajendranNo ratings yet

- November 2022Document4 pagesNovember 2022NURSAJIDANo ratings yet

- Quiz 514Document17 pagesQuiz 514Haris NoonNo ratings yet

- Advanced Introduction To Post Keynesian Economics - J. E. King Edward Elgar Publishing (2015) (Elgar Advanced Introductions)Document169 pagesAdvanced Introduction To Post Keynesian Economics - J. E. King Edward Elgar Publishing (2015) (Elgar Advanced Introductions)Lucas Jean de Miranda CoelhoNo ratings yet

- Ogl 182681680521100076Document5 pagesOgl 182681680521100076Rajesh KumarNo ratings yet

- Marginal Costing & Absorption Costing: Garrison, Noreen, Brewer, Cheng & Yuen Mcgraw-Hill Education (Asia)Document56 pagesMarginal Costing & Absorption Costing: Garrison, Noreen, Brewer, Cheng & Yuen Mcgraw-Hill Education (Asia)Đăng NguyễnNo ratings yet

- Printed by SYSUSER: Dial Toll Free 1912 For Bill & Supply ComplaintsDocument1 pagePrinted by SYSUSER: Dial Toll Free 1912 For Bill & Supply ComplaintsAartiNo ratings yet

- Gujarat Technological UniversityDocument1 pageGujarat Technological UniversityHarsh GakhreNo ratings yet