You might also like

- Earned Value Project Management (Fourth Edition)From EverandEarned Value Project Management (Fourth Edition)Rating: 1 out of 5 stars1/5 (2)

- Budgetary Planning: Answers To QuestionsDocument33 pagesBudgetary Planning: Answers To QuestionsCharlene MakNo ratings yet

- Managing Successful Projects with PRINCE2 2009 EditionFrom EverandManaging Successful Projects with PRINCE2 2009 EditionRating: 4 out of 5 stars4/5 (3)

- Cost Behavior: Answers To QuestionsDocument57 pagesCost Behavior: Answers To QuestionsCharlene MakNo ratings yet

- Chapter 11 Capital Budgeting: Answers To QuestionsDocument35 pagesChapter 11 Capital Budgeting: Answers To Questionsafsdasdf3qf4341f4asDNo ratings yet

- Managerial Accounting 2nd Edition Whitecotton Solutions Manual 1Document54 pagesManagerial Accounting 2nd Edition Whitecotton Solutions Manual 1margaret100% (50)

- Solutions Chapter 8 - 2d EditionDocument29 pagesSolutions Chapter 8 - 2d Editionafsdasdf3qf4341f4asDNo ratings yet

- Solutions Chapter 8 - 3rd EditionDocument30 pagesSolutions Chapter 8 - 3rd Editionafsdasdf3qf4341f4asDNo ratings yet

- Ch13 SolutionsManual FINAL 050417Document30 pagesCh13 SolutionsManual FINAL 050417Natalie ChoiNo ratings yet

- Chapter 13 - SolutionsManual - FINAL - 050417 PDFDocument30 pagesChapter 13 - SolutionsManual - FINAL - 050417 PDFNatalie ChoiNo ratings yet

- Solutions Chapter 9Document37 pagesSolutions Chapter 9Brenda WijayaNo ratings yet

- Fundamentals of Financial Accounting 6th Edition Phillips Solutions ManualDocument25 pagesFundamentals of Financial Accounting 6th Edition Phillips Solutions ManualJadeFischerqtcj98% (53)

- Fundamentals of Financial Accounting 5th Edition Phillips Solutions ManualDocument35 pagesFundamentals of Financial Accounting 5th Edition Phillips Solutions Manualalvacalliopeewc96% (25)

- Full Download Fundamentals of Financial Accounting 6th Edition Phillips Solutions ManualDocument35 pagesFull Download Fundamentals of Financial Accounting 6th Edition Phillips Solutions Manualleavings.strix.b9xf100% (39)

- Chuong 6Document35 pagesChuong 6mummimNo ratings yet

- Financial Management Theory and Practice 14Th Edition Brigham Solutions Manual Full Chapter PDFDocument36 pagesFinancial Management Theory and Practice 14Th Edition Brigham Solutions Manual Full Chapter PDFchristopher.ridgeway589100% (10)

- Mid Term IT Project MGNTDocument10 pagesMid Term IT Project MGNTmwaseem2011No ratings yet

- University of Gloucestershire: MBA-1 (GROUP-D)Document10 pagesUniversity of Gloucestershire: MBA-1 (GROUP-D)Nikunj PatelNo ratings yet

- Chapter 5Document48 pagesChapter 5aluatNo ratings yet

- Microeconomics Principles Problems and Policies Mcconnell 20th Edition Solutions ManualDocument14 pagesMicroeconomics Principles Problems and Policies Mcconnell 20th Edition Solutions ManualVictoriaWilliamsegtnm100% (94)

- Solution Manual For Fundamentals of Financial Accounting 5Th Edition by Phillips Libby Isbn 0078025915 9780078025914 Full Chapter PDFDocument36 pagesSolution Manual For Fundamentals of Financial Accounting 5Th Edition by Phillips Libby Isbn 0078025915 9780078025914 Full Chapter PDFnancy.rodriguez985100% (11)

- Fundamentals of Financial Accounting Canadian Canadian 4th Edition Phillips Solutions ManualDocument17 pagesFundamentals of Financial Accounting Canadian Canadian 4th Edition Phillips Solutions ManualJacobFloresxbpcn100% (50)

- 2015 Dse Econ 1Document15 pages2015 Dse Econ 1Victor ChanNo ratings yet

- Economics Principles Problems and Policies Mcconnell 20th Edition Solutions ManualDocument14 pagesEconomics Principles Problems and Policies Mcconnell 20th Edition Solutions ManualCatherineJohnsonabpg100% (41)

- CA Financial Reporting Book PDFDocument516 pagesCA Financial Reporting Book PDFPrashant NeupaneNo ratings yet

- Software Project ManagementDocument33 pagesSoftware Project ManagementMuhammad QasimNo ratings yet

- Economics 21st Edition McConnell Solutions Manual 1Document14 pagesEconomics 21st Edition McConnell Solutions Manual 1melissa100% (28)

- ch10 Project Monitoring & ControlDocument29 pagesch10 Project Monitoring & ControlLucky Luke100% (1)

- Solution Manual For Intermediate Accounting Principles and Analysis 2nd Edition by WarfieldDocument25 pagesSolution Manual For Intermediate Accounting Principles and Analysis 2nd Edition by WarfieldJosephWilliamsjfyae100% (66)

- Advanced Audit and Assurance - International: Specimen Exam - September 2022Document35 pagesAdvanced Audit and Assurance - International: Specimen Exam - September 2022Asif RiazNo ratings yet

- The Basics of Capital Budgeting: Learning ObjectivesDocument35 pagesThe Basics of Capital Budgeting: Learning Objectivesnahnah2121No ratings yet

- Activity - Capital Investment AnalysisDocument4 pagesActivity - Capital Investment AnalysisKATHRYN CLAUDETTE RESENTENo ratings yet

- Project Concept and FormulationDocument56 pagesProject Concept and FormulationWP 2-1-PR Katubedda-CESLNo ratings yet

- Libby 4ce Solutions Manual - Ch05Document55 pagesLibby 4ce Solutions Manual - Ch057595522No ratings yet

- Course Materials BAFINMAX Week8Document8 pagesCourse Materials BAFINMAX Week8emmanvillafuerteNo ratings yet

- Cost Accounting A Managerial Emphasis 2nd Edition Horngren Solutions ManualDocument57 pagesCost Accounting A Managerial Emphasis 2nd Edition Horngren Solutions Manualbotryosetamarinh1m7a100% (22)

- 2KES Balance Carry ForwardDocument10 pages2KES Balance Carry Forwardnguyencaohuy100% (1)

- Managerial Accounting 3rd Edition Whitecotton Solutions Manual DownloadDocument55 pagesManagerial Accounting 3rd Edition Whitecotton Solutions Manual DownloadCharlotte Jackson100% (22)

- Chapter 4Document22 pagesChapter 4bikilahussenNo ratings yet

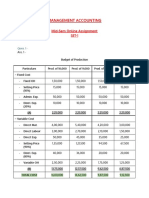

- Arjun Salwan - Management Accounting (SET-1)Document3 pagesArjun Salwan - Management Accounting (SET-1)Arjun SalwanNo ratings yet

- EUE43E Business Management Simulation Manual Prague 2010Document48 pagesEUE43E Business Management Simulation Manual Prague 2010HarpagannNo ratings yet

- POM Planning Scheduling Part1 2021Document12 pagesPOM Planning Scheduling Part1 2021zunkuzabiNo ratings yet

- Managerial Accounting 4th Edition Wild Solutions Manual 1Document50 pagesManagerial Accounting 4th Edition Wild Solutions Manual 1sarah100% (51)

- Managerial Accounting 4th Edition Wild Solutions Manual 1Document36 pagesManagerial Accounting 4th Edition Wild Solutions Manual 1crystalhensonfxjemnbkwg100% (23)

- Victoria Chemicals Plc. (A) The Merseyside ProjectDocument9 pagesVictoria Chemicals Plc. (A) The Merseyside ProjectAs17 As17No ratings yet

- Solution Manual For Intermediate Accounting Principles and Analysis 2nd Edition by WarfieldDocument23 pagesSolution Manual For Intermediate Accounting Principles and Analysis 2nd Edition by WarfieldTiffanyMilleredpn100% (39)

- 16 SolutionsDocument10 pages16 SolutionsFebrie Dharma KuncoroNo ratings yet

- Works To Be Done in ROCKWELL AMCDocument2 pagesWorks To Be Done in ROCKWELL AMCgopisettyNo ratings yet

- Module 4 SCMDocument10 pagesModule 4 SCMKhai LaNo ratings yet

- FFM12, CH 13, IM, 01-08-09Document20 pagesFFM12, CH 13, IM, 01-08-09seventeenlopez100% (1)

- Chapter 07 - Businesses and The Costs of ProductionDocument11 pagesChapter 07 - Businesses and The Costs of ProductionErjon SkordhaNo ratings yet

- 2022 CFA Curriculum Changes - Our Super Summary - 300hoursDocument3 pages2022 CFA Curriculum Changes - Our Super Summary - 300hoursClareNo ratings yet

- Solution Manual For Managerial Accounting 4th Edition Stacey Whitecotton Robert Libby Fred PhillipsDocument38 pagesSolution Manual For Managerial Accounting 4th Edition Stacey Whitecotton Robert Libby Fred PhillipsElizabethMoodyxwym100% (41)

- Analyzing and Interpreting Financial Statements: Learning Objectives - Coverage by QuestionDocument37 pagesAnalyzing and Interpreting Financial Statements: Learning Objectives - Coverage by QuestionpoollookNo ratings yet

- Cornerstones of Managerial Accounting 6th Edition Mowen Solutions Manual 1Document36 pagesCornerstones of Managerial Accounting 6th Edition Mowen Solutions Manual 1dawnlarsentsgiwnqczm100% (25)

- Cornerstones of Managerial Accounting 6Th Edition Mowen Solutions Manual Full Chapter PDFDocument36 pagesCornerstones of Managerial Accounting 6Th Edition Mowen Solutions Manual Full Chapter PDFrenee.crawford887100% (10)

- Ch. 8 - Making Capital Investment Decisions M New Tax LawDocument25 pagesCh. 8 - Making Capital Investment Decisions M New Tax LawMazen SalahNo ratings yet

- Mis 3300 Feasibility AnalysisDocument28 pagesMis 3300 Feasibility Analysisapi-281205316No ratings yet

- Project Development & Implementation For Strategic ManagersDocument19 pagesProject Development & Implementation For Strategic ManagersParadise 2026No ratings yet

- f5 SQB 15 Sample PDFDocument51 pagesf5 SQB 15 Sample PDFCecilia Mfene Sekubuwane0% (1)

- ACCT 2200 - Chapter 3 Part 2 CompletedDocument20 pagesACCT 2200 - Chapter 3 Part 2 Completedafsdasdf3qf4341f4asDNo ratings yet

- Bus Service FareDocument5 pagesBus Service Fareafsdasdf3qf4341f4asDNo ratings yet

- Chapter 11 Capital Budgeting: Answers To QuestionsDocument31 pagesChapter 11 Capital Budgeting: Answers To Questionssernhaow_658673991No ratings yet

- Solutions Chapter 8 - 3rd EditionDocument30 pagesSolutions Chapter 8 - 3rd Editionafsdasdf3qf4341f4asDNo ratings yet

- Solutions Chapter 10 - 3rd EditionDocument41 pagesSolutions Chapter 10 - 3rd Editionafsdasdf3qf4341f4asDNo ratings yet

- Review Session - 28/04/2017: Question 2: The Following Information Is Available On A New Piece of EquipmentDocument4 pagesReview Session - 28/04/2017: Question 2: The Following Information Is Available On A New Piece of Equipmentafsdasdf3qf4341f4asDNo ratings yet

- ACCT 2200 - Chapter 9Document26 pagesACCT 2200 - Chapter 9afsdasdf3qf4341f4asDNo ratings yet

- Solution Case StudyDocument8 pagesSolution Case Studyafsdasdf3qf4341f4asDNo ratings yet

- ACCT 2200 - Chapter 11 P2 - With SolutionsDocument26 pagesACCT 2200 - Chapter 11 P2 - With Solutionsafsdasdf3qf4341f4asDNo ratings yet

- Capital Budgeting MethodsDocument39 pagesCapital Budgeting Methodsafsdasdf3qf4341f4asDNo ratings yet

- ACCT 2200 - Chapter 10Document29 pagesACCT 2200 - Chapter 10afsdasdf3qf4341f4asDNo ratings yet

- ACCT 2200 - Chapter 8Document27 pagesACCT 2200 - Chapter 8afsdasdf3qf4341f4asDNo ratings yet

- Capital Budgeting MethodsDocument39 pagesCapital Budgeting Methodsafsdasdf3qf4341f4asDNo ratings yet

- ACCT 2200 - Chapter 11 P2 - With SolutionsDocument26 pagesACCT 2200 - Chapter 11 P2 - With Solutionsafsdasdf3qf4341f4asDNo ratings yet

- ACCT 2200 - Chapter 8Document27 pagesACCT 2200 - Chapter 8afsdasdf3qf4341f4asDNo ratings yet

- ACCT 2200 - Chapter 10Document29 pagesACCT 2200 - Chapter 10afsdasdf3qf4341f4asDNo ratings yet

- ACCT 2200 - Chapter 9Document26 pagesACCT 2200 - Chapter 9afsdasdf3qf4341f4asDNo ratings yet

- 17 Operating CostingDocument5 pages17 Operating CostingDeepak R GoradNo ratings yet

- Accounting For Overheads: ACCA F2 Chapter 7Document21 pagesAccounting For Overheads: ACCA F2 Chapter 7Ibrahim JawedNo ratings yet

- Decision Making: Relevant Costs and BenefitsDocument39 pagesDecision Making: Relevant Costs and BenefitsAira Nhaira MecateNo ratings yet

- Variable and Absorption Costing Problems Without SolutionsDocument4 pagesVariable and Absorption Costing Problems Without SolutionsMeca CorpuzNo ratings yet

- Managerial Accounting 2nd Edition Whitecotton Solutions ManualDocument35 pagesManagerial Accounting 2nd Edition Whitecotton Solutions Manualoutroarzimocca469r100% (21)

- Cost Accounting assignment on inventory levels, accounting entries for spoiled goods, piece rate incentives, factory overhead variancesDocument5 pagesCost Accounting assignment on inventory levels, accounting entries for spoiled goods, piece rate incentives, factory overhead variancesM Noaman AkbarNo ratings yet

- CH 06 IllustrationDocument2 pagesCH 06 Illustrationlauhouian20No ratings yet

- PlanSwift 9.1 User ManualDocument260 pagesPlanSwift 9.1 User ManualAdrian Albizuris100% (1)

- CVP Analysis - Docx Final PDFDocument146 pagesCVP Analysis - Docx Final PDFDivyapratap Singh ChauhanNo ratings yet

- FARQ1Q2 MendozaDocument6 pagesFARQ1Q2 MendozaLeane MarcoletaNo ratings yet

- B. Sales Less Variable: Absorption CostingDocument3 pagesB. Sales Less Variable: Absorption CostingLaraNo ratings yet

- Question 1 of 20 Accounting For ManagersDocument8 pagesQuestion 1 of 20 Accounting For ManagersgghhsdNo ratings yet

- Activity - Accounting For Overhead: Problem 1Document2 pagesActivity - Accounting For Overhead: Problem 1Nick ivan AlvaresNo ratings yet

- Marginal CostingDocument42 pagesMarginal CostingAbdifatah SaidNo ratings yet

- Decision-Making Using Marginal Costing-IDocument11 pagesDecision-Making Using Marginal Costing-Iapi-27014089100% (3)

- BuddDocument34 pagesBuddPeishi Ong50% (2)

- CN04HODocument51 pagesCN04HOAbood AlissaNo ratings yet

- Jorpati, Kathmandu Pre-Board Examination-2077 Subject: Principles of Accounting II Grade: XII Time: 3 Hrs FM: 100 PM: 32Document3 pagesJorpati, Kathmandu Pre-Board Examination-2077 Subject: Principles of Accounting II Grade: XII Time: 3 Hrs FM: 100 PM: 32Abin DhakalNo ratings yet

- Bab 4 Cost System and Cost AccumulationDocument6 pagesBab 4 Cost System and Cost AccumulationAndi SupenoNo ratings yet

- Tentative Suggested Answer - Nov. 22 ExamDocument20 pagesTentative Suggested Answer - Nov. 22 ExamHemant RathvaNo ratings yet

- Chapter 1 Question Review - 102Document5 pagesChapter 1 Question Review - 102Mark Joseph CanoNo ratings yet

- N5 Building Administration Lecturer GuideDocument76 pagesN5 Building Administration Lecturer Guideyandatshabalala75No ratings yet

- Formules Managerial Accounting 1Document56 pagesFormules Managerial Accounting 1Nour MkaouriNo ratings yet

- Solution Manual For Horngrens Accounting The Managerial Chapters 10Th Edition Nobles Mattison Matsumura 0133117715 9780133117714 Full Chapter PDFDocument36 pagesSolution Manual For Horngrens Accounting The Managerial Chapters 10Th Edition Nobles Mattison Matsumura 0133117715 9780133117714 Full Chapter PDFgerard.lopez310100% (11)

- A. Calculate The Break-Even Dollar Sales For The MonthDocument25 pagesA. Calculate The Break-Even Dollar Sales For The MonthPriyankaNo ratings yet

- Management AccountingDocument11 pagesManagement AccountingMalikwaheedNo ratings yet

- MIC Stove Final PresentationDocument24 pagesMIC Stove Final PresentationObi ChrisNo ratings yet

- Relevant Costing by A Bobadilla PDFDocument43 pagesRelevant Costing by A Bobadilla PDFAnalieSullano100% (4)

- Mock Final Departmental Exam - Accounting 201 - NCABALUNA 1Document9 pagesMock Final Departmental Exam - Accounting 201 - NCABALUNA 1francis albaracinNo ratings yet

- Management Accounting ConceptsDocument12 pagesManagement Accounting ConceptsManan ShahNo ratings yet

- Packing for Mars: The Curious Science of Life in the VoidFrom EverandPacking for Mars: The Curious Science of Life in the VoidRating: 4 out of 5 stars4/5 (1395)

- Sully: The Untold Story Behind the Miracle on the HudsonFrom EverandSully: The Untold Story Behind the Miracle on the HudsonRating: 4 out of 5 stars4/5 (103)

- Hero Found: The Greatest POW Escape of the Vietnam WarFrom EverandHero Found: The Greatest POW Escape of the Vietnam WarRating: 4 out of 5 stars4/5 (19)

- The Fabric of Civilization: How Textiles Made the WorldFrom EverandThe Fabric of Civilization: How Textiles Made the WorldRating: 4.5 out of 5 stars4.5/5 (57)

- Transformed: Moving to the Product Operating ModelFrom EverandTransformed: Moving to the Product Operating ModelRating: 4 out of 5 stars4/5 (1)

- The Beekeeper's Lament: How One Man and Half a Billion Honey Bees Help Feed AmericaFrom EverandThe Beekeeper's Lament: How One Man and Half a Billion Honey Bees Help Feed AmericaNo ratings yet

- The Intel Trinity: How Robert Noyce, Gordon Moore, and Andy Grove Built the World's Most Important CompanyFrom EverandThe Intel Trinity: How Robert Noyce, Gordon Moore, and Andy Grove Built the World's Most Important CompanyNo ratings yet

- The Technology Trap: Capital, Labor, and Power in the Age of AutomationFrom EverandThe Technology Trap: Capital, Labor, and Power in the Age of AutomationRating: 4.5 out of 5 stars4.5/5 (46)

- Faster: How a Jewish Driver, an American Heiress, and a Legendary Car Beat Hitler's BestFrom EverandFaster: How a Jewish Driver, an American Heiress, and a Legendary Car Beat Hitler's BestRating: 4 out of 5 stars4/5 (28)

- The Weather Machine: A Journey Inside the ForecastFrom EverandThe Weather Machine: A Journey Inside the ForecastRating: 3.5 out of 5 stars3.5/5 (31)

- Einstein's Fridge: How the Difference Between Hot and Cold Explains the UniverseFrom EverandEinstein's Fridge: How the Difference Between Hot and Cold Explains the UniverseRating: 4.5 out of 5 stars4.5/5 (50)

- The Quiet Zone: Unraveling the Mystery of a Town Suspended in SilenceFrom EverandThe Quiet Zone: Unraveling the Mystery of a Town Suspended in SilenceRating: 3.5 out of 5 stars3.5/5 (23)

- The End of Craving: Recovering the Lost Wisdom of Eating WellFrom EverandThe End of Craving: Recovering the Lost Wisdom of Eating WellRating: 4.5 out of 5 stars4.5/5 (80)

- 35 Miles From Shore: The Ditching and Rescue of ALM Flight 980From Everand35 Miles From Shore: The Ditching and Rescue of ALM Flight 980Rating: 4 out of 5 stars4/5 (21)

- Recording Unhinged: Creative and Unconventional Music Recording TechniquesFrom EverandRecording Unhinged: Creative and Unconventional Music Recording TechniquesNo ratings yet

- Pale Blue Dot: A Vision of the Human Future in SpaceFrom EverandPale Blue Dot: A Vision of the Human Future in SpaceRating: 4.5 out of 5 stars4.5/5 (586)

- The Path Between the Seas: The Creation of the Panama Canal, 1870-1914From EverandThe Path Between the Seas: The Creation of the Panama Canal, 1870-1914Rating: 4.5 out of 5 stars4.5/5 (124)

- A Place of My Own: The Architecture of DaydreamsFrom EverandA Place of My Own: The Architecture of DaydreamsRating: 4 out of 5 stars4/5 (241)

- Reality+: Virtual Worlds and the Problems of PhilosophyFrom EverandReality+: Virtual Worlds and the Problems of PhilosophyRating: 4 out of 5 stars4/5 (24)

- Data-ism: The Revolution Transforming Decision Making, Consumer Behavior, and Almost Everything ElseFrom EverandData-ism: The Revolution Transforming Decision Making, Consumer Behavior, and Almost Everything ElseRating: 3.5 out of 5 stars3.5/5 (12)

- The Future of Geography: How the Competition in Space Will Change Our WorldFrom EverandThe Future of Geography: How the Competition in Space Will Change Our WorldRating: 4.5 out of 5 stars4.5/5 (4)

- Permaculture for the Rest of Us: Abundant Living on Less than an AcreFrom EverandPermaculture for the Rest of Us: Abundant Living on Less than an AcreRating: 4.5 out of 5 stars4.5/5 (33)

- Dirt to Soil: One Family’s Journey into Regenerative AgricultureFrom EverandDirt to Soil: One Family’s Journey into Regenerative AgricultureRating: 5 out of 5 stars5/5 (125)