You might also like

- RE1 and RE5 Preparation Document-Final Document UpdatedDocument38 pagesRE1 and RE5 Preparation Document-Final Document UpdatedBrian KufahakutizwiNo ratings yet

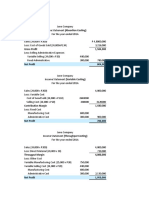

- Financial Statement Analysis ExerciseDocument5 pagesFinancial Statement Analysis ExerciseMelanie SamsonaNo ratings yet

- Statement of Comprehensive Income: Problem 1: True or FalseDocument17 pagesStatement of Comprehensive Income: Problem 1: True or FalsePaula Bautista100% (3)

- An Analysis of The Business and Financial Performance of Tesco PLCDocument17 pagesAn Analysis of The Business and Financial Performance of Tesco PLCbanardsNo ratings yet

- Project Management-Interview QuestionsDocument10 pagesProject Management-Interview QuestionsPrakash MuraliNo ratings yet

- Quiz 4 Audit ProbDocument5 pagesQuiz 4 Audit ProbVinz Patrick E. PerochoNo ratings yet

- Accounting Changes and ErrorsDocument3 pagesAccounting Changes and ErrorsJohn Emerson PatricioNo ratings yet

- Cfas - Journal EntriesDocument3 pagesCfas - Journal EntriesJefferson SarmientoNo ratings yet

- Multiple StepDocument1 pageMultiple StepMerza DyanNo ratings yet

- Lesson 4 Income Statement Balance SheetDocument5 pagesLesson 4 Income Statement Balance SheetklipordNo ratings yet

- 2108AFE Topic 3 Inventory and Retail Operations - StudentDocument79 pages2108AFE Topic 3 Inventory and Retail Operations - StudentAnh TrầnNo ratings yet

- Cash and AccrualDocument3 pagesCash and Accrual夜晨曦No ratings yet

- 05 Current Taxation 05 Current TaxationDocument28 pages05 Current Taxation 05 Current TaxationShehrozSTNo ratings yet

- Adjusting Entries For Merchandising (4 Step) : Merchandising Concern Manufacturing ConcernDocument1 pageAdjusting Entries For Merchandising (4 Step) : Merchandising Concern Manufacturing ConcernyzaNo ratings yet

- Statement of Cash FlowDocument6 pagesStatement of Cash FlowNhel AlvaroNo ratings yet

- Chapter 10Document12 pagesChapter 10Villanueva, Jane G.No ratings yet

- Accounting Chap 5Document6 pagesAccounting Chap 5Nguyễn Ngọc MaiNo ratings yet

- 6804 - Lecture On Statement of Comprehensive IncomeDocument2 pages6804 - Lecture On Statement of Comprehensive IncomeJustine TadeoNo ratings yet

- Chapter 9Document23 pagesChapter 9TouseefsabNo ratings yet

- HW Chap 5Document9 pagesHW Chap 5uong huonglyNo ratings yet

- Subsequent Events and Cash and Acrrual BasisDocument14 pagesSubsequent Events and Cash and Acrrual BasisKezNo ratings yet

- FINACCREDocument187 pagesFINACCREKendall JennerNo ratings yet

- PDF Sol Man Chapter 10 Cash To Accrual Basis of Acctg - CompressDocument9 pagesPDF Sol Man Chapter 10 Cash To Accrual Basis of Acctg - CompressFrost GarisonNo ratings yet

- 2 Assignment For Midterm - Merchandising Business: (Periodic System)Document4 pages2 Assignment For Midterm - Merchandising Business: (Periodic System)Lisa PalermoNo ratings yet

- Auditing SM CH 2 2019Document13 pagesAuditing SM CH 2 2019Angel BalatucanNo ratings yet

- Financial Statements Analysis - Ratio AnalysisDocument44 pagesFinancial Statements Analysis - Ratio AnalysisDipanjan SenguptaNo ratings yet

- Business Finance: Session 3: Financial StatementsDocument45 pagesBusiness Finance: Session 3: Financial StatementsXia AlliaNo ratings yet

- Preliminary Balance Sheet AssetsDocument3 pagesPreliminary Balance Sheet AssetsleuleuNo ratings yet

- The Statement of Comprehensive Income: Profit For The YearDocument4 pagesThe Statement of Comprehensive Income: Profit For The YearPlawan GhimireNo ratings yet

- Classroom Notes 6393 and 6394Document2 pagesClassroom Notes 6393 and 6394Mary Grace Galleon-Yang OmacNo ratings yet

- Review Notes #2 - Comprehensive Problem PDFDocument3 pagesReview Notes #2 - Comprehensive Problem PDFtankofdoom 4No ratings yet

- MASDocument6 pagesMASDan RyanNo ratings yet

- PRACTICEDocument4 pagesPRACTICEGleeson Jay NiedoNo ratings yet

- Installment SalesDocument12 pagesInstallment SalesRusselle Therese DaitolNo ratings yet

- Merchandising Operations: Inventory Base. These Items Are Then Resold To Customers and Recorded As Sales RevenueDocument12 pagesMerchandising Operations: Inventory Base. These Items Are Then Resold To Customers and Recorded As Sales RevenueMingxNo ratings yet

- Advance Chapter 3Document12 pagesAdvance Chapter 3abel habtamuNo ratings yet

- CAB AcctDocument9 pagesCAB AcctA.J. ChuaNo ratings yet

- AUDPROB CHPT 5 and 61Document30 pagesAUDPROB CHPT 5 and 61Jem ValmonteNo ratings yet

- Asdos Pert 2Document2 pagesAsdos Pert 2mutiaoooNo ratings yet

- Answer Key Q1 PDFDocument4 pagesAnswer Key Q1 PDFNonami AbicoNo ratings yet

- Chapter 3Document12 pagesChapter 3Solomon AbebeNo ratings yet

- Exercises IAS 8 SolutionDocument5 pagesExercises IAS 8 SolutionLê Xuân HồNo ratings yet

- Business Transactions and Their Analysis As Applied To THE Accounting Cycle of A Merchandising Business (Part Ii)Document6 pagesBusiness Transactions and Their Analysis As Applied To THE Accounting Cycle of A Merchandising Business (Part Ii)Tumamudtamud, JenaNo ratings yet

- 07 Quiz 1 - SCMDocument1 page07 Quiz 1 - SCMJen DeloyNo ratings yet

- Common Size and Comparative Statements Format of Statement of Profit and LossDocument18 pagesCommon Size and Comparative Statements Format of Statement of Profit and LosssatyaNo ratings yet

- CosoldatedDocument11 pagesCosoldatedShafiqNo ratings yet

- 2 Case1 1bFinPlannNEWFashionSHOPS2022 23SolutionTemplateDocument8 pages2 Case1 1bFinPlannNEWFashionSHOPS2022 23SolutionTemplatesantiagoNo ratings yet

- Closing Entries AND Reversing Entries: John G. Pagaddut, Cpa, LPT, MsaDocument12 pagesClosing Entries AND Reversing Entries: John G. Pagaddut, Cpa, LPT, MsaGeraldine Lop-nao GermanoNo ratings yet

- Financial Accounting: Tools For Business Decision Making: Ninth EditionDocument70 pagesFinancial Accounting: Tools For Business Decision Making: Ninth EditionJesussNo ratings yet

- Adjustment To Financial Statements-1-1Document6 pagesAdjustment To Financial Statements-1-1Usman AttiqueNo ratings yet

- CFS Baf 1 CpaDocument6 pagesCFS Baf 1 CpaErnest NyangiNo ratings yet

- Badvac1x - Mod 5 TemplatesDocument18 pagesBadvac1x - Mod 5 Templatesfaye pantiNo ratings yet

- Chapter 15: Single Entry Characteristics of Single EntryDocument12 pagesChapter 15: Single Entry Characteristics of Single EntryPaula Bautista100% (2)

- Discussion For Adjustment Entries - QuestionsDocument6 pagesDiscussion For Adjustment Entries - QuestionsMUHAMMAD ZAIM ILYASA KASIMNo ratings yet

- P1-Single Entry FormulasDocument3 pagesP1-Single Entry FormulasJohn Yrick EraNo ratings yet

- Domondon - Acctg 3 - Prelim Quiz 2Document2 pagesDomondon - Acctg 3 - Prelim Quiz 2Prince Anton DomondonNo ratings yet

- Pr. 4-146-Income StatementDocument13 pagesPr. 4-146-Income StatementElene SamnidzeNo ratings yet

- SBA03 FSAnalysisPart32of3Document5 pagesSBA03 FSAnalysisPart32of3Jr PedidaNo ratings yet

- FAR.0747 - Cash To AccrualDocument8 pagesFAR.0747 - Cash To Accrualandrew dacullaNo ratings yet

- Cash Basis To Accrual Basis of Accounting: Problem 1: For Classroom DiscussionDocument9 pagesCash Basis To Accrual Basis of Accounting: Problem 1: For Classroom DiscussionPaula BautistaNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Facilities Management Quality and User Satisfaction in Outsourced ServicesDocument16 pagesFacilities Management Quality and User Satisfaction in Outsourced ServicesAHMEDNABTNo ratings yet

- Tracking ReportDocument135 pagesTracking ReportRoel AllosadaNo ratings yet

- Reset and Reverse Down Payment ClearingsDocument8 pagesReset and Reverse Down Payment Clearingssuhas_12345No ratings yet

- Resource Allocation: Class 7: 3/9/11Document64 pagesResource Allocation: Class 7: 3/9/11Tyas AgustinaNo ratings yet

- Malaysia Airlines Business Transformation Plan BTP 2 1Document50 pagesMalaysia Airlines Business Transformation Plan BTP 2 1Nisha100% (1)

- Nivea OsDocument17 pagesNivea OsNikhil AggarwalNo ratings yet

- Introduction To Managing A Service EnterpriseDocument21 pagesIntroduction To Managing A Service EnterpriseJulius Hans GallegoNo ratings yet

- Hannah Money Resume 2Document2 pagesHannah Money Resume 2api-289276737No ratings yet

- Finlatics Investment Banking Experience ProgramDocument4 pagesFinlatics Investment Banking Experience ProgramSameer BheriNo ratings yet

- Symposium: Organizational Ambidexterity: Past, Present, and FutureDocument15 pagesSymposium: Organizational Ambidexterity: Past, Present, and FutureIsmail JamesNo ratings yet

- Allianz Annual Report 2020Document290 pagesAllianz Annual Report 2020Hafiz IqbalNo ratings yet

- ABCDDocument45 pagesABCDKartik GaurNo ratings yet

- Chapter 13 LeaseDocument29 pagesChapter 13 LeaseHammad Ahmad100% (2)

- Leadership FinalDocument23 pagesLeadership Finalapi-302501867No ratings yet

- Causes and Effects of InflationDocument10 pagesCauses and Effects of Inflationprof_akvchary100% (1)

- (Full Paper) Greek Tourism Under Crisi - Strategies and The Way OutDocument24 pages(Full Paper) Greek Tourism Under Crisi - Strategies and The Way OutSotiris VarelasNo ratings yet

- As 3724-1994 Fibreboard Boxes For The Export of Meat Meat Products and OffalDocument7 pagesAs 3724-1994 Fibreboard Boxes For The Export of Meat Meat Products and OffalSAI Global - APACNo ratings yet

- Inbound Supply Chain Methodology of Indian Sugar Industry: R.S.Deshmukh N.N.Bhostekar U.V.Aswalekar V.B.SawantDocument8 pagesInbound Supply Chain Methodology of Indian Sugar Industry: R.S.Deshmukh N.N.Bhostekar U.V.Aswalekar V.B.SawantnileshsawNo ratings yet

- Labor Code 2810.5 NoticeDocument2 pagesLabor Code 2810.5 NoticejohnlusfNo ratings yet

- Tib Ems Users GuideDocument641 pagesTib Ems Users GuidejanofassNo ratings yet

- Global Marketing in Health SectorDocument10 pagesGlobal Marketing in Health SectorMythily Vedhagiri100% (2)

- RESA ReviewersDocument8 pagesRESA Reviewersmommel53150% (6)

- HRM Case Study TemplatesDocument3 pagesHRM Case Study TemplatesSolexNo ratings yet

- Kotler Mm15e Inppt 02Document34 pagesKotler Mm15e Inppt 02Eng Eman HannounNo ratings yet

- SwotDocument3 pagesSwotRichman ManabatNo ratings yet

- Optical Media Act of 2003 PDFDocument13 pagesOptical Media Act of 2003 PDFCHow GatchallanNo ratings yet

- CONTRACT COSTING - Chapter 6Document21 pagesCONTRACT COSTING - Chapter 6abhilekh91No ratings yet