You might also like

- Hacking and Cracking TechniguesDocument16 pagesHacking and Cracking TechniguesEric MuiaNo ratings yet

- E-Payment SystemDocument19 pagesE-Payment SystemChuong MaiNo ratings yet

- A Study On Electronic Payment System in IndiaDocument67 pagesA Study On Electronic Payment System in IndiaAvula Shravan Yadav50% (2)

- Design Procedure of A Wire RopeDocument1 pageDesign Procedure of A Wire RopeKutty Aravind100% (3)

- Networker Errors and ResolutionsDocument8 pagesNetworker Errors and Resolutionspulkit632No ratings yet

- Growth of Digital Transactions in Transforming EconomyDocument4 pagesGrowth of Digital Transactions in Transforming EconomyInternational Journal of Innovative Science and Research Technology100% (2)

- Crosswalk For CCNA 4 Labs and ActivitiesDocument212 pagesCrosswalk For CCNA 4 Labs and Activitiesaft3rmath2100% (1)

- Electronic Payments Recent Trends, Challenges and Emerging IssuesDocument54 pagesElectronic Payments Recent Trends, Challenges and Emerging IssuesUmesh PatilNo ratings yet

- DW 10 TDDocument151 pagesDW 10 TDjoaogasparteixeiraNo ratings yet

- Literature Review of Online Payment SystemDocument5 pagesLiterature Review of Online Payment Systemrobin75% (4)

- A o BrochureDocument20 pagesA o Brochuremax69442No ratings yet

- A Compendious Study of Online Payment SystemsDocument16 pagesA Compendious Study of Online Payment SystemsMuhammad SarmadNo ratings yet

- TGN-D-02 Fatigue Improvement of Welded StructuresDocument10 pagesTGN-D-02 Fatigue Improvement of Welded StructuresakuntayNo ratings yet

- Impact of E-Commerce On Supply Chain ManagementFrom EverandImpact of E-Commerce On Supply Chain ManagementRating: 3.5 out of 5 stars3.5/5 (3)

- Idoc - Pub Challenges and Opportunities of e Payment in Ethiopia Banking Industry With The Reference of Private Commercial BanksDocument8 pagesIdoc - Pub Challenges and Opportunities of e Payment in Ethiopia Banking Industry With The Reference of Private Commercial BanksMikiyas ToleraNo ratings yet

- Electronic Payment Systems Architecture Elements Challengesand Security Concepts An OverviewDocument13 pagesElectronic Payment Systems Architecture Elements Challengesand Security Concepts An OverviewDMT IPONo ratings yet

- Analysis of The Impact of E-Payment On Culinary Business Development in Kupang CityDocument7 pagesAnalysis of The Impact of E-Payment On Culinary Business Development in Kupang CityClariss CrisolNo ratings yet

- Secure Credits For Micro Payments Scheme Using Encrypted TechniquesDocument4 pagesSecure Credits For Micro Payments Scheme Using Encrypted TechniquesRahul SharmaNo ratings yet

- DownloadDocument22 pagesDownloadOlapade BabatundeNo ratings yet

- A Study of Electronic Payment System PDFDocument11 pagesA Study of Electronic Payment System PDFGeorgianaNo ratings yet

- A Study On Digital Banking System and MeDocument6 pagesA Study On Digital Banking System and MepranalirandilNo ratings yet

- 3.the Effect of Consumer Trust and Perceived RiskDocument8 pages3.the Effect of Consumer Trust and Perceived Riskphamuyen11012003No ratings yet

- A Multi-Agent Architecture For Electronic PaymentDocument39 pagesA Multi-Agent Architecture For Electronic PaymentLucifer MathewNo ratings yet

- Technology in Society: Feng Li, Hui Lu, Meiqian Hou, Kangle Cui, Mehdi DarbandiDocument11 pagesTechnology in Society: Feng Li, Hui Lu, Meiqian Hou, Kangle Cui, Mehdi Darbandibuat meetingNo ratings yet

- Transaction Flow in Card Payment Systems Using Mobile AgentsDocument14 pagesTransaction Flow in Card Payment Systems Using Mobile AgentsIndra Arif RamadhanNo ratings yet

- Fatonah 2018 J. Phys. Conf. Ser. 1140 012033Document8 pagesFatonah 2018 J. Phys. Conf. Ser. 1140 012033Hazel Bianca GabalesNo ratings yet

- Challenges For Indian E-Payment SystemDocument3 pagesChallenges For Indian E-Payment SystemDeepak RahejaNo ratings yet

- Jurnal Josiah Aduda and Nancy Kingoo KenyaDocument20 pagesJurnal Josiah Aduda and Nancy Kingoo KenyaJennifer WijayaNo ratings yet

- E-Payment System in Saudi Arabia PDFDocument16 pagesE-Payment System in Saudi Arabia PDFRohan MehtaNo ratings yet

- Analysis of Customer Satisfaction Factors On Ommerce Payment System Methods in IndonesiaDocument10 pagesAnalysis of Customer Satisfaction Factors On Ommerce Payment System Methods in IndonesiaRikudo AkyoshiNo ratings yet

- Degital Payment SystemDocument20 pagesDegital Payment SystemJaivik PanchalNo ratings yet

- Doolhur 2013Document4 pagesDoolhur 2013bichodavidNo ratings yet

- A Survey On E-Payment Systems: Elements, Adoption, Architecture, Challenges and Security ConceptsDocument20 pagesA Survey On E-Payment Systems: Elements, Adoption, Architecture, Challenges and Security ConceptsPooja ShahNo ratings yet

- IRJET - Review Paper On - Smart WalletDocument3 pagesIRJET - Review Paper On - Smart WalletPaul RicardoNo ratings yet

- Paper 63-Analysis of Customer Satisfaction FactorsDocument10 pagesPaper 63-Analysis of Customer Satisfaction FactorsPrayas NandaNo ratings yet

- Akinyede and Akinyede - A Prototype Design For Secure E-Commerce Payment System ModelDocument7 pagesAkinyede and Akinyede - A Prototype Design For Secure E-Commerce Payment System ModelRaphael AKINYEDENo ratings yet

- Implementing and Evaluating A Smart-M3 Platform-Based Multi-Vendor Micropayment System Pilot in The Context of Small BusinessDocument8 pagesImplementing and Evaluating A Smart-M3 Platform-Based Multi-Vendor Micropayment System Pilot in The Context of Small BusinessAditya ContohNo ratings yet

- The Effectiveness of E-Wallet SystemDocument11 pagesThe Effectiveness of E-Wallet SystemDr Yousef ElebiaryNo ratings yet

- Evaluation of Identity Access Management Frameworks On The Safety of Mobile Money Transactions Used by FinTech Companies in NairobiDocument9 pagesEvaluation of Identity Access Management Frameworks On The Safety of Mobile Money Transactions Used by FinTech Companies in NairobiInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- B - Teng & Khong (2021) Promotion E WalletDocument18 pagesB - Teng & Khong (2021) Promotion E WalletDiana HartonoNo ratings yet

- CI04054FUDocument11 pagesCI04054FUPranav KulkarniNo ratings yet

- Aibuma2011 Submission 43Document15 pagesAibuma2011 Submission 43Mayibongwe MpofuNo ratings yet

- RRL6 (Practical Research)Document15 pagesRRL6 (Practical Research)J-ira LariosaNo ratings yet

- A Study of Electronic Payment System in IndiaDocument77 pagesA Study of Electronic Payment System in IndiaNeeraj BaghelNo ratings yet

- Billing System Design Based On Internet Environmen PDFDocument8 pagesBilling System Design Based On Internet Environmen PDFYousef A SalemNo ratings yet

- Factors Influencing Adoption of Electronic Payment-213Document14 pagesFactors Influencing Adoption of Electronic Payment-213Rasyidah RosliNo ratings yet

- Case Study On The Rational of Multi-Channel Platform As A Management Information System in The Banking SectorDocument11 pagesCase Study On The Rational of Multi-Channel Platform As A Management Information System in The Banking SectorHurul AinNo ratings yet

- Combination of TAM and TPB in Internet Banking AdoptionDocument5 pagesCombination of TAM and TPB in Internet Banking AdoptionMihaela GanciuNo ratings yet

- Marks: 19 Comment: Good Effort Comment: See The Solution FileDocument4 pagesMarks: 19 Comment: Good Effort Comment: See The Solution FileShahid SaeedNo ratings yet

- Appraising The State of E-Banking Implementation in Nigeria - 013427Document7 pagesAppraising The State of E-Banking Implementation in Nigeria - 013427titus okekeNo ratings yet

- JMEITJUN0303004Document24 pagesJMEITJUN0303004divya bharathiNo ratings yet

- Adrit Main FileDocument65 pagesAdrit Main Filevishwas mishraNo ratings yet

- Online Payments Systems For E-CommerceDocument6 pagesOnline Payments Systems For E-Commerceoctal1No ratings yet

- Marketing Research Chapter 1 4Document60 pagesMarketing Research Chapter 1 4Paul Jastine RodriguezNo ratings yet

- Iciitvol.2 621 625Document6 pagesIciitvol.2 621 625Olapade BabatundeNo ratings yet

- Bank TechDocument6 pagesBank TechQuenie SagunNo ratings yet

- Unit 5Document26 pagesUnit 5Yashi BishtNo ratings yet

- Factors Affecting Customers' Adoption of Electronic Payment: An Empirical AnalysisDocument15 pagesFactors Affecting Customers' Adoption of Electronic Payment: An Empirical Analysisprabin ghimireNo ratings yet

- Factors Affecting Customers' Adoption of Electronic Payment: An Empirical AnalysisDocument17 pagesFactors Affecting Customers' Adoption of Electronic Payment: An Empirical AnalysisOsama AhmadNo ratings yet

- E-Payment in India PDFDocument6 pagesE-Payment in India PDFM GouthamNo ratings yet

- 6.the Perceived Benefit and Risk Framework of E-Wallet AdoptionDocument6 pages6.the Perceived Benefit and Risk Framework of E-Wallet Adoptionphamuyen11012003No ratings yet

- Titled ProposalDocument11 pagesTitled ProposalabceritreaNo ratings yet

- Secure and Privacy Off-Line Micro-Payments For The Resilient DeviceDocument5 pagesSecure and Privacy Off-Line Micro-Payments For The Resilient DeviceEdmund ZinNo ratings yet

- Research PosterDocument1 pageResearch PosterShad Mad Stephen CakirNo ratings yet

- PB 24 - KYC Practices in IndonesiaDocument14 pagesPB 24 - KYC Practices in IndonesiaBabe GueNo ratings yet

- Implementation of a Central Electronic Mail & Filing StructureFrom EverandImplementation of a Central Electronic Mail & Filing StructureNo ratings yet

- A Proposed Method For Text Encryption Using Symmetric and Asymmetric CryptosystemsDocument7 pagesA Proposed Method For Text Encryption Using Symmetric and Asymmetric CryptosystemsazmiNo ratings yet

- Relationship Between Ethical Leadership and Sustainability in SmaDocument16 pagesRelationship Between Ethical Leadership and Sustainability in SmaazmiNo ratings yet

- Patient Health Monitoring System Based On E-Health Monitoring ArchitectureDocument6 pagesPatient Health Monitoring System Based On E-Health Monitoring ArchitectureazmiNo ratings yet

- Evaluation of Best Steganography Tool Using Image Features: Jensi Lakdawala, Jiya RankawatDocument9 pagesEvaluation of Best Steganography Tool Using Image Features: Jensi Lakdawala, Jiya RankawatazmiNo ratings yet

- Cloud Computing - Key Hashing Cryptographic Implication Based Algorithm For Service Provider Based Encryption and DecryptionDocument7 pagesCloud Computing - Key Hashing Cryptographic Implication Based Algorithm For Service Provider Based Encryption and DecryptionazmiNo ratings yet

- Zhu Etal LQ2015 Role of Follower Identifications and Entity Morality BeliefsDocument58 pagesZhu Etal LQ2015 Role of Follower Identifications and Entity Morality BeliefsazmiNo ratings yet

- Ethical Leadership and Organization Effectiveness: Harpreet SinghDocument5 pagesEthical Leadership and Organization Effectiveness: Harpreet SinghazmiNo ratings yet

- Impact of Ethical Leadership On Employees' Performance: Moderating Role of Organizational ValuesDocument7 pagesImpact of Ethical Leadership On Employees' Performance: Moderating Role of Organizational ValuesazmiNo ratings yet

- Qing 2019Document28 pagesQing 2019azmiNo ratings yet

- Ijmra 13215Document15 pagesIjmra 13215azmiNo ratings yet

- The Influence of Ethical Leadership, Intrinsic Motivation, and Work Commitments On Job Satisfaction (Study of The Ministry of Religion, Padang City and Pasaman District) Trisno Trisno, Abror AbrorDocument9 pagesThe Influence of Ethical Leadership, Intrinsic Motivation, and Work Commitments On Job Satisfaction (Study of The Ministry of Religion, Padang City and Pasaman District) Trisno Trisno, Abror AbrorazmiNo ratings yet

- The Effect of Ethical Leadership and Organizational Justice On Employee Engagement - The Mediating Role of Employee TrustDocument6 pagesThe Effect of Ethical Leadership and Organizational Justice On Employee Engagement - The Mediating Role of Employee TrustazmiNo ratings yet

- The Presentation of Modeling An Ethical Leadership Consistent With Public Organizations in IranDocument11 pagesThe Presentation of Modeling An Ethical Leadership Consistent With Public Organizations in IranazmiNo ratings yet

- Leadership and Mobile Working: The Impact of Distance On The Superior-Subordinate Relationship and The Moderating Effects of Leadership StyleDocument14 pagesLeadership and Mobile Working: The Impact of Distance On The Superior-Subordinate Relationship and The Moderating Effects of Leadership StyleazmiNo ratings yet

- The Impact of Perceived Ethical Leadership and Trust in Leader On Job SatisfactionDocument7 pagesThe Impact of Perceived Ethical Leadership and Trust in Leader On Job SatisfactionazmiNo ratings yet

- The Relationship Between Ethical Leadership, Leadership Effectiveness and Organizational Performance: A Review of Literature in Smes ContextDocument5 pagesThe Relationship Between Ethical Leadership, Leadership Effectiveness and Organizational Performance: A Review of Literature in Smes ContextazmiNo ratings yet

- v2p019 035agbim4291Document17 pagesv2p019 035agbim4291azmiNo ratings yet

- A Graphical User Interface For EEG Analysis and ClassificationDocument5 pagesA Graphical User Interface For EEG Analysis and ClassificationazmiNo ratings yet

- The Role of Ethical Leadership On Employee Performance in Guilan University of Medical SciencesDocument8 pagesThe Role of Ethical Leadership On Employee Performance in Guilan University of Medical SciencesazmiNo ratings yet

- Smart Clothes With Bio-Sensors For ECG Monitoring: P.Sakthi Shunmuga Sundaram, N.Hari Basker, L.NatrayanDocument4 pagesSmart Clothes With Bio-Sensors For ECG Monitoring: P.Sakthi Shunmuga Sundaram, N.Hari Basker, L.NatrayanazmiNo ratings yet

- ECG Image Compression: Essentially Non-Oscillatory Interpolation Technique and Lifting SchemesDocument7 pagesECG Image Compression: Essentially Non-Oscillatory Interpolation Technique and Lifting SchemesazmiNo ratings yet

- EEG Based Brain Controlled Wheelchair For Physically Challenged PeopleDocument4 pagesEEG Based Brain Controlled Wheelchair For Physically Challenged PeopleazmiNo ratings yet

- Topics:: Mid-Point Circle Algorithm, Filling Algorithms & PolygonsDocument34 pagesTopics:: Mid-Point Circle Algorithm, Filling Algorithms & PolygonsazmiNo ratings yet

- 710 Ijar-16312Document9 pages710 Ijar-16312azmiNo ratings yet

- Area Fill Algorithms For Various Graphics Primitives: Amity University, HaryanaDocument53 pagesArea Fill Algorithms For Various Graphics Primitives: Amity University, HaryanaazmiNo ratings yet

- Mth100 Assignment 1Document3 pagesMth100 Assignment 1dibit31075No ratings yet

- Sanken Regulator-ICs-Catalog PDFDocument119 pagesSanken Regulator-ICs-Catalog PDFJoseni FigueiredoNo ratings yet

- Cariboo Pulp Paper CompanyDocument19 pagesCariboo Pulp Paper Companymn1938No ratings yet

- Dynamic Braking Unit Sikes 2016 01Document8 pagesDynamic Braking Unit Sikes 2016 01Javier VasquezNo ratings yet

- Export SVG For The Web With Illustrator CC - Creative DropletsDocument23 pagesExport SVG For The Web With Illustrator CC - Creative DropletsMiya MusashiNo ratings yet

- Aims Case Study Abu Dhabi Airport 1252006246Document2 pagesAims Case Study Abu Dhabi Airport 1252006246coolrafeekNo ratings yet

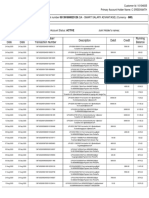

- Transaction Date Value Date Cheque Number/ Transaction Number Description Debit Credit Running BalanceDocument3 pagesTransaction Date Value Date Cheque Number/ Transaction Number Description Debit Credit Running Balancesreekanth chinthaNo ratings yet

- U06CaptureImage PDFDocument1 pageU06CaptureImage PDFFranciscoArandaMateuNo ratings yet

- Applications and Examples of Experiments With Mobile Phones and Smartphones in Physics LessonsDocument7 pagesApplications and Examples of Experiments With Mobile Phones and Smartphones in Physics LessonsSEP-PublisherNo ratings yet

- Radio MobileDocument78 pagesRadio Mobilefatmirz9448No ratings yet

- HBD E570Document1 pageHBD E570Rafael RodríguezNo ratings yet

- 3rd International Conference On Filipino As Global Language - Call For PapersDocument2 pages3rd International Conference On Filipino As Global Language - Call For PapersDavid Michael San JuanNo ratings yet

- Cswip - Section 06-Wps and Welders QualificationDocument15 pagesCswip - Section 06-Wps and Welders QualificationNsidibe Michael Etim100% (1)

- Lec#02 PDC - Design Aspects of A Process Control SystemDocument19 pagesLec#02 PDC - Design Aspects of A Process Control SystemqamarVEXNo ratings yet

- A4954 Datasheet PDFDocument9 pagesA4954 Datasheet PDFJason WuNo ratings yet

- Myers Briggs Type Indicator PIODocument1 pageMyers Briggs Type Indicator PIODesi Tri SatrianiNo ratings yet

- Walbro Carburetor WA-133-1 Parts Diagram For WA-133-1 PARTS LISTDocument3 pagesWalbro Carburetor WA-133-1 Parts Diagram For WA-133-1 PARTS LISTRoberto ZilianiNo ratings yet

- CKTG Quarter 2 Table of ContentsDocument6 pagesCKTG Quarter 2 Table of Contentsreychelle santeNo ratings yet

- 1íócylinder BlockDocument11 pages1íócylinder BlockGames of LifeNo ratings yet

- BUSINESS PROFILE Example PDFDocument2 pagesBUSINESS PROFILE Example PDFHisham Adiong SacarNo ratings yet

- Tough of The Toughest Interview QuestionsDocument4 pagesTough of The Toughest Interview Questionsalexsh_hahaNo ratings yet

- Globalization and EducationDocument3 pagesGlobalization and Educationava1234567890No ratings yet

- Gilchrist & Soames Order # 18270013Document1 pageGilchrist & Soames Order # 18270013vision23No ratings yet