You might also like

- A Street Car Named Desire (Penguin)Document18 pagesA Street Car Named Desire (Penguin)the_perfectionistNo ratings yet

- Financial Accounting and Reporting Study Guide NotesFrom EverandFinancial Accounting and Reporting Study Guide NotesRating: 1 out of 5 stars1/5 (1)

- 1964-1986 OMC Sterndrive ManualDocument572 pages1964-1986 OMC Sterndrive ManualBarry Pieters75% (4)

- Absorption and Variable Costing Income Statement: Reporter: Sharmaine Laye M. PascualDocument20 pagesAbsorption and Variable Costing Income Statement: Reporter: Sharmaine Laye M. PascualPatrick LanceNo ratings yet

- Fringe Benefit TaxDocument9 pagesFringe Benefit TaxAlexander Dimalipos100% (2)

- Inclusion and Exclusion of GIDocument14 pagesInclusion and Exclusion of GIRoxanne Dela Cruz100% (1)

- Client Hunting HandbookDocument105 pagesClient Hunting Handbookc__brown_3No ratings yet

- Senior Citizen and PDWDocument6 pagesSenior Citizen and PDWNico evansNo ratings yet

- Income Taxation Solution Manual 2019 Ed 2Document40 pagesIncome Taxation Solution Manual 2019 Ed 2Alexander DimaliposNo ratings yet

- 02 Fin MarketDocument89 pages02 Fin MarketyovitaNo ratings yet

- Auditing Theory 250 QuestionsDocument39 pagesAuditing Theory 250 Questionsxxxxxxxxx75% (4)

- VAT Output TaxesDocument7 pagesVAT Output TaxesJocelyn Verbo-AyubanNo ratings yet

- Marginal Costing & Absorption CostingDocument56 pagesMarginal Costing & Absorption CostingHoàng Phương ThảoNo ratings yet

- Taxation Law BarQA 2009-2017 PDFDocument195 pagesTaxation Law BarQA 2009-2017 PDFAjilNo ratings yet

- IFRSDocument98 pagesIFRSadelia100% (1)

- Revised Summer 2015 Key ConceptsDocument28 pagesRevised Summer 2015 Key ConceptsGelyn CruzNo ratings yet

- Tax Compliance RequirementsDocument8 pagesTax Compliance RequirementsJocelyn Verbo-AyubanNo ratings yet

- ch13 Testbank Intermediate AccountingDocument43 pagesch13 Testbank Intermediate Accountingalaa96% (53)

- Donor's Tax Rates and ExemptionsDocument7 pagesDonor's Tax Rates and ExemptionsRanel Clark D. Tabios50% (2)

- MAS-03: Understanding absorption and variable costingDocument4 pagesMAS-03: Understanding absorption and variable costingClint AbenojaNo ratings yet

- Zomer Development Company, Inc Vs Special 20th Division of CADocument20 pagesZomer Development Company, Inc Vs Special 20th Division of CACJNo ratings yet

- CPE655 Solid Waste ManagementDocument108 pagesCPE655 Solid Waste ManagementAmirah SufianNo ratings yet

- TAX-1202: Special Allowable Itemized Deductions: - T R S ADocument2 pagesTAX-1202: Special Allowable Itemized Deductions: - T R S AAlexander Dimalipos100% (1)

- MAS 04: ABSORPTION VS VARIABLE COSTINGDocument8 pagesMAS 04: ABSORPTION VS VARIABLE COSTINGJunZon VelascoNo ratings yet

- Osamu Dazai: Genius, But No Saint - The Japan TimesDocument3 pagesOsamu Dazai: Genius, But No Saint - The Japan TimesBenito TenebrosusNo ratings yet

- Management Accounting NotesDocument212 pagesManagement Accounting NotesFrank Chinguwo100% (1)

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Absorption Vs Marginal CostingDocument24 pagesAbsorption Vs Marginal CostingPoint BlankNo ratings yet

- Absorption and Variable CostingDocument5 pagesAbsorption and Variable CostingKIM RAGANo ratings yet

- Manure HandlingDocument14 pagesManure HandlingIvan Sampson100% (1)

- Contribution Approach 2Document16 pagesContribution Approach 2kualler80% (5)

- Al WakalahDocument12 pagesAl WakalahMahyuddin Khalid100% (3)

- Manufacturing Account NotesDocument7 pagesManufacturing Account Notesdayna davisNo ratings yet

- Absorption Costing GclassDocument4 pagesAbsorption Costing GclassDoromal, Jerome A.No ratings yet

- Variable Costing ConceptsDocument10 pagesVariable Costing Conceptsrodell pabloNo ratings yet

- Int To Management AccDocument53 pagesInt To Management AccPUTTU GURU PRASAD SENGUNTHA MUDALIARNo ratings yet

- Lecture 4 - 5 17102022 032709am 07032023 090715pm 17102023 015148pmDocument41 pagesLecture 4 - 5 17102022 032709am 07032023 090715pm 17102023 015148pmmurtaza haiderNo ratings yet

- Inventories Notes2 170419181823Document28 pagesInventories Notes2 170419181823Ebsa AdemeNo ratings yet

- Chapter 19Document51 pagesChapter 19Kanika AggarwalNo ratings yet

- DAC 5013-Week 03Document60 pagesDAC 5013-Week 03Dilshan J. NiranjanNo ratings yet

- Marginal and Absorption CostingDocument15 pagesMarginal and Absorption CostingCollins AbereNo ratings yet

- 1.3 Income Statement and Statement of Comrehensive IncomeDocument20 pages1.3 Income Statement and Statement of Comrehensive IncomeRula Abu NuwarNo ratings yet

- Overview of Absorption and Variable CostingDocument5 pagesOverview of Absorption and Variable CostingJarrelaine SerranoNo ratings yet

- Variable costing key conceptsDocument21 pagesVariable costing key conceptsMary Rose GonzalesNo ratings yet

- Cost & Mgt II CH 1Document13 pagesCost & Mgt II CH 1fikruhope533No ratings yet

- CMA CU - Chap 6Document24 pagesCMA CU - Chap 6TAMANNANo ratings yet

- MAS 04 Absorption CostingDocument6 pagesMAS 04 Absorption CostingJoelyn Grace MontajesNo ratings yet

- Module 3 SCMDocument9 pagesModule 3 SCMKhai LaNo ratings yet

- Introduction To Cost Accounting: La Verdad Christian Colleges Cost Accounting First Term SY 2021-2022Document3 pagesIntroduction To Cost Accounting: La Verdad Christian Colleges Cost Accounting First Term SY 2021-2022Adriana Del rosarioNo ratings yet

- ABSORPTION VS VARIABLE COSTINGDocument3 pagesABSORPTION VS VARIABLE COSTINGDhona Mae FidelNo ratings yet

- Stement of Comprehensive IncomeDocument28 pagesStement of Comprehensive Incomemaricar reyesNo ratings yet

- Job Order Costing 16112021 123409pmDocument8 pagesJob Order Costing 16112021 123409pmHassan AliNo ratings yet

- Absorption Costing & Variable CostingDocument20 pagesAbsorption Costing & Variable Costingsaidkhatib368No ratings yet

- Cost AccountingDocument17 pagesCost AccountingFaisal RafiqNo ratings yet

- Nobles Acctg10 PPT 05Document69 pagesNobles Acctg10 PPT 05Tayar ElieNo ratings yet

- 3MA 03 Absortion and Variable CostingDocument3 pages3MA 03 Absortion and Variable CostingAbigail Regondola BonitaNo ratings yet

- Lecture 1-Financial Statements I-SDocument75 pagesLecture 1-Financial Statements I-SjamesbinstrateNo ratings yet

- Analyze Financial Statements and Valuation TechniquesDocument43 pagesAnalyze Financial Statements and Valuation TechniquesfelipeNo ratings yet

- Accounting & Control: Cost ManagementDocument39 pagesAccounting & Control: Cost ManagementciconsultanNo ratings yet

- Financial Statements ExplainedDocument9 pagesFinancial Statements ExplainedTokie TokiNo ratings yet

- Managerial Accounting: Tools For Business Decision-MakingDocument69 pagesManagerial Accounting: Tools For Business Decision-MakingdavidNo ratings yet

- Accounting & Control: Cost ManagementDocument39 pagesAccounting & Control: Cost ManagementKM RobinNo ratings yet

- Chapter 2 Cost Acct (Mowen)Document20 pagesChapter 2 Cost Acct (Mowen)Kelly Brenda CruzNo ratings yet

- ACCTG 42 Module 3Document5 pagesACCTG 42 Module 3Hazel Grace PaguiaNo ratings yet

- CLO 3 - LGE 3503 Accounting For ManagersDocument25 pagesCLO 3 - LGE 3503 Accounting For ManagersHello WorldNo ratings yet

- Financial Statements: I. Income StatementDocument3 pagesFinancial Statements: I. Income StatementKen MateyowNo ratings yet

- Manufacturing Costs Lecture Version 2 STUDENT VERSIONDocument15 pagesManufacturing Costs Lecture Version 2 STUDENT VERSIONLampel Louise LlandaNo ratings yet

- Principles of Cost Accounting 14EDocument30 pagesPrinciples of Cost Accounting 14Etegegn mogessieNo ratings yet

- Variable CostingDocument34 pagesVariable CostingScraper LancelotNo ratings yet

- Absorption Costing For STDocument6 pagesAbsorption Costing For STDEREJENo ratings yet

- Cost Accounting FundamentalsDocument26 pagesCost Accounting FundamentalsSiraj MohammedNo ratings yet

- Presentation4.1 - Audit of Inventories, Cost of Sales and Other Related AccountsDocument37 pagesPresentation4.1 - Audit of Inventories, Cost of Sales and Other Related AccountsRoseanne Dela CruzNo ratings yet

- Absorption and Variable Costing: Types of Product Costing MethodDocument2 pagesAbsorption and Variable Costing: Types of Product Costing MethodKuya ANo ratings yet

- Absorption Costing Vs Variable CostingDocument20 pagesAbsorption Costing Vs Variable CostingMa. Alene MagdaraogNo ratings yet

- 107-W7-8-Variable cost-chp05-STDocument48 pages107-W7-8-Variable cost-chp05-STmargaret mariaNo ratings yet

- Chapter 07 - Introduction To Inventories and The Classified Incomes StatementDocument10 pagesChapter 07 - Introduction To Inventories and The Classified Incomes StatementSayed AnwarNo ratings yet

- Variable Costing & Segment Reporting-FINALDocument29 pagesVariable Costing & Segment Reporting-FINALTin Bernadette DominicoNo ratings yet

- Sesi 2 Akuntansi ManajemenDocument33 pagesSesi 2 Akuntansi ManajemenDian Permata SariNo ratings yet

- ACCA Level 2&3 Foundation Course (Text II)Document8 pagesACCA Level 2&3 Foundation Course (Text II)CarnegieNo ratings yet

- Fundamentalsofabm2statementofcomprehensiveincomeabmspecializedsubject 171210045513Document12 pagesFundamentalsofabm2statementofcomprehensiveincomeabmspecializedsubject 171210045513Aira Nhaira MecateNo ratings yet

- ACT2111 Fall 2019 Ch6 - Lecture 9&10 - StudentDocument62 pagesACT2111 Fall 2019 Ch6 - Lecture 9&10 - StudentKevinNo ratings yet

- Notes and Summary in Product Costing With QuizzerDocument12 pagesNotes and Summary in Product Costing With QuizzerCykee Hanna Quizo LumongsodNo ratings yet

- Ia Vol 3 Valix 2019 Solman 2 PDF FreeDocument105 pagesIa Vol 3 Valix 2019 Solman 2 PDF FreeLJNo ratings yet

- Accounting For Income TaxDocument4 pagesAccounting For Income TaxMjhayeNo ratings yet

- G.R. No. 92087: Torts and Damages Case Digest: Fernando V. CA (1992)Document2 pagesG.R. No. 92087: Torts and Damages Case Digest: Fernando V. CA (1992)Alexander DimaliposNo ratings yet

- FAR 4116 CleanDocument7 pagesFAR 4116 Cleanruel c armillaNo ratings yet

- Torts Case Digest on Fernando v. CA (1992Document2 pagesTorts Case Digest on Fernando v. CA (1992Alexander DimaliposNo ratings yet

- G.R. No. 92087: Torts and Damages Case Digest: Fernando V. CA (1992)Document2 pagesG.R. No. 92087: Torts and Damages Case Digest: Fernando V. CA (1992)Alexander DimaliposNo ratings yet

- Name: Setienor B. Panduma Year and Section: Accy2 Date: May 6, 2021Document3 pagesName: Setienor B. Panduma Year and Section: Accy2 Date: May 6, 2021Alexander DimaliposNo ratings yet

- G.R. No. 92087: Torts and Damages Case Digest: Fernando V. CA (1992)Document2 pagesG.R. No. 92087: Torts and Damages Case Digest: Fernando V. CA (1992)Alexander DimaliposNo ratings yet

- Discussion Problems: FAR.2935-Income Taxes OCTOBER 2020Document4 pagesDiscussion Problems: FAR.2935-Income Taxes OCTOBER 2020Alexander DimaliposNo ratings yet

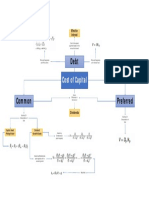

- Cost of Capital: Effective InterestDocument1 pageCost of Capital: Effective InterestAlexander DimaliposNo ratings yet

- Business and Human Rights WebDocument20 pagesBusiness and Human Rights WebAlexander DimaliposNo ratings yet

- Midterm Quiz 1 Gross IncomeDocument3 pagesMidterm Quiz 1 Gross IncomeMjhayeNo ratings yet

- Estate TaxDocument15 pagesEstate TaxDustin PascuaNo ratings yet

- Chap 36 - Land and Building Fin Acct 1 - Barter Summary Team PDFDocument4 pagesChap 36 - Land and Building Fin Acct 1 - Barter Summary Team PDFJunneth Pearl HomocNo ratings yet

- TAXATION OF CAPITAL GAINS AND PASSIVE INCOMEDocument12 pagesTAXATION OF CAPITAL GAINS AND PASSIVE INCOMELiyana ChuaNo ratings yet

- Capital Asset and Capital Gains LossDocument4 pagesCapital Asset and Capital Gains LossAmy Olaes DulnuanNo ratings yet

- Abm01 - Module 5-6.1 (Bus. Transaction)Document19 pagesAbm01 - Module 5-6.1 (Bus. Transaction)Love JcwNo ratings yet

- Grammar Marwa 22Document5 pagesGrammar Marwa 22YAGOUB MUSANo ratings yet

- Notes of Meetings MergedDocument8 pagesNotes of Meetings MergedKreeshnee OreeNo ratings yet

- A CHAIN OF THUNDER: A Novel of The Siege of Vicksburg by Jeff ShaaraDocument13 pagesA CHAIN OF THUNDER: A Novel of The Siege of Vicksburg by Jeff ShaaraRandom House Publishing Group20% (5)

- ch-1 Phy MEASUREMENT AND MOTIONDocument2 pagesch-1 Phy MEASUREMENT AND MOTIONRakesh GuptaNo ratings yet

- Instructions: Skim The Following Job Advertisements. Then, Scan The Text That Follows andDocument2 pagesInstructions: Skim The Following Job Advertisements. Then, Scan The Text That Follows andVasu WinNo ratings yet

- Municipal Trial Court in Cities: Motion For Release On RecognizanceDocument4 pagesMunicipal Trial Court in Cities: Motion For Release On RecognizanceMaria Leonora TheresaNo ratings yet

- Semi Anual SM Semana 15Document64 pagesSemi Anual SM Semana 15Leslie Caysahuana de la cruzNo ratings yet

- Public High School Teachers' Strategies for Addressing Challenges in Conducting Action ResearchDocument75 pagesPublic High School Teachers' Strategies for Addressing Challenges in Conducting Action ResearchMilbert Loyloy SalmasanNo ratings yet

- Case Week 2Document2 pagesCase Week 2Reta AzkaNo ratings yet

- Inter CavablarDocument86 pagesInter CavablarcavidannuriyevNo ratings yet

- CVDocument7 pagesCVRedemptah Mutheu MutuaNo ratings yet

- Review On Birth Asphyxia by TibinDocument22 pagesReview On Birth Asphyxia by Tibintibinj67No ratings yet

- 10 INSIGHT - 2023 - D SouzaDocument7 pages10 INSIGHT - 2023 - D SouzazhaobingNo ratings yet

- Parallel Worlds ChessDocument2 pagesParallel Worlds ChessRobert BonisoloNo ratings yet

- JVC Mini DV and S-VHS Deck Instruction Sheet: I. Capturing FootageDocument3 pagesJVC Mini DV and S-VHS Deck Instruction Sheet: I. Capturing Footagecabonedu0340No ratings yet

- Asma G.SDocument5 pagesAsma G.SAfia FaheemNo ratings yet

- GNM 10102023Document118 pagesGNM 10102023mohammedfz19999No ratings yet

- Integrated BMSDocument14 pagesIntegrated BMSjim.walton100% (5)

- Mikro Prism Manual English PDFDocument18 pagesMikro Prism Manual English PDFrakeshr2007No ratings yet

- Chapter 01Document33 pagesChapter 01Michael BANo ratings yet

- Levis Vs VogueDocument12 pagesLevis Vs VoguedayneblazeNo ratings yet